Central Banks Trapped: Is the Global Rate-Cut Cycle Dead in 2026?

The 2026 oil shock has revived inflation pressure and forced central banks to reconsider the aggressive easing path markets had expected.

OpenMacro

Expectations for a broad 2026 rate-cut cycle have been sharply scaled back as high oil prices revive inflation risks. Central banks now face a narrow path between protecting growth and preventing inflation expectations from becoming unanchored.

Only two months ago, consensus expectations pointed to four to five rate cuts from the Federal Reserve and ECB in 2026. That narrative has now been completely rewritten.

The sustained surge in oil prices caused by the Hormuz disruptions has reignited inflation fears, pushing central banks into a difficult wait-and-see posture. Energy costs flow quickly into transportation, manufacturing, and food prices, making core inflation more persistent than many policymakers had anticipated.

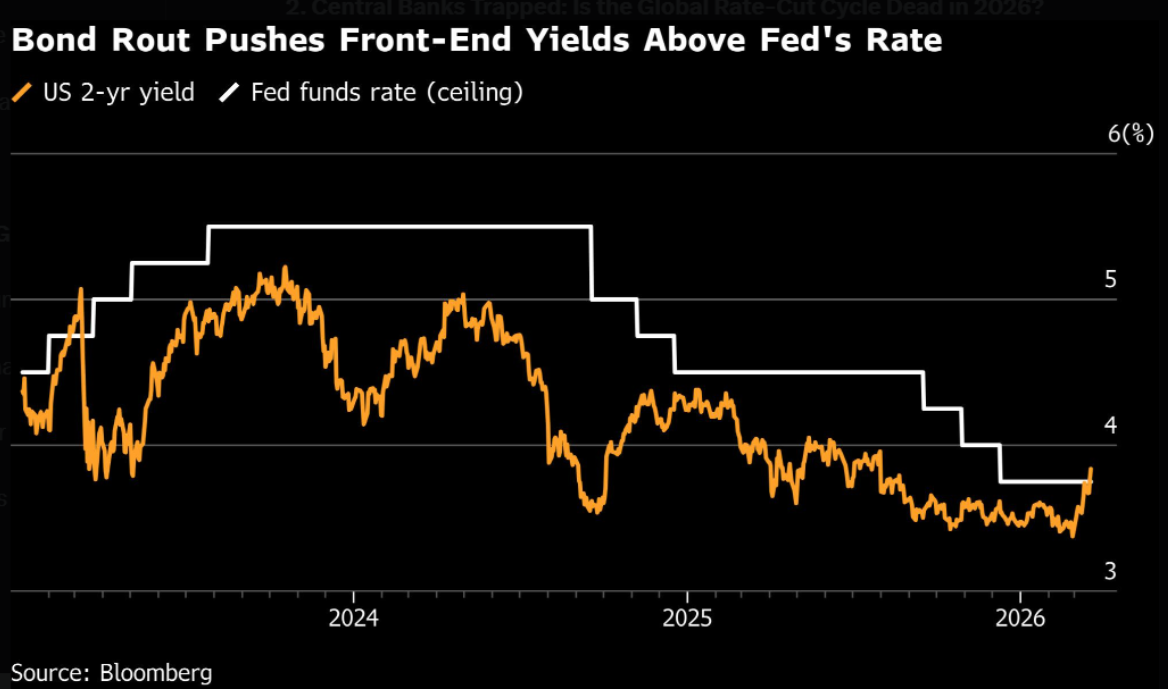

Bond markets have reacted forcefully. Front-end yields have risen sharply, and rate-cut probabilities for 2026 have been slashed or pushed further into the future. The ECB has already signaled a delay in its first cut, while Fed officials are now emphasizing data dependence and caution.

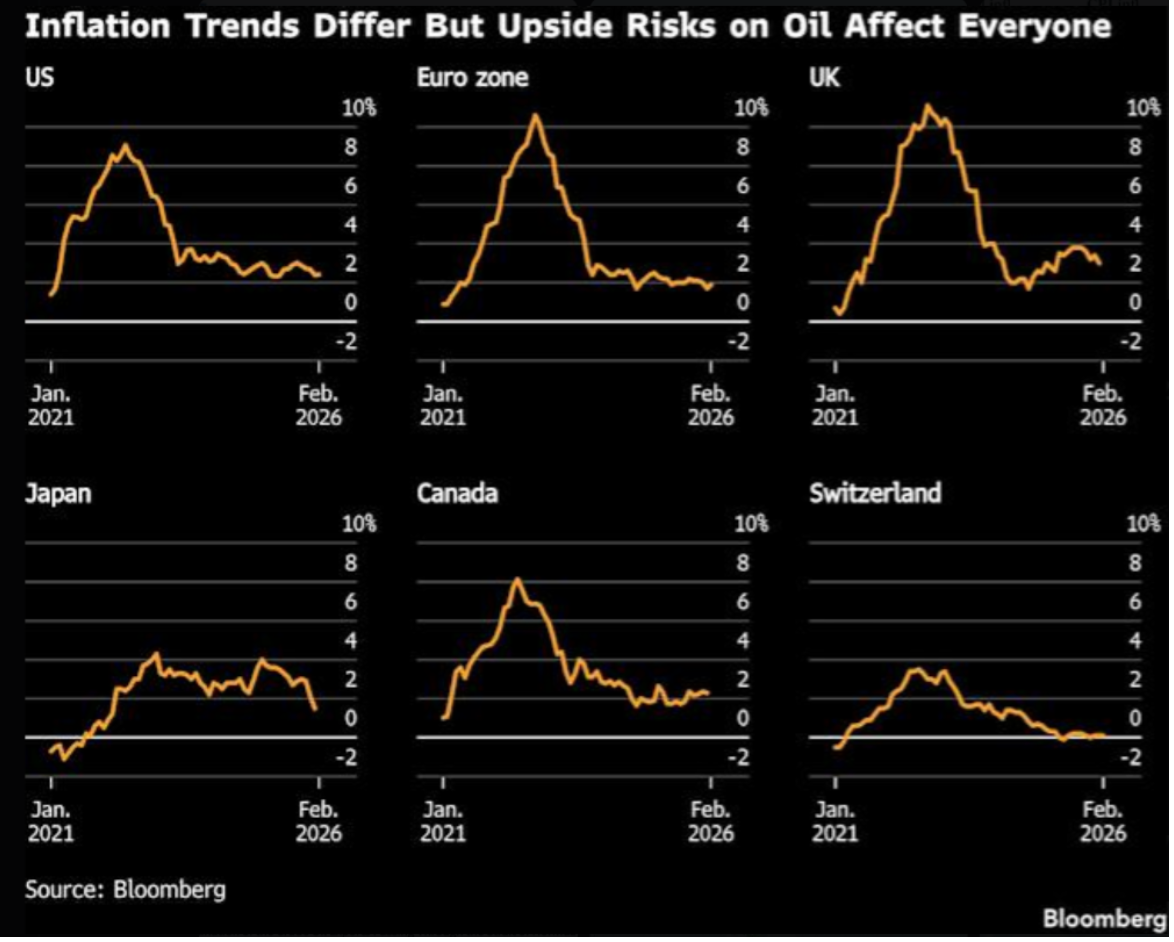

Figure 1

Inflation trends across the US, euro zone, UK, Japan, Canada, and Switzerland show different paths, but all remain exposed to upside oil-price risks.

Source: Bloomberg

This creates a painful trap for monetary authorities. Cutting rates too early risks letting inflation expectations rise, while keeping policy tight risks tipping fragile economies into recession. With global growth already being revised lower, the margin for error is extremely thin.

Emerging-market central banks face an even tougher challenge. Many have already paused or reversed easing cycles to defend their currencies against a stronger US dollar and capital outflows triggered by higher oil prices.

The long-awaited global easing cycle that investors were counting on to support risk assets may now be postponed or significantly reduced in scope. Higher-for-longer interest rates combined with higher-for-longer oil prices create a challenging backdrop for highly leveraged sectors and growth-sensitive equities.

Bottom line: The 2026 oil shock has effectively killed the easy-money narrative for this year. Central banks are trapped between inflation control and growth support, and markets will have to adjust to a less dovish policy environment than previously expected.