China’s Deepening Economic Malaise: Deflationary Risks and a Persistent Real Estate Crisis

China’s 2026 slowdown looks increasingly structural, with deflation, a prolonged property slump, weak confidence, and demographic decline reinforcing one another.

OpenMacro

China’s economic weakness in 2026 is being driven by structural forces, not a short-term slowdown. A persistent real estate crisis, weak inflation, overcapacity, debt stress, and rapid aging are combining to drag on growth, confidence, and household wealth.

China’s economic troubles in 2026 are no longer easy to dismiss as a temporary slowdown. While Beijing continues to emphasize resilient 5% growth in 2025 and projects modest expansion in 2026, many analysts argue that the headline figures obscure deeper structural weakness beneath the surface. Household confidence remains badly damaged, youth unemployment is elevated, and the hoped-for transition from investment-led growth to a more consumption-driven model has stalled.

What makes the current moment more consequential is that China’s problems are feeding into one another. The real estate bust is eroding household wealth and local-government revenues. Weak demand is amplifying disinflation and deflation risk. Industrial overcapacity is squeezing profits and worsening competitive pressures. And all of this is unfolding against the backdrop of an aging and shrinking population.

This is why the current slowdown matters far beyond the next quarter or two. China is not simply losing momentum. It is entering a more difficult structural transition that could redefine both its domestic growth model and its role in the global economy.

The Real Estate Crisis Remains the Central Drag

China’s property sector was once one of the core engines of national growth, directly and indirectly accounting for a very large share of economic activity. That engine is now broken. The downturn that began after the “three red lines” debt curbs and the Evergrande collapse has stretched into a multi-year crisis with no convincing end in sight.

New home sales, prices, and construction starts continue to weaken. National property prices remain far below their 2021 peaks, and large developers continue to struggle with debt, unfinished projects, and collapsing market confidence. The result is not just a sectoral adjustment. It is a broad macroeconomic drag that affects growth, investment, local-government finance, and household wealth all at once.

Figure 1

Unfinished apartment blocks and weak demand have turned parts of China’s property boom into a visible symbol of stalled growth and broken confidence.

Source: LSEG DataSTream | Jan 19, 2026 | REUTERS

The damage runs deeper than pricing alone. China faces a massive stock of unsold and vacant housing, along with millions of unfinished pre-sold units. That has undermined trust in the property model itself. Buyers who once saw housing as the safest store of wealth have instead faced delays, bankruptcies, and incomplete developments.

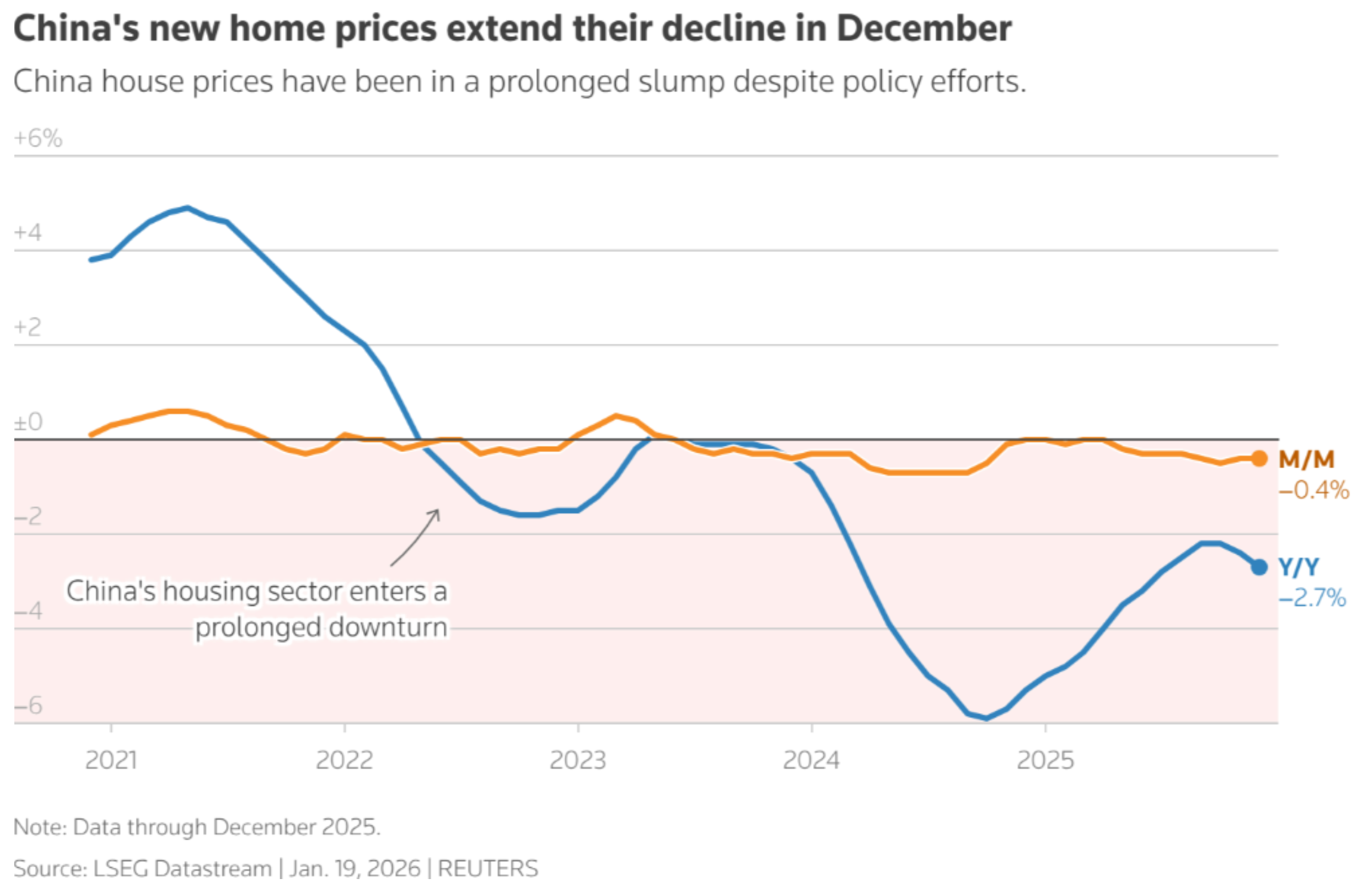

Figure 2

Unfinished apartment blocks and weak demand have turned parts of China’s property boom into a visible symbol of stalled growth and broken confidence.

Source: OpenMacro

The sector is also undergoing a harsh restructuring. Many private developers and construction firms are likely to disappear or be absorbed, while state-backed players take a larger role. Property investment has fallen sharply as a share of GDP, removing one of the country’s most important growth drivers. At the same time, local governments that once relied heavily on land sales are facing growing fiscal pressure.

The property slump matters because it reaches far beyond construction. It weakens household balance sheets, depresses confidence, strains local finance, and locks the broader economy into a weaker demand environment.

Deflationary Pressures Are Becoming More Structural

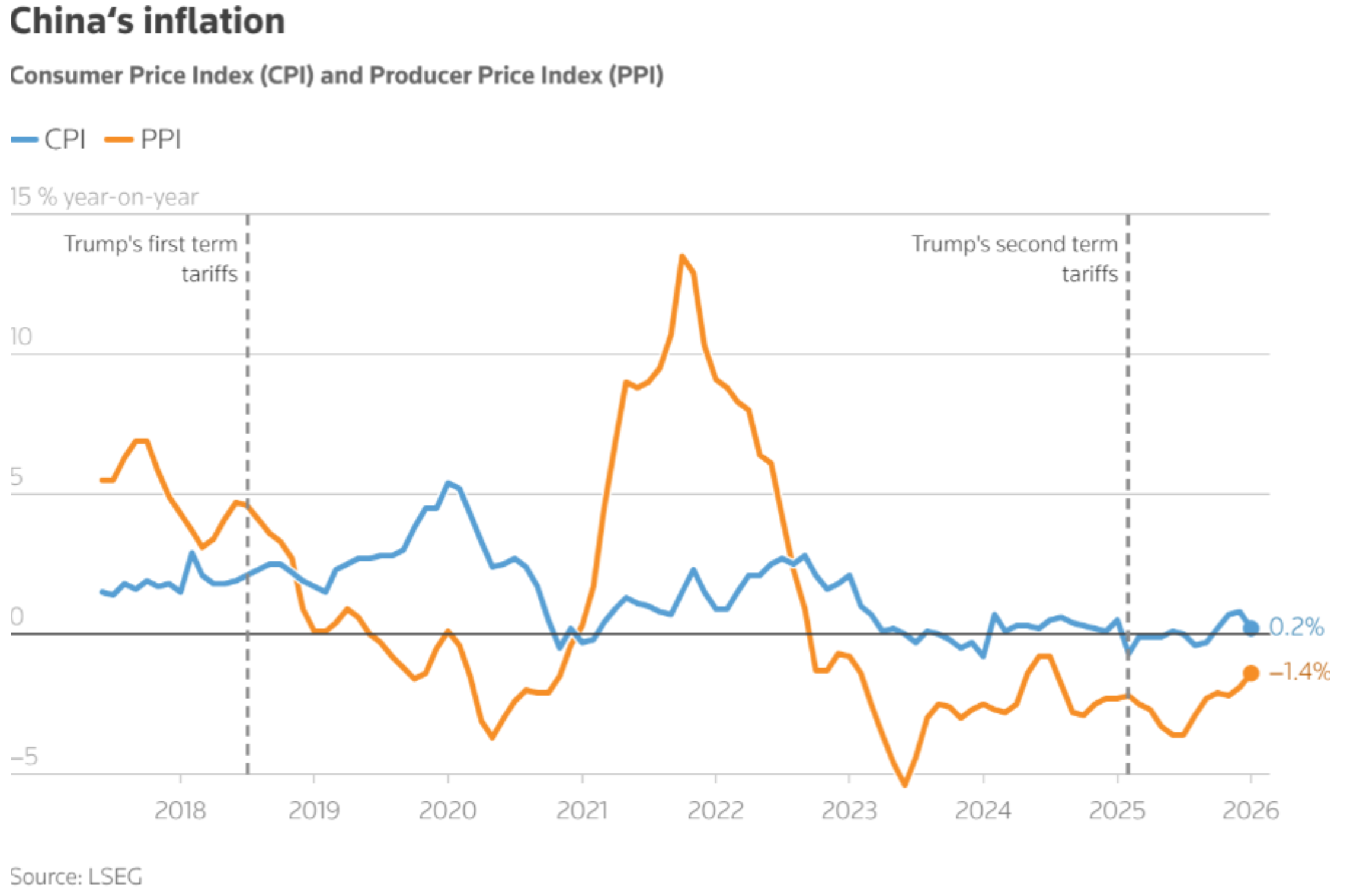

China’s property crisis is unfolding alongside an extended period of disinflation and deflationary pressure. Producer prices spent years in decline before turning slightly positive in March 2026, and that rebound appears to reflect external energy effects more than a genuine domestic recovery. Consumer inflation remains weak, and core inflation is even softer.

Figure 3

China’s housing downturn remains entrenched, with new-home prices still falling despite repeated policy efforts to stabilize the market

Source: Reuters / LSEG Datastream

This is the hallmark of an economy struggling with insufficient domestic demand. Households remain cautious, firms face overcapacity, and profits are under pressure. When expectations of weaker prices and weaker income become embedded, spending gets delayed and deflation becomes self-reinforcing.

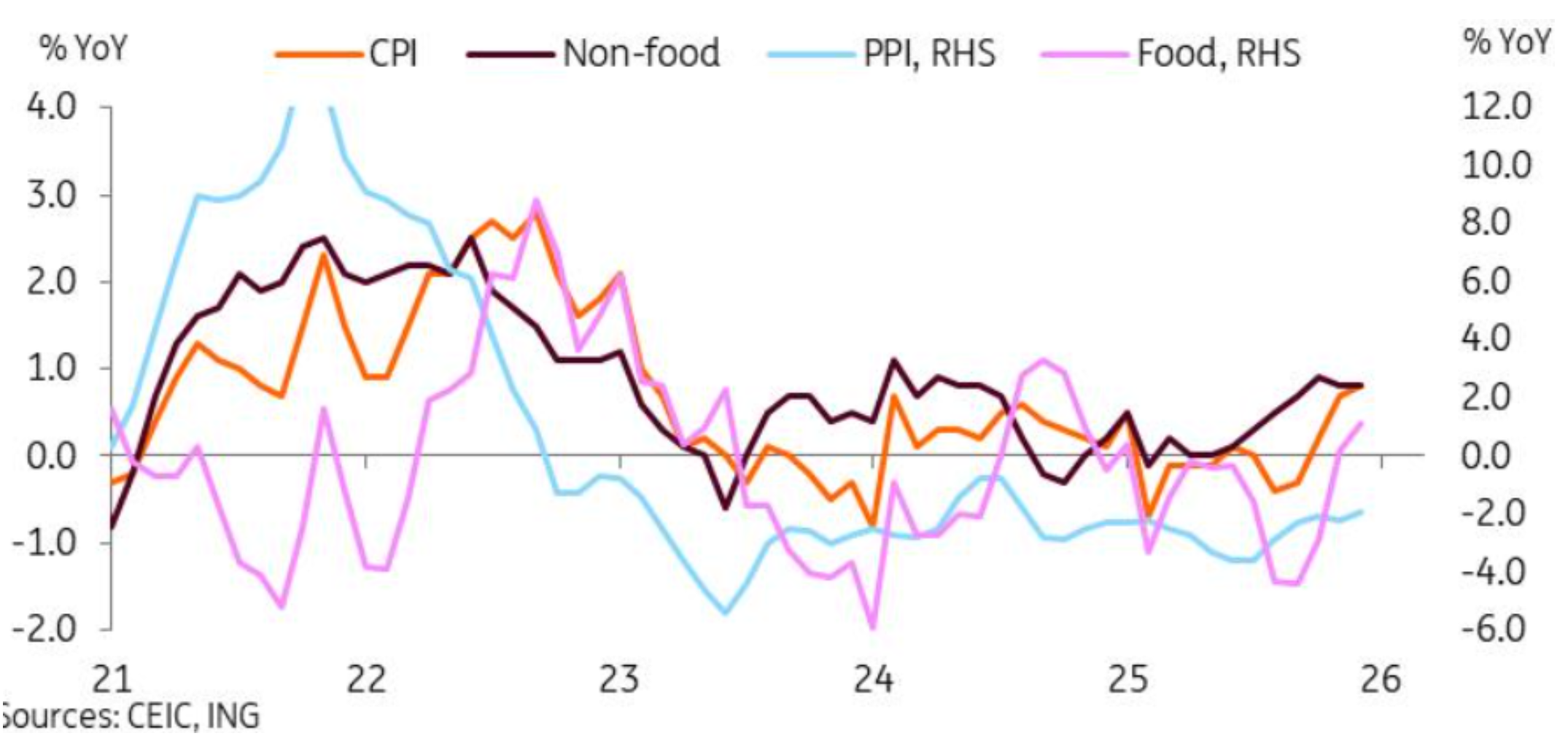

A second inflation chart reinforces the same pattern. Consumer inflation remains low, non-food price pressure is subdued, and producer prices have been consistently weak. This suggests that China’s inflation problem is not merely about one or two volatile components. It reflects broad economic softness.

Figure 4

China’s inflation indicators point to a broader demand problem, not just isolated price volatility, with weak core dynamics and prolonged producer-price weakness.

Source: CEIC; ING

Beijing’s lower inflation target for 2026 reflects this reality. The problem is no longer overheating or excessive price growth. It is that the economy risks settling into a pattern of weak demand, weak pricing power, and weak income growth.

Overcapacity, Debt, and Weak Confidence Are Locking In the Slowdown

China’s broader growth model is now part of the problem. Years of state-directed investment and industrial expansion have produced chronic overcapacity in sectors ranging from steel and solar to electric vehicles and semiconductors. That strategy has supported exports, but it has also intensified domestic price competition and weakened profitability.

At the same time, debt burdens are narrowing the government’s ability to respond aggressively. Local government financing vehicles carry massive obligations, while many state-linked or low-productivity firms remain alive through subsidies and implicit support. That prevents capital from being reallocated efficiently and leaves the economy with too many weak balance sheets and too little dynamic private-sector confidence.

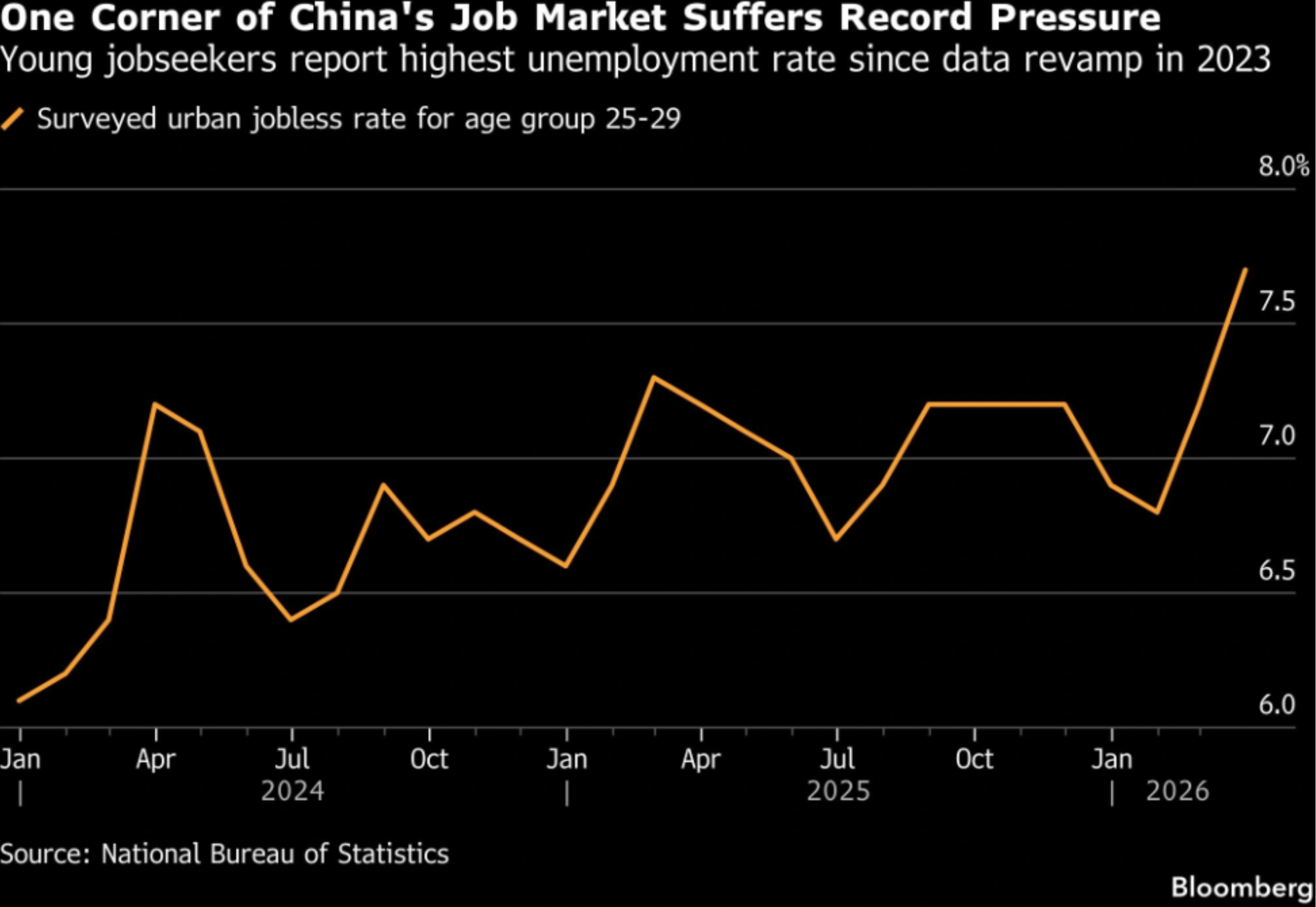

The labor market reflects this strain. Youth and young-adult unemployment remain elevated, especially in urban areas where expectations were once strongest. Confidence in private-sector opportunity has deteriorated as firms cut hiring and investment.

Figure 5

Persistent weakness in the labor market, especially for younger workers, is reinforcing household caution and undercutting consumption-led recovery.

Source: Bloomberg; National Bureau of Statistics

Weak confidence is not abstract. It is visible both in the labor market and in social frustration tied to unfinished homes, weaker wages, and fewer reliable paths to upward mobility.

Figure 6

Social frustration and falling trust have become part of the economic story, especially as households confront unfinished housing projects and weaker prospects.

Source: OpenMacro

Together, these factors create a difficult equilibrium: weak demand, too much supply, too much debt, and too little confidence in future income growth.

The Demographic Crisis Makes Rebalancing Harder

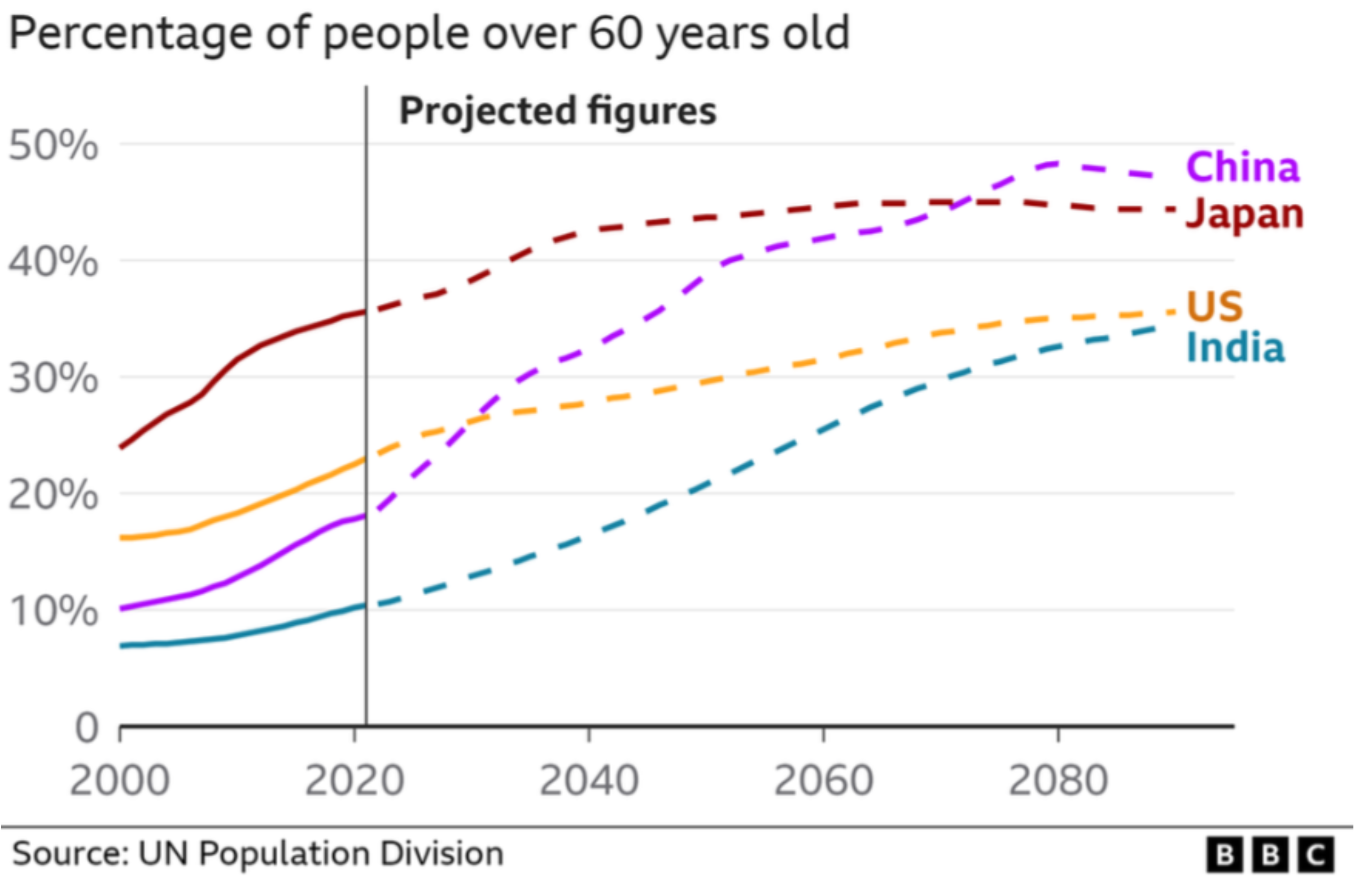

China’s most intractable challenge may be demographic. The population is shrinking, births have fallen to record lows, and the share of older citizens is rising rapidly. These are not distant issues. They are already influencing labor supply, household formation, consumption patterns, pension burdens, and fiscal sustainability.

The working-age population has been shrinking for years, while the retirement-age population continues to rise. Over time, that reduces the economy’s natural growth rate and makes demand-side recovery harder. Fewer younger households also mean structurally weaker support for housing demand, which feeds directly back into the real estate crisis.

Figure 7

China’s aging population is accelerating quickly, adding long-term pressure to growth, fiscal sustainability, and the future path of housing and consumption.

Source: BBC; UN Population Division

Policies aimed at boosting births have so far done little to reverse the trend. High living costs, economic uncertainty, and shifting social norms are all working against a demographic rebound. That leaves China facing a slower-growing and older society at the same moment it is trying to stabilize a property bust and revive confidence.

These Problems Reinforce One Another

China’s economic weaknesses do not sit in isolation. The property slump erodes wealth and confidence. That weakens consumption and contributes to disinflation. Overcapacity intensifies downward price pressure and compresses profits. Debt burdens reduce the flexibility of local governments and weaker firms. Demographic decline makes it harder to reignite housing demand or sustain long-term consumption growth.

This is what makes the current moment so important. China still retains major strengths in manufacturing scale, state capacity, infrastructure, and parts of the high-tech sector. But those strengths are increasingly offset by structural drags that are proving difficult to reform away.

Beijing has responded with targeted easing, selective support for housing, and repeated calls for rebalancing toward consumption and advanced industry. Yet the reforms needed are deeper: higher household income support, cleaner resolution of bad property debt, a more credible revival of private-sector confidence, and a more durable answer to local government fiscal stress.

Conclusion: A Critical Juncture for China’s Growth Model

China’s economic malaise in 2026 reflects a structural turning point rather than a temporary loss of momentum. Deflation risks, a prolonged real estate correction, entrenched overcapacity, weak confidence, and rapid demographic aging are all weighing on the economy at once.

The danger is not just slower growth in one year. It is the risk of a prolonged period in which weak demand, weak pricing power, and weak confidence become embedded. China retains formidable capabilities, but its old model is delivering diminishing returns and its new one has yet to fully emerge.

For households, the effects are already tangible: falling property values, reduced job security, and growing uncertainty about future prosperity. The years ahead will determine whether Beijing can engineer a genuine rebalancing or whether these headwinds will define a more subdued era for the Chinese economy.