Why the US Dollar Has a Bearish Medium-Term Outlook in 2026

Narrowing rate differentials, weaker official-sector demand, and rising fiscal concerns are creating a structurally softer backdrop for the dollar.

OpenMacro

The US dollar’s medium-term outlook is turning bearish as yield support fades, reserve managers diversify away from dollar assets, and fiscal sustainability concerns push investors to demand a higher term premium.

he greenback’s multi-year bull run is clearly losing steam. While the USD has shown short-term volatility, recently trading around 98.8 to 100 on the DXY as of early April 2026, the medium-term outlook for the next 12 to 18 months remains structurally bearish.

Major banks and strategists, including Morgan Stanley, ING, Goldman Sachs, and J.P. Morgan, largely agree: we are entering a period of gradual but meaningful USD depreciation, especially through the second half of 2026 and into 2027.

Here’s a deeper, data-driven breakdown of the three structural forces driving this shift:

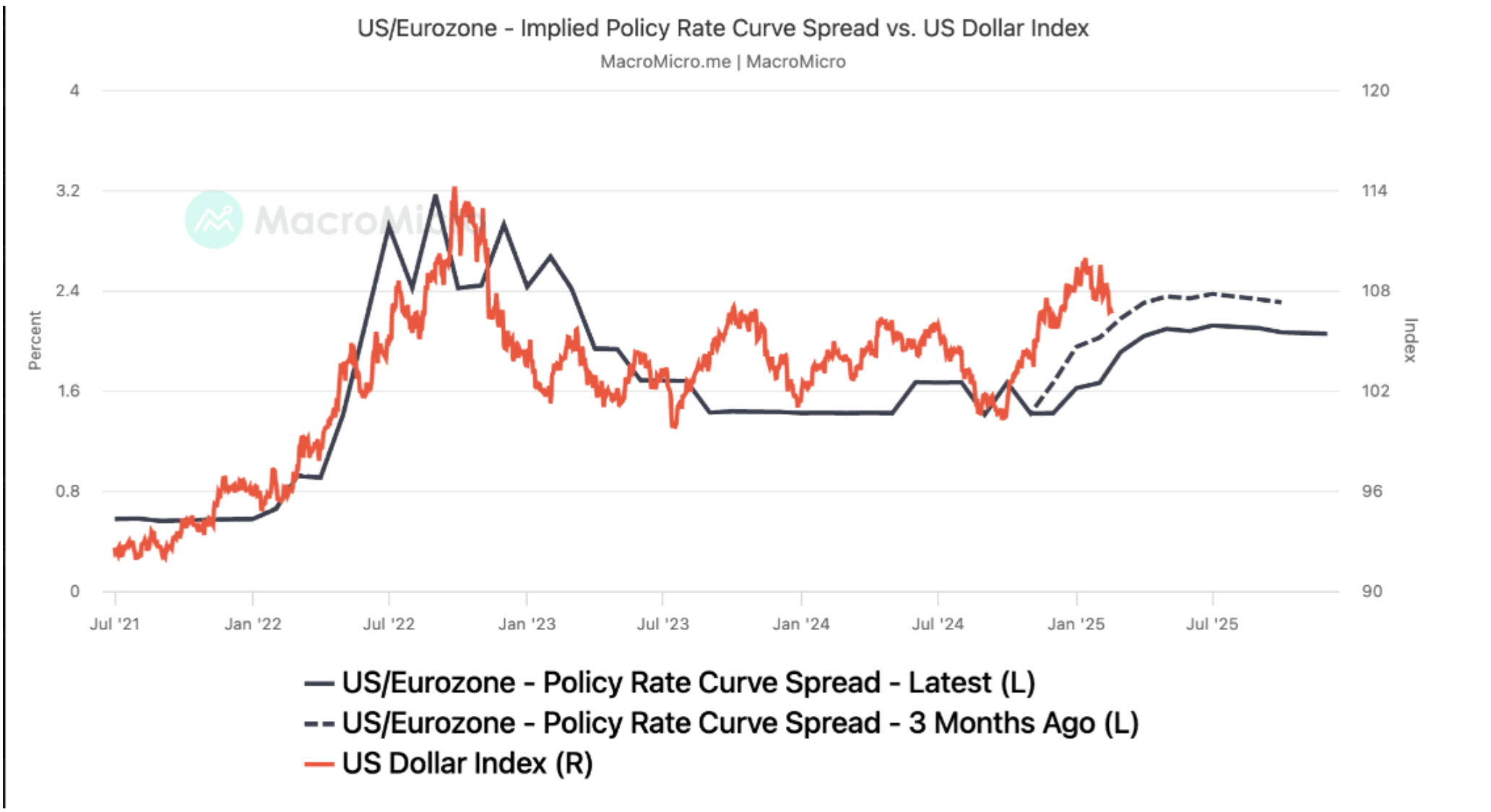

1. Narrowing Interest Rate Differentials

The dollar is losing its yield advantage faster than expected.

Forward two-year rate differentials between the United States and major peers, especially the eurozone, have already compressed to cycle lows. The Federal Reserve is widely expected to continue easing, with markets pricing in cuts toward 3.0% to 3.25% by mid-2026, while other central banks maintain relatively higher policy rates or slower easing paths.

This compression directly reduces the carry-trade appeal of USD assets. As the yield gap narrows, capital flows shift away from dollar-denominated investments, a classic driver of medium-term USD weakness.

Figure 1

Narrowing US-Eurozone rate differentials are reducing the dollar’s carry advantage and reinforcing the medium-term bearish outlook.

Source: MacroMicro.me

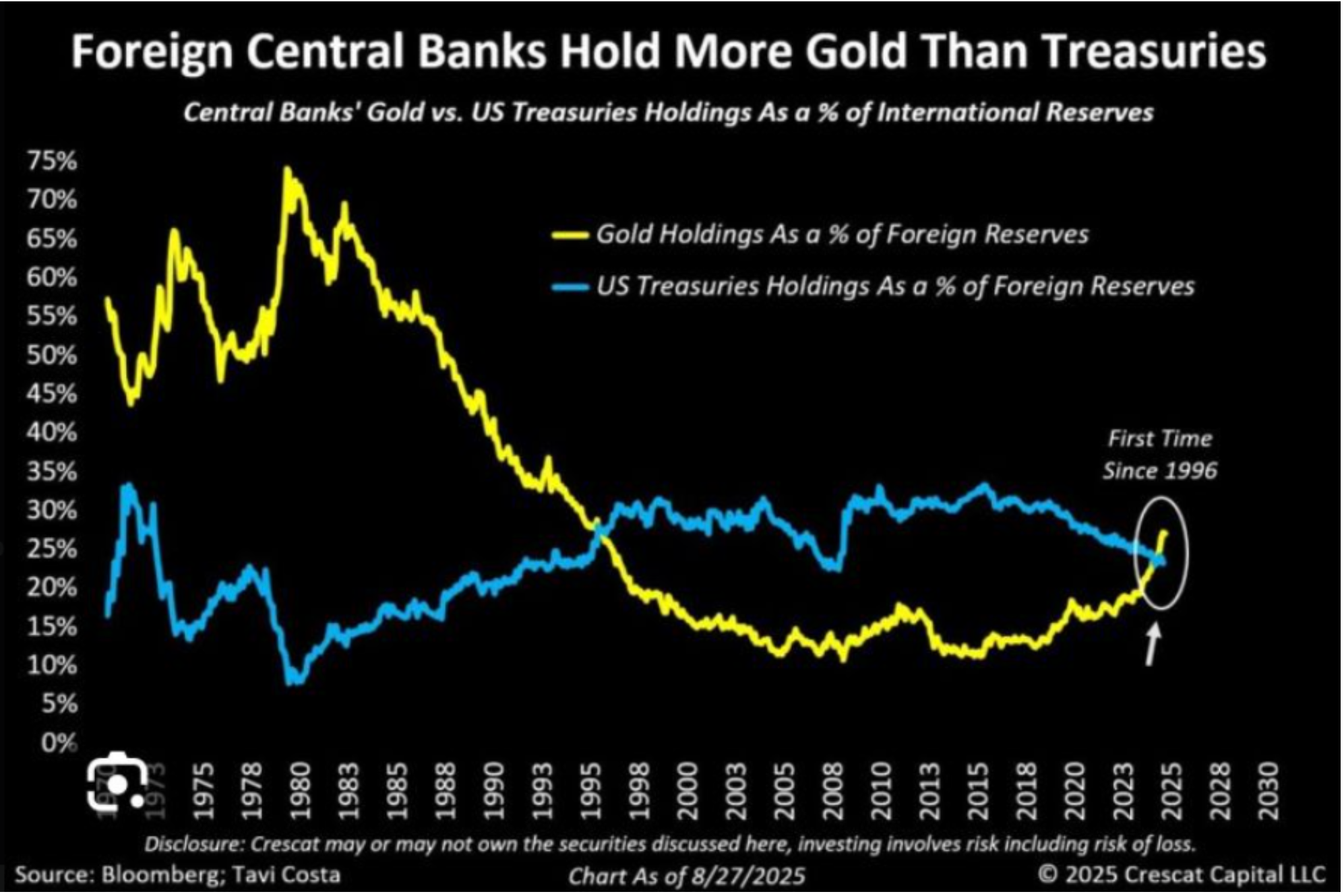

2. Falling Demand from Central Banks and Institutions

De-dollarization is real and accelerating.

The USD’s share of global official foreign exchange reserves fell to 56.8% in Q4 2025, the lowest level since 1994, according to IMF COFER data. Central banks, particularly in emerging markets, continue aggressive diversification into gold and non-traditional currencies.

Gold has now overtaken the euro to become the second-largest reserve asset globally, with foreign central banks holding more gold than US Treasuries as a percentage of reserves for the first time since 1996. This is not a sudden collapse, but a slow and powerful structural erosion of long-term USD demand.

Figure 2

Reserve diversification into gold is reducing long-term official demand for dollar assets and weakening a key structural support for the USD.

Source: Bloomberg; Tavi Costa

Markets are waking up to the fiscal reality.

US gross federal debt now stands at roughly 122% to 124% of GDP, with debt held by the public projected near 101% at the end of 2026 and rising toward 108% by 2030 under CBO projections. Annual deficits remain near 5.8% to 6.0% of GDP, while net interest payments have already climbed above $1 trillion annually and are projected to reach $2.1 trillion by 2036, or 4.6% of GDP.

Figure 3

Rising US debt-to-GDP levels are increasing fiscal risk and contributing to higher term-premium pressure on the dollar.

Source: BEA; Treasury Dept.; Wolfstreet.com

Bottom Line: A Structurally Weaker Environment for the Dollar

Lower relative yields, reduced official-sector demand, and mounting fiscal concerns are creating a fundamentally less supportive backdrop for the world’s reserve currency.

Most institutional forecasts point to:

- DXY declining toward 94 to 96 by mid-2026

- Gradual depreciation continuing into 2027

- A possible V-shaped recovery in late 2026 or 2027 if US growth reaccelerates or geopolitical risk premiums return

This is not a doomsday scenario; the dollar remains dominant. But the medium-term bias is clearly bearish, and the window for positioning is now.