Australia Interest Rate Expectations

Reaccelerating inflation and a still-tight labor market are forcing the RBA to keep policy tighter for longer in 2026.

OpenMacro

Australia’s inflation rebound in 2026 has pushed the RBA back into tightening mode. With headline and trimmed mean inflation above target and unemployment still low, rate cuts have been delayed and policy is likely to stay restrictive for longer than markets expected.

Australia’s inflation challenge has intensified markedly in 2026. After some relief in late 2025, price pressures have reaccelerated, prompting the Reserve Bank of Australia to shift from easing to tightening mode with consecutive rate hikes.

Headline CPI inflation stood at 3.8% year-on-year in January 2026, slightly above expectations, while the RBA’s preferred trimmed mean, or underlying inflation, hovered around 3.4% to 3.7%.

The central bank’s February 2026 forecasts projected headline inflation peaking at 4.2% by mid-2026, with trimmed mean inflation reaching 3.7% around the same period, clearly above the 2% to 3% target band.

Inflation is now expected to moderate gradually, returning to the target range only by the end of 2026 or in 2027, and reaching the midpoint of 2.5% around 2028.

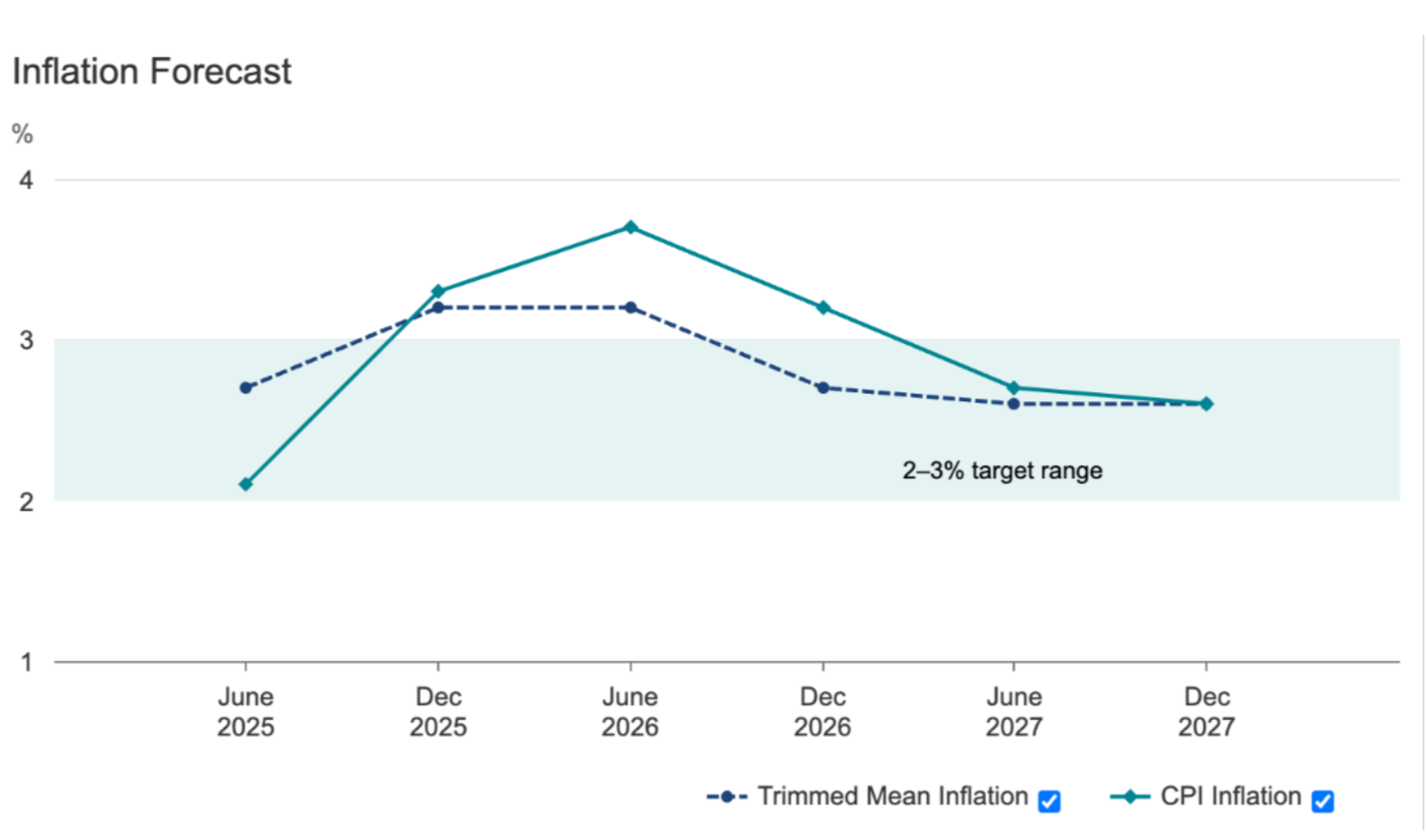

Figure 1

Australia’s inflation is projected to peak in mid-2026 and only gradually return toward the RBA’s target band.

Source: OpenMacro

The projection shows a clear peak in mid-2026 before a slow decline toward the target band.

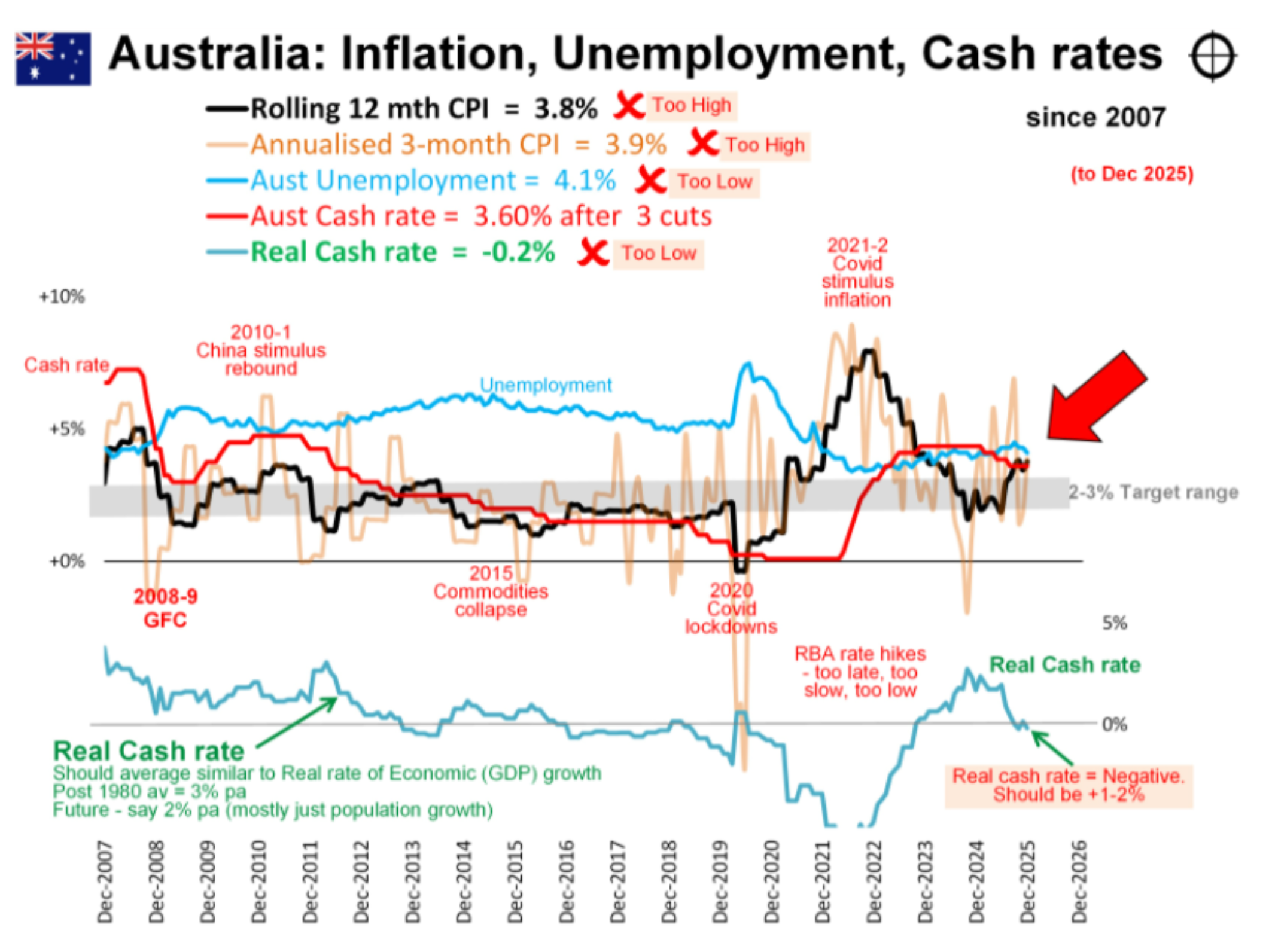

Figure 2

Australia’s recent inflation rebound and low unemployment help explain why the RBA has shifted back toward tighter policy.

Source: OpenMacro

Long-term historical chart: Australia inflation, unemployment, and cash rate from 2007 to 2026. The red arrow highlights the recent inflation rebound and rate hikes amid a still-tight labor market, with unemployment around 4.1%.

Key drivers of the stubborn inflation include:

- Renewed strength in private demand and household spending in late 2025.

- Higher energy and fuel costs linked to geopolitical tensions in the Middle East.

- Persistent pressures in housing, services, wages, and capacity constraints in the economy.

The labor market remains relatively tight, with unemployment low at around 4.1%, adding to wage and cost pressures. Economists note that risks to inflation are skewed to the upside, including through inflation expectations and global spillovers.

This sticky inflation has delayed expected rate cuts and is impacting households via higher mortgage costs, adding roughly $100 per month for an average borrower, cooling the housing market, and moderating consumer spending.

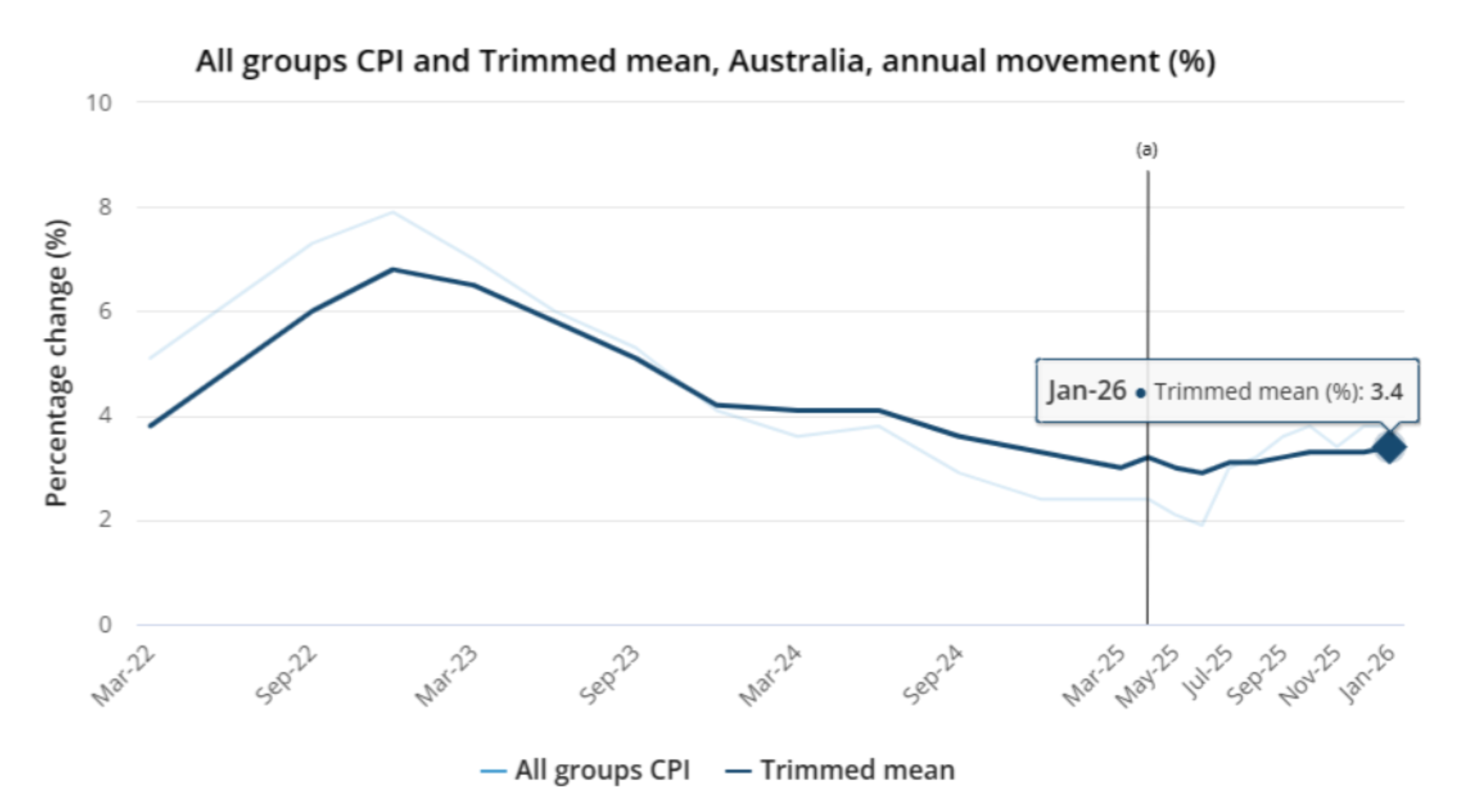

Figure 3

Trimmed mean inflation remains elevated, reinforcing the case for a tighter-for-longer RBA stance.

Source: OpenMacro

Trimmed mean inflation trends versus the RBA cash rate show that underlying inflation remains elevated relative to target.

In summary, Australia is navigating a renewed inflation surge that requires tighter monetary policy for longer than anticipated earlier in the year. The RBA’s data-dependent approach will be closely watched, especially amid global uncertainties from energy markets.

This environment poses challenges for borrowers, businesses, and overall economic growth in 2026.