Reclaiming German Power: A Blueprint for Economic, Technological, and Military Renaissance

Germany can still reclaim economic and strategic leadership, but only through coordinated action on competitiveness, capital markets, energy, defense, and European scale.

OpenMacro

Germany retains the foundations of great-power relevance, but restoring it will require a stronger industrial base, cheaper and more secure energy, deeper European capital-market integration, faster technological upgrading, and a sustained military buildup.

Germany stands at a strategic crossroads. For decades, it was Europe’s industrial engine, export leader, and fiscal anchor. But since the early 2020s, that model has come under growing pressure from energy shocks, deindustrialization risks, demographic decline, and a harsher geopolitical environment shaped by competition between the United States and China.

The core question is not whether Germany still has structural strengths. It does. The question is whether it can adapt those strengths to a new era in which cheap energy is gone, global trade is more fragmented, technological leadership is more contested, and military power matters more than it did in the post-Cold War period.

Reclaiming German power therefore requires more than cyclical recovery. It requires a systemic reset across external balances, industrial competitiveness, capital-market architecture, defense capacity, and energy economics. Germany cannot rely on its old model alone. It needs a new strategic blueprint.

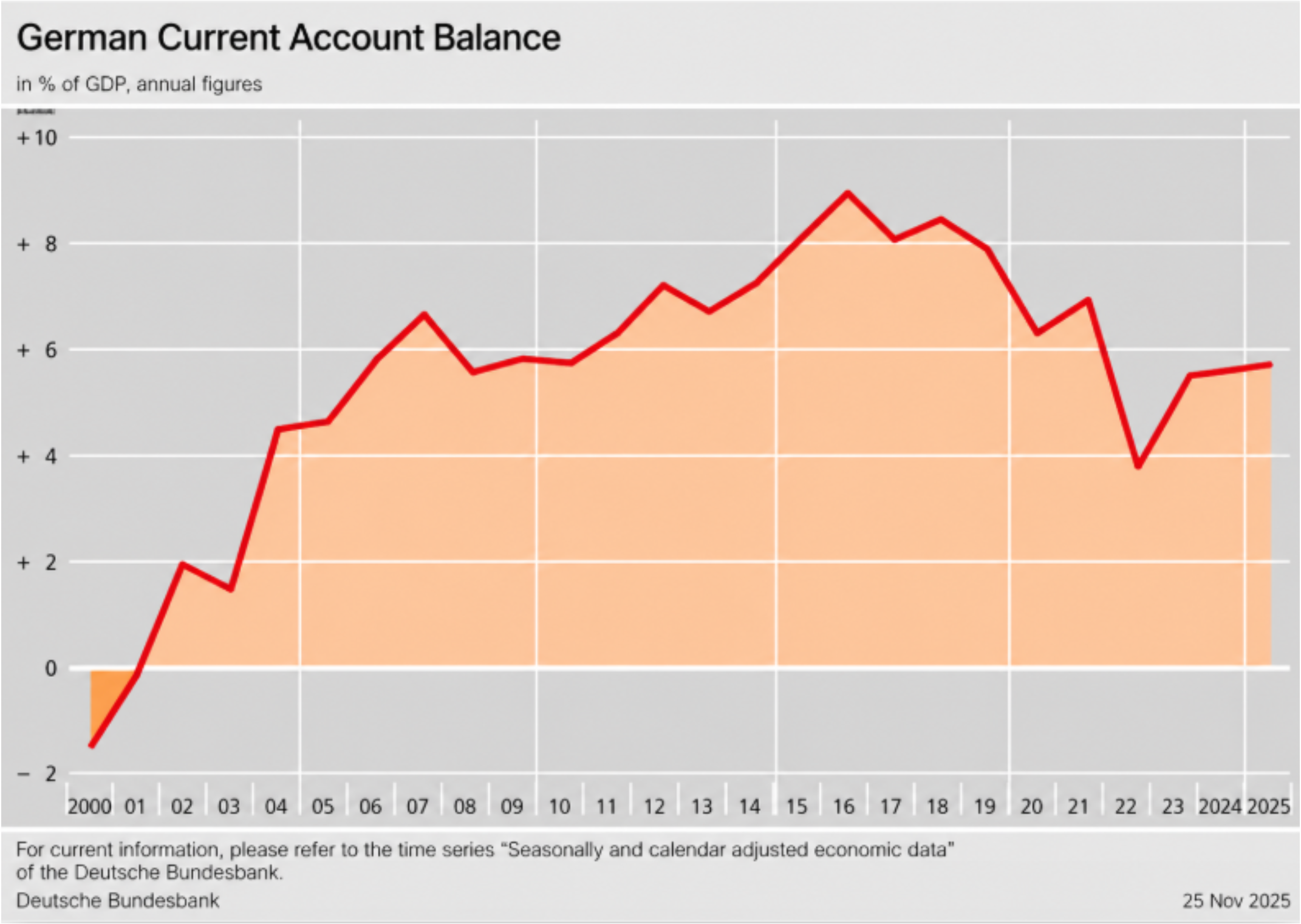

1. Fortifying the Current Account Surplus

Germany’s current account surplus remains one of its most important strategic assets. It generates external financial strength, supports long-term capital formation, and gives the country room to invest without depending on foreign savings in the same way many peers do.

Even after retreating from the extraordinary highs of the 2010s, the surplus remains large by international standards. That matters because Germany’s export base still spans world-class sectors including autos, machinery, chemicals, and precision engineering. In a more fragmented global economy, a durable external surplus is not just an accounting outcome. It is a source of resilience and influence.

Figure 1

Germany’s current account surplus remains structurally large, even after falling from earlier peaks, preserving an important pillar of national economic strength.

Source: Deutsche Bundesbank

Still, the surplus cannot be taken for granted. High energy costs, Chinese industrial competition, and supply-chain fragmentation all threaten Germany’s export machine. Preserving surplus strength will require more than export discipline. It will require reinvestment in productive capacity, smarter trade diversification, and careful monetary coordination within the euro area.

The strategic use of external strength is just as important as its preservation. Germany’s large net international investment position gives it scope to fund infrastructure, technology, and acquisitions in strategically important sectors. A stronger external balance should therefore be treated not as an end in itself, but as the financial engine of national renewal.

Current account strength as strategic leverage

| Pillar | Why it matters | Strategic use |

|---|---|---|

| Export surplus | Supports national resilience and external strength | Funds long-term investment and strategic acquisitions |

| Manufacturing base | Anchors Germany’s trade competitiveness | Sustains influence inside Europe and globally |

| Net foreign assets | Expands financial room for maneuver | Can back technology, minerals, and infrastructure strategy |

2. Restoring Competitiveness Through Technology and Industrial Upgrading

Germany’s manufacturing advantage has not disappeared, but it has weakened. Bureaucratic friction, high labor costs, and above all the energy shock have made parts of the industrial model less competitive than they once were. At the same time, Chinese overcapacity and increasingly capable foreign rivals are squeezing Germany’s traditional industrial sectors.

What is needed is not nostalgia for old industrial dominance, but a modernized version of it. Germany remains well positioned in advanced engineering, automation, and industrial know-how. The challenge is to push that base decisively into the next technological cycle through AI, robotics, digital twins, quantum research, biotech, and dual-use technologies.

A revived competitiveness model would pair large-scale R&D expansion with a more aggressive Industry 4.0 rollout across the Mittelstand. Germany’s SMEs are already strong in industrial automation; the opportunity is to turn that existing edge into a broader productivity surge. That means more capital spending, faster digital adoption, and a labor strategy that combines vocational modernization with selective high-skill immigration.

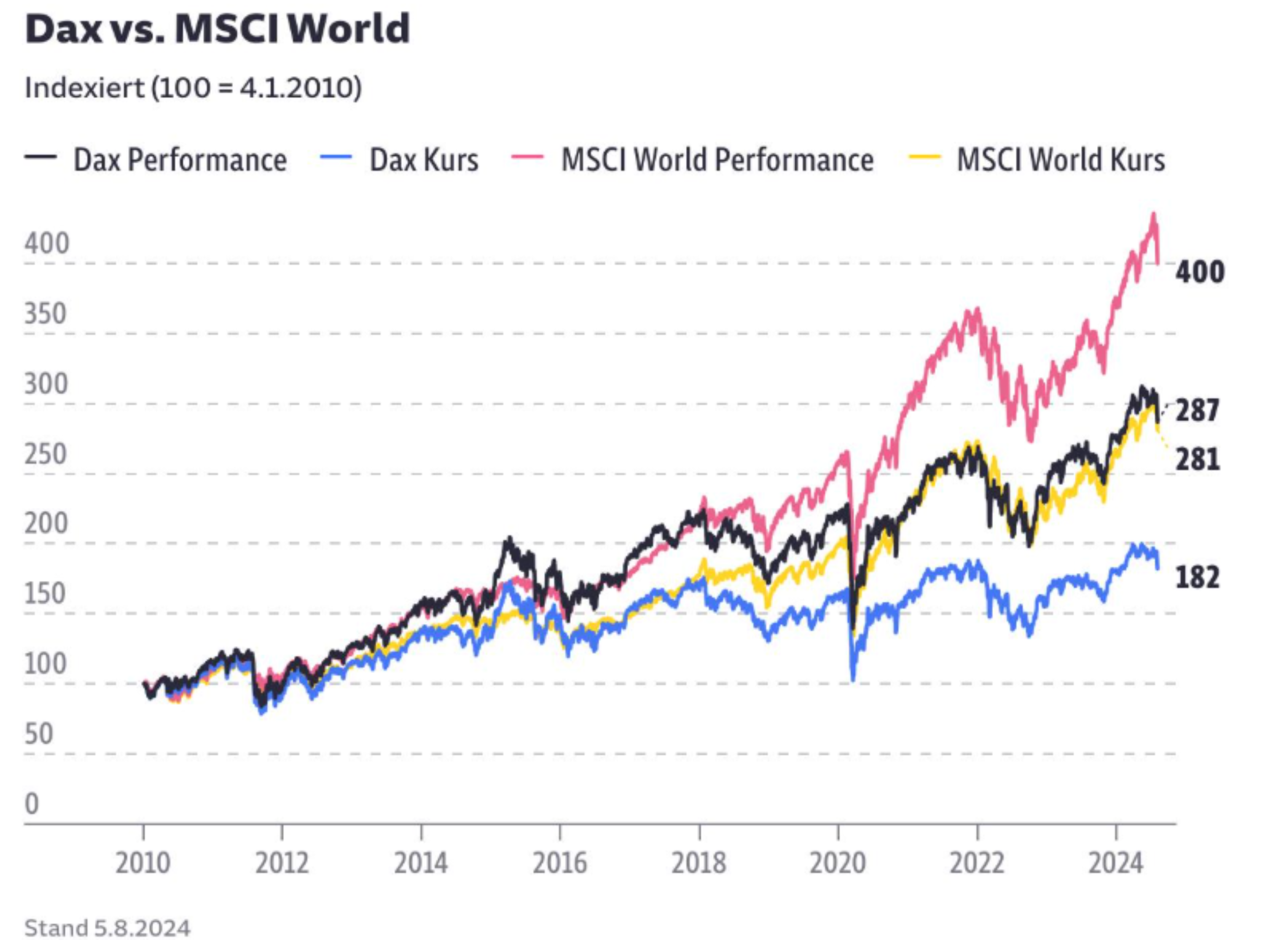

Figure 2

Germany’s market performance has remained respectable, but it still trails stronger global benchmarks, underscoring the need for a deeper competitiveness reset.

Source: OpenMacro

Current headwinds

- Bureaucratic drag

- High labor costs

- Persistent energy disadvantage

- Chinese industrial competition

- Slower manufacturing momentum

Competitiveness roadmap

- Raise R&D intensity

- Scale AI and smart-factory adoption

- Modernize vocational training

- Expand STEM-focused immigration

- Push productivity through industrial digitalization

Germany does not need to imitate Silicon Valley. But it does need to close the gap between industrial excellence and frontier innovation. If it succeeds, its productivity model can remain globally relevant. If it fails, it risks sliding from advanced manufacturer to slower-growth legacy economy.

3. Why European Capital-Market Integration Matters for German Power

Germany’s next phase of economic strength depends not only on national reform, but on European scale. The Savings and Investments Union, building on the older Capital Markets Union agenda, is one of the most important structural opportunities available to Germany.

Europe has enormous household savings, but too much of that capital remains trapped in fragmented national systems rather than flowing efficiently into productive equity, venture capital, and scale-up financing. A truly integrated European capital market would change that. For Germany, it would reduce financing frictions, deepen investment pools, improve scale-up funding, and help retain more value creation within Europe.

This matters because Germany sits at the center of Europe’s industrial and corporate system. As the bloc’s largest economy, it is positioned to capture an outsized share of the gains from harmonized insolvency rules, more unified prospectus standards, deeper securitization, and stronger cross-border investment channels.

Figure 3

Germany’s share of global equity-market weight has drifted lower over time, highlighting the need for deeper capital markets and stronger domestic value creation.

Source: Bloomberg

A deeper capital market would also help solve one of Germany’s most persistent weaknesses: the scale-up gap. The country is strong in engineering and deep-tech talent, yet still weaker than the United States in late-stage venture finance and public-market depth. A unified European market would give German firms more room to grow at home rather than seeking scale elsewhere.

4. A Unified EU Regulatory Framework Would Multiply German Strength

Capital integration works best when regulatory fragmentation falls alongside it. Today, German companies still operate across a Europe with too many legal, supervisory, and tax frictions. That raises costs and creates uncertainty, especially for startups and fast-growing firms.

A more harmonized European rulebook would reduce that burden. Standardized insolvency, more portable investment vehicles, simplified cross-border expansion, and a usable “28th regime” for European companies would make it easier for German firms to operate continent-wide as if in a single business environment.

This is especially important for Germany’s bank-centric economy. The Mittelstand still relies heavily on bank lending, which is not always the best fit for high-growth or innovation-intensive sectors. Capital-market deepening would reduce financing costs, widen the investor base, and make growth capital more available for companies moving from strong engineering niches into continental or global leadership.

The broader strategic gain is scale. If German firms can operate under effectively unified rules across the EU, Germany’s industrial base becomes even more deeply embedded in the continent’s core value chains. That would reinforce its role as Europe’s indispensable principal economy.

5. Military Renaissance and the Return of Hard Power

Germany’s strategic transformation is no longer optional. The Zeitenwende marked a political turning point, but its real significance will depend on whether the country can turn higher defense spending into durable capability, readiness, and continental leadership.

That means Germany must aim not merely to spend more, but to build Europe’s premier conventional force. Procurement, readiness, force structure, and defense-industrial scale all matter. The ambition to expand active and reserve manpower, modernize equipment, and integrate next-generation capabilities points toward a more serious German role in European security.

Figure 4

Germany’s military renewal will depend on turning higher defense spending into real readiness, larger force capacity, and stronger European strategic autonomy.

Source: OpenMacro

Phase 1 to 2029

Rapid procurement, readiness gains, and stronger equipment availability with a bias toward European supply chains.

Phase 2 to 2035

Deeper European integration through interoperable forces, joint command structures, and a more unified defense market.

Phase 3 to 2039

Technological sovereignty in AI, cyber, space, hypersonics, and autonomous systems developed largely within Europe.

A credible military renaissance also requires a longer horizon. Rapid readiness gains matter in the near term, but the larger objective is a force structure that integrates AI, cyber, space, autonomous systems, and deeper European command coordination. Germany cannot become a leading strategic actor while remaining militarily hesitant or structurally dependent on others for core deterrence.

The geopolitical implication is clear: a stronger Germany is inseparable from a stronger European pillar in defense. If Germany moves decisively, it can become the backbone of Europe’s conventional military capacity.

6. Energy Security Is the Foundation of Reindustrialization

Germany’s industrial model cannot recover fully without cheaper and more stable energy. The post-2022 scramble to diversify supply succeeded in preventing acute shortages, but it did not restore the cost advantage that once underpinned industrial competitiveness.

Even as wholesale prices have moderated, energy-intensive industry still faces costs well above US and Chinese levels. That gap continues to pressure chemicals, steel, autos, and other core sectors. In that sense, Germany’s energy problem is no longer just a supply problem. It is a structural competitiveness problem.

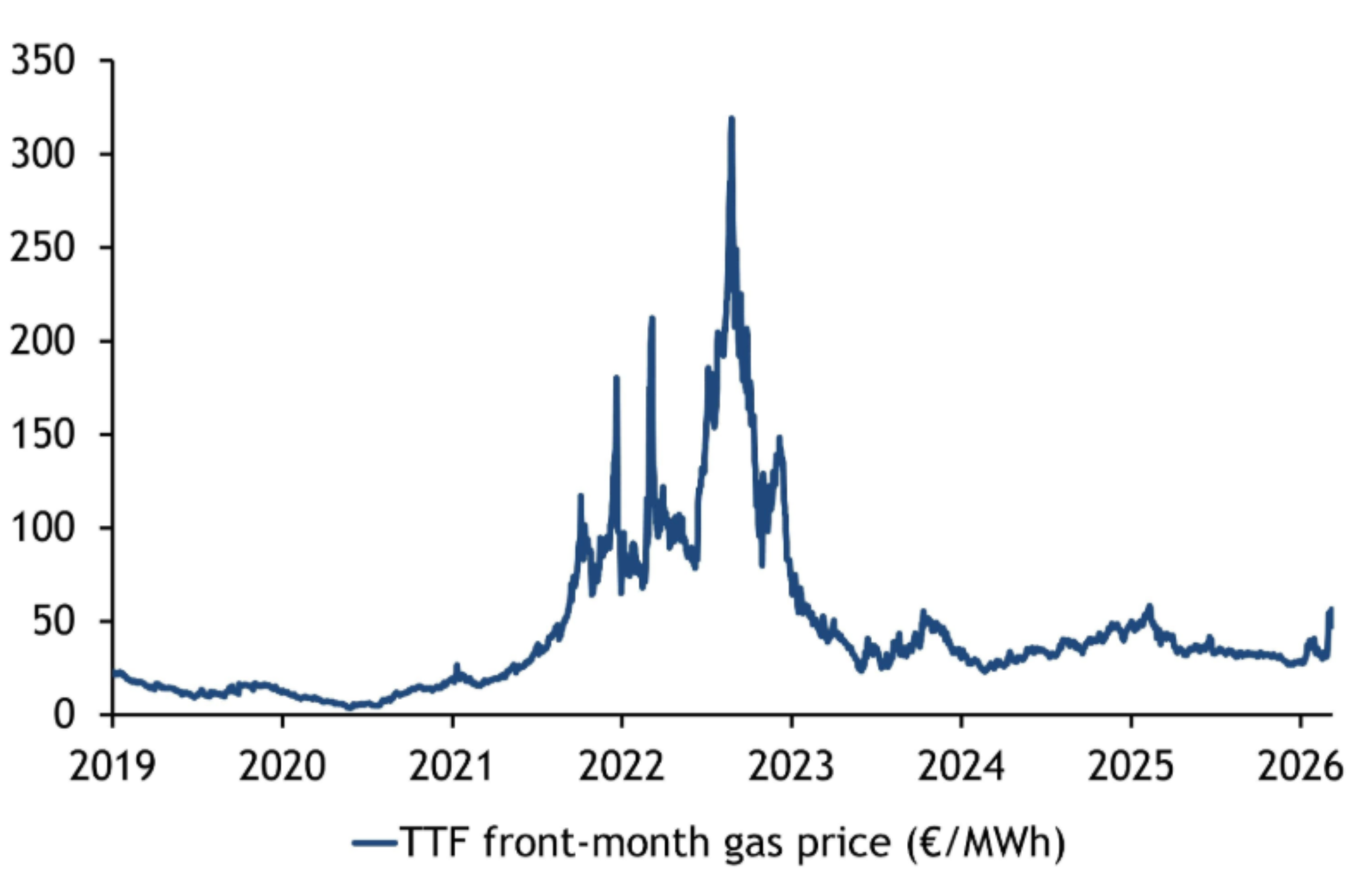

Figure 5

Although gas prices have fallen sharply from their crisis peaks, Germany still lives with the aftereffects of an energy shock that permanently altered industrial cost structures.

Source: OpenMacro

A durable solution requires more than emergency diversification. Germany needs structurally lower industrial energy costs through grid expansion, more stable baseload options, long-term LNG and hydrogen contracting, and deeper EU energy-market integration. Without that, capital will keep drifting toward lower-cost jurisdictions.

Energy policy is therefore not a side issue. It is the base layer of German industrial power. If the country cannot solve energy economics, the rest of the renaissance agenda becomes much harder to sustain.

Germany’s energy challenge

| Problem | Why it matters | Strategic response |

|---|---|---|

| High industrial power prices | Erodes competitiveness in chemicals, steel, autos | Lower structural energy costs |

| Loss of cheap pipeline gas | Permanently changed cost base | Diversify supply and secure long-term contracts |

| Grid and backup constraints | Raises volatility and system cost | Accelerate grid investment and stable baseload capacity |

| Global cost disadvantage | Encourages relocation of production | Deepen EU energy integration and domestic reform |

7. From Reluctant Leader to Strategic Enabler

Germany has long been Europe’s economic center of gravity, but it has often acted cautiously in geopolitical terms. That posture is increasingly untenable. A more fractured world requires Germany to use economic, military, diplomatic, and regulatory tools more coherently.

That means leading on EU strategic autonomy, not as an abstract doctrine but as a practical agenda. Germany should push harder for integrated defense markets, more resilient Indo-Pacific trade links, a realistic China strategy based on de-risking rather than fantasy decoupling, and a stronger alignment between national power and European scale.

This is also where domestic and continental strategies converge. Germany’s future influence depends on whether it can make Europe a larger platform for power rather than merely a larger market. The same integration that helps German firms scale also helps Europe compete with the United States and China more effectively.

Conclusion

Germany retains all the foundations necessary to reassert itself as Europe’s dominant economic and strategic power. It still has industrial depth, financial strength, institutional capacity, and a central role in the European project. But those strengths are no longer self-sustaining.

To reclaim power, Germany must reinforce its current account surplus, modernize its industrial base, exploit European capital-market integration, restore energy competitiveness, build serious military strength, and act more deliberately as a geopolitical enabler inside Europe. None of those pillars can succeed in isolation.

Economic strength finances strategic ambition. Technological leadership sustains industrial dominance. European integration provides the scale. Energy security underwrites the system. If Germany can align those pillars with speed and clarity, it will not simply stabilize decline. It will define the next phase of European power.