The Capital Markets Union and Savings and Investments Union: Unlocking Trillions for EU Competitiveness

Europe has the savings but not yet the capital-market depth to fund its green, digital, and strategic ambitions at scale.

OpenMacro

The EU’s Savings and Investments Union could unlock trillions in underused household savings, deepen capital markets, lower financing costs, and help close Europe’s annual investment gap. If fully implemented, it would strengthen innovation, resilience, and competitiveness against the US and China.

As of mid-2026, the European Union stands at a critical juncture. Geopolitical tensions, the need for massive green and digital investment, and intensifying competition with the United States and China are forcing Europe to confront one of its deepest structural weaknesses: it has ample savings, but an underdeveloped and fragmented system for channeling those savings into productive investment.

The shift from the Capital Markets Union, launched in 2015, to the Savings and Investments Union, formally introduced by the European Commission in March 2025, reflects Europe’s most serious attempt yet to create a genuine single market for capital. This is not simply a financial-sector reform. It is a strategic project aimed at improving growth, resilience, and long-term competitiveness.

With household financial assets exceeding €40 trillion and an annual investment gap estimated at €800 billion to €1.2 trillion, the stakes are immense. If Europe can mobilize even a modest share of idle savings more effectively, it can materially strengthen its capacity to fund innovation, infrastructure, defense, and the green transition.

1. The Persistent Fragmentation Problem

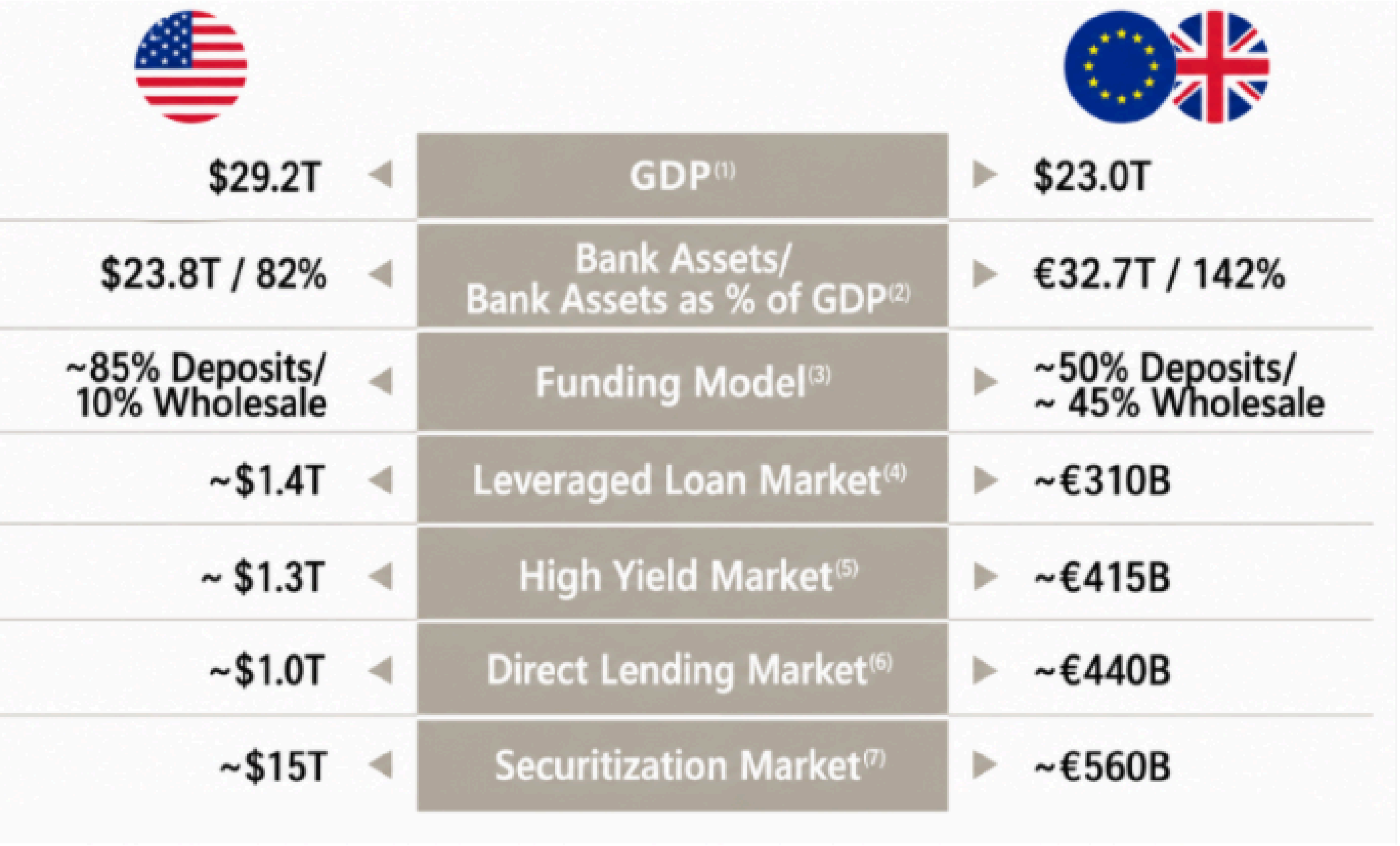

Europe’s financial system remains overwhelmingly bank-centric. In many member states, banks still provide around 80% of corporate financing, in sharp contrast to the United States, where capital markets play the dominant role. This creates structural vulnerabilities: when banks retrench during downturns, financing to the real economy contracts more sharply, smaller firms struggle to scale, and cross-border capital allocation remains constrained by national fragmentation.

The gap with the United States is visible across multiple dimensions. EU stock-market capitalization remains far shallower relative to GDP, leveraged finance and securitization markets are much smaller, and Europe’s funding model is still far more dependent on deposits and bank balance sheets. This is not just a financial-sector difference. It shapes the entire competitive capacity of the European economy.

Figure 1

Europe’s financial system remains much more bank-centric than the United States, leaving it with shallower capital markets and a weaker scale-up environment for innovative firms.

Source: OpenMacro

This imbalance creates several weaknesses at once. It makes the system more procyclical, because bank stress transmits quickly to business financing. It leaves SMEs heavily dependent on credit rather than risk capital. And it prevents savings from moving efficiently across borders into the sectors and firms where they would be most productive.

Why Europe lags in capital-market depth

| Structural issue | Why it matters | Competitive consequence |

|---|---|---|

| Bank-heavy financing | Firms rely too much on bank credit | Less risk capital for scaling and innovation |

| Fragmented regulation | Capital cannot move as freely across borders | Lower efficiency and weaker market depth |

| Shallow equity markets | Fewer exit and growth-financing options | Lower valuations and slower expansion |

| Underused household savings | Too much wealth sits in deposits | Productive investment remains underfunded |

2. Europe’s Household Savings Are an Untapped Reservoir

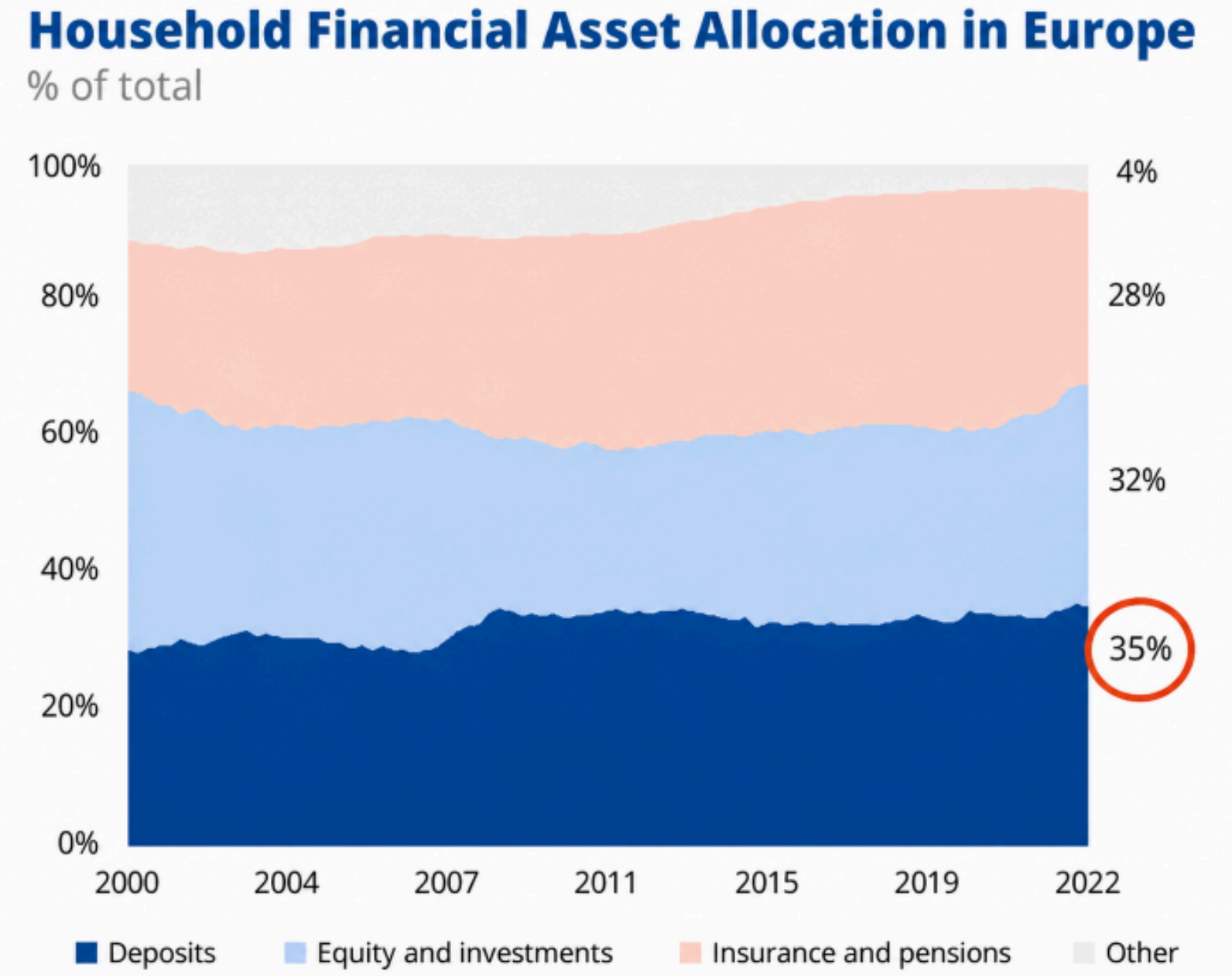

Europe is not poor in capital. It is inefficient in how it allocates it. Roughly one-third or more of household financial wealth remains in cash and bank deposits, generating low returns for savers while leaving businesses short of long-term equity, venture capital, and infrastructure finance.

This is partly a product of culture and risk preferences, but it is also a consequence of policy design. Retail investment products remain fragmented, cross-border investment is still cumbersome, and many households lack easy access to attractive, transparent market-based savings vehicles. The result is a system in which savings are abundant, but risk capital remains scarce.

Figure 2

A large share of European household wealth remains parked in deposits rather than flowing into equities, pensions, and long-term productive investment.

Source: OpenMacro

By contrast, the United States channels far more household wealth into equities, pensions, and capital-market instruments. That does not just improve long-term returns for households. It also gives companies deeper and more liquid financing pools, which in turn support technological leadership, startup scaling, and stronger overall productivity.

3. Why the SIU Matters in 2026

The Savings and Investments Union is the EU’s attempt to fix this structural problem. Launched in March 2025, it builds on the Capital Markets Union agenda while also connecting more clearly to banking-union goals, supervisory convergence, retail participation, and the broader need for strategic investment at scale.

By early 2026, the SIU agenda had already produced meaningful milestones. The Commission had formally laid out the strategy, the Council had moved toward insolvency harmonization, and political agreement had been reached on revitalizing securitization markets. These steps matter because legal fragmentation and weak market plumbing have long been among the biggest barriers to cross-border capital flows in Europe.

The strategy is often framed around five priorities: stronger supervision, deeper securitization and market-making, sustainable finance, better access to equity for SMEs, and the development of safe and liquid assets. Taken together, these are meant to give Europe a more coherent financial architecture rather than just a collection of national markets loosely connected by EU membership.

What SIU is trying to fix

- Fragmented national markets

- Weak retail-market participation

- Limited scale-up financing

- Shallow securitization and private-credit channels

- Insufficient cross-border risk sharing

What SIU is trying to build

- More unified supervision

- Deeper and more liquid market funding

- Better SME and equity access

- More productive use of household savings

- A stronger EU investment ecosystem

4. The Innovation and Competitiveness Case

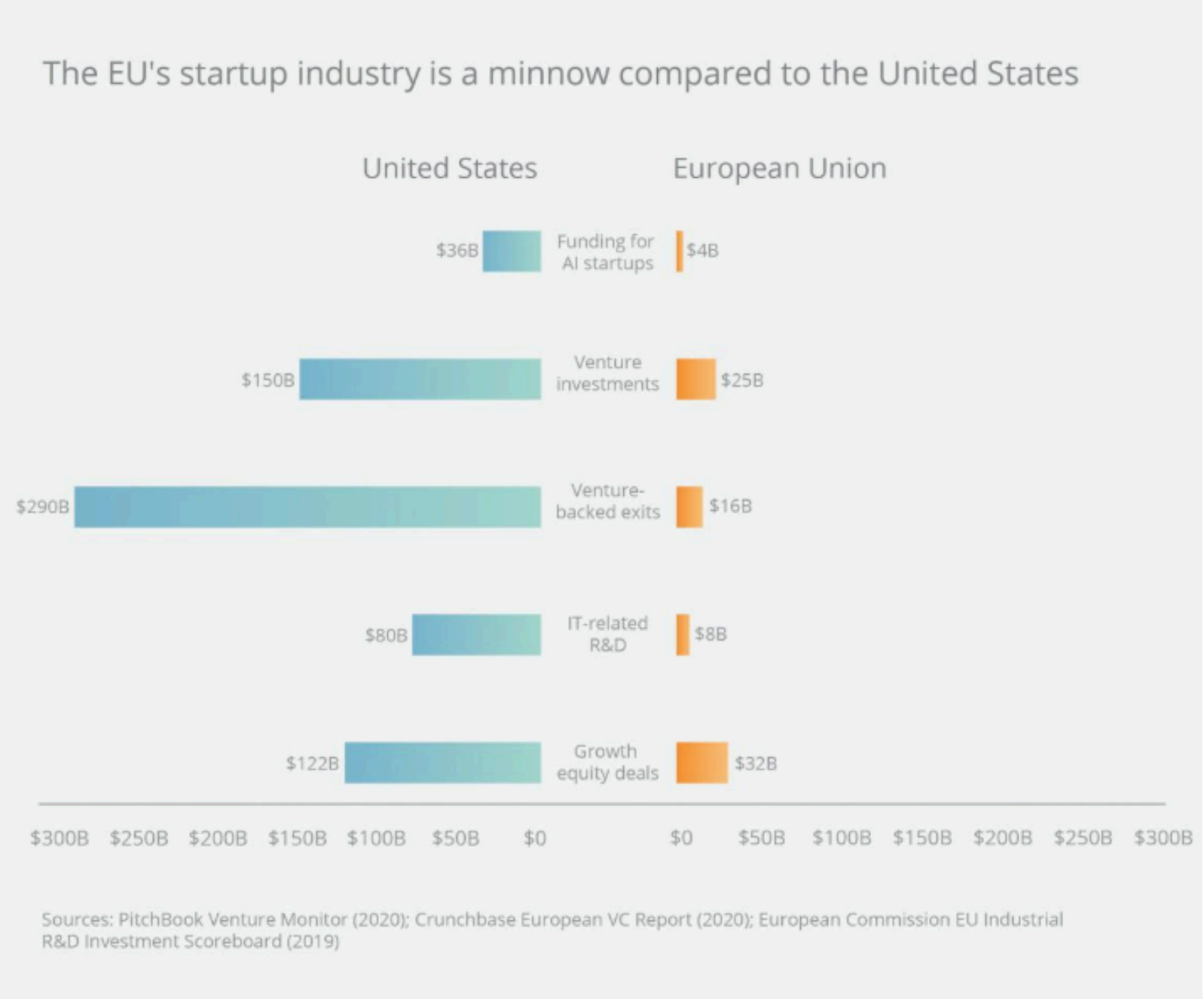

A stronger capital-market union is not valuable only because it lowers financing costs. It also determines whether Europe can generate and retain technological leadership. Young firms in the United States benefit from deeper equity markets, larger venture-capital pools, and more robust exit options. European firms too often face the opposite: limited scale-up capital, lower valuations, and a greater risk of stagnating or relocating.

That matters especially in sectors such as AI, biotech, clean technology, semiconductors, and advanced manufacturing. These sectors need patient capital, risk tolerance, and the ability to raise large sums outside traditional bank lending. Without deeper capital markets, Europe will continue to produce talent and ideas but struggle to scale them into global champions.

Figure 3

The gap between the US and EU startup ecosystems shows why Europe needs deeper venture, equity, and scale-up financing if it wants to compete in frontier industries.

Source: PitchBook Venture Monitor (2020); Crunchbase European VC Report (2020); European Commission EU Industrial R&D Investment Scoreboard (2019)

This is why the SIU should be seen as part of Europe’s industrial and geopolitical strategy, not just its financial-reform agenda. Better capital allocation would support innovation, productivity, and autonomy in sectors where scale now matters enormously.

5. Quantifying the Potential Gains

The economic upside from successful implementation could be substantial. Redirecting even a modest share of Europe’s trapped savings toward productive investment would help close much of the annual investment gap identified by Draghi and others. That alone would improve Europe’s ability to finance climate infrastructure, digital transformation, defense industrial capacity, and strategic technologies.

Broader estimates suggest additional GDP gains over a decade from both price and quantity effects, with even larger upside when productivity improvements from better innovation finance are included. Better access to capital would also improve resilience by making cross-border private risk sharing stronger across the euro area.

How SIU could boost competitiveness

| Channel | Mechanism | Likely effect |

|---|---|---|

| Investment mobilization | Redirects trapped savings into markets | Helps close Europe’s annual investment gap |

| Innovation finance | Improves venture, equity, and scale-up funding | Stronger startup growth and higher productivity |

| Cost of capital | Deepens liquidity and investor base | Cheaper financing for firms |

| Risk sharing | Expands cross-border capital flows | Greater resilience in downturns |

| Household returns | Moves savings into higher-yield assets | Better pensions and long-term wealth outcomes |

Source: Article analysis based on SIU and Draghi-report framing

6. The Main Hurdles Still Standing

Despite the momentum, the barriers remain real. Political resistance to centralized supervision is still strong in parts of the EU. Tax fragmentation continues to distort investment decisions. Insolvency regimes are improving but remain uneven. And across much of Europe, households still prefer safety and liquidity over market risk.

Those constraints matter because SIU success depends not only on legislative milestones, but on implementation across all 27 member states. The agenda needs support from large economies such as France, Germany, Italy, the Netherlands, Poland, and Spain if it is to become more than a partially harmonized framework.

In that sense, the project remains unfinished. The mid-term review expected in 2027 will be important, but the real question is whether Europe can sustain political will long enough to turn the SIU into a functioning continental capital market rather than another incomplete integration effort.

7. Why the 2026 Window Matters

The EU’s strategic environment is making delay more dangerous. Europe needs much larger investment flows not only for the green and digital transitions, but also for defense, industrial resilience, energy systems, and geopolitical competitiveness. The old model of relying on fragmented national finance while hoping banks carry most of the burden is no longer sufficient.

The SIU offers a way to convert one of Europe’s biggest structural weaknesses into a structural strength. Excess savings with low returns can become a large integrated funding base for the next generation of European growth. That would lower the cost of capital, improve innovation capacity, strengthen the euro area, and enhance Europe’s global position.

Conclusion

The Savings and Investments Union is Europe’s opportunity to turn vast private savings into engines of growth, innovation, and long-term competitiveness. The alternative is continued fragmentation, underinvestment, and gradual strategic decline in a world where both the United States and China are operating at much greater scale.

Europe has the savings, the talent, and now a clearer policy framework. What it has lacked is an integrated capital market capable of mobilizing those strengths efficiently. Completing the SIU would not solve every structural problem the EU faces, but it would address one of the most important bottlenecks holding back growth, innovation, and resilience.