How the 2026 Oil Price Shock Is Bolstering Brazil’s Economy

Higher crude prices are strengthening Brazil’s trade balance, supporting the real, improving external accounts, and delivering fiscal and investment gains.

OpenMacro

The 2026 oil shock is benefiting Brazil by boosting crude export revenues, widening the trade surplus, supporting the real, improving the current account, and lifting fiscal receipts. As a low-cost pre-salt producer, Brazil is emerging as one of the clearest macroeconomic winners from higher oil prices.

In 2026, the global oil market has been jolted by a major supply shock tied to escalating tensions in the Middle East and disruptions around the Strait of Hormuz. Brent crude has moved well above $100 per barrel, far above the levels embedded in many earlier forecasts. For oil-importing economies, that shock has raised inflation and growth concerns. For Brazil, however, the same surge has become a powerful macroeconomic tailwind.

That shift reflects how much Brazil’s energy profile has changed over the past two decades. Once more vulnerable to oil-price spikes, Brazil now enters this period as a major crude exporter with large, low-cost pre-salt production. The result is a clear terms-of-trade gain: higher export earnings, stronger foreign-exchange inflows, improved external balances, and increased fiscal revenue.

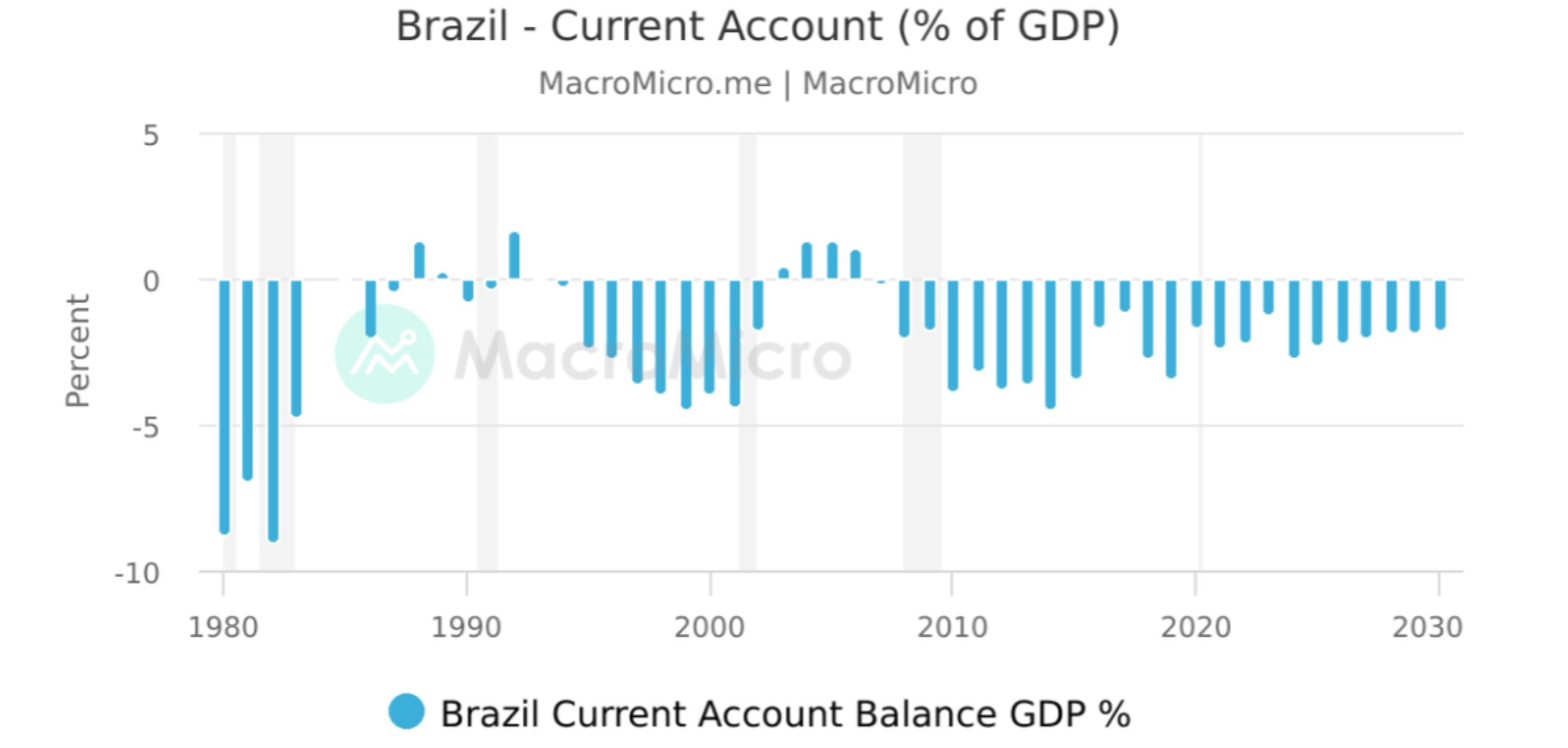

Figure 1

Brazil’s current account has typically remained in deficit, but stronger oil export revenues help narrow that gap and improve external resilience.

Source: MacroMicro

The benefits are not limited to the oil sector itself. A stronger trade balance supports the Brazilian real, improves current-account dynamics, and gives policymakers a more stable macroeconomic backdrop. At a time when many countries are absorbing the pain of higher energy prices, Brazil is instead capturing a significant share of the upside.

Brazil’s Rise as a Net Oil Exporter

Brazil’s position in the current oil shock is the product of a long structural transformation. The discovery and development of pre-salt reserves in the Santos and Campos basins changed the trajectory of the country’s energy sector, turning Brazil from a more vulnerable importer into one of the world’s major crude exporters.

By early 2026, Brazil’s oil production had reached record levels of roughly 4.1 million barrels per day, with pre-salt fields accounting for the overwhelming majority of output. These reserves are especially valuable because they tend to produce light, low-sulfur crude and remain commercially attractive even in volatile markets, with many projects sitting well below current oil prices on a breakeven basis.

That production base gives Brazil unusual resilience. When global prices rise sharply, the country is no longer primarily exposed through higher import costs. Instead, it captures the upside through larger export receipts and stronger sectoral cash flow. This is the core reason Brazil is emerging as one of the clearest beneficiaries of the 2026 oil shock.

Figure 2

Record trade-surplus figures underline how higher oil prices are strengthening Brazil’s external accounts and boosting export earnings.

Source: IndexBox Market Intelligence

Oil Revenues Are Driving a Larger Trade Surplus

The first and most visible benefit has been in the trade balance. Higher crude prices, combined with strong export volumes, have sharply increased the value of Brazil’s oil shipments abroad. In the first quarter of 2026, crude exports rose strongly year over year, helping drive a record oil and fuels surplus and contributing to one of the strongest trade performances in the region.

This matters because oil has become a much larger driver of Brazil’s overall external position. In a high-price environment, every additional barrel exported brings in more foreign exchange, and that income feeds directly into the trade balance. With oil and fuels accounting for a large share of the surplus, analysts have revised full-year trade expectations higher.

The broader implication is that Brazil now enjoys a stronger external buffer in moments of geopolitical stress. While many economies see their trade accounts deteriorate when energy prices rise, Brazil sees the opposite. That is a strategic advantage, not just a cyclical gain.

How higher oil prices help Brazil’s external accounts

| Channel | Oil shock effect | Macro result |

|---|---|---|

| Crude export revenues | Higher realized prices and robust export volumes | Larger trade surplus |

| Foreign-exchange inflows | More dollar receipts from commodity exports | Support for the BRL |

| Goods balance | Oil surplus offsets weakness elsewhere | Better current-account dynamics |

| Fiscal income | Higher royalties, dividends, and fees | Stronger public revenues |

Source: Based on the article’s analysis and cited 2026 trade and production trends

Why the Brazilian Real Benefits

Higher oil prices have also supported the Brazilian real. As export revenues rise and more hard currency flows into the country, Brazil’s balance of payments improves, increasing demand for the BRL. This is a classic commodity-currency effect, but in Brazil’s case it is amplified by the scale of the pre-salt sector and the country’s broader commodity exposure.

In April 2026, the real strengthened to its firmest levels in more than two years, helped by better terms of trade and continued investor appetite for Brazil’s yield advantage. That has allowed the currency to hold up relatively well even during periods of broader emerging-market volatility.

A firmer currency brings secondary benefits. It helps reduce imported inflation pressure, improves confidence in external sustainability, and gives the central bank a somewhat more favorable environment in which to manage the inflation consequences of the global oil shock. Brazil is still exposed to energy-related price pressures, but far less destructively than economies that rely heavily on imported crude.

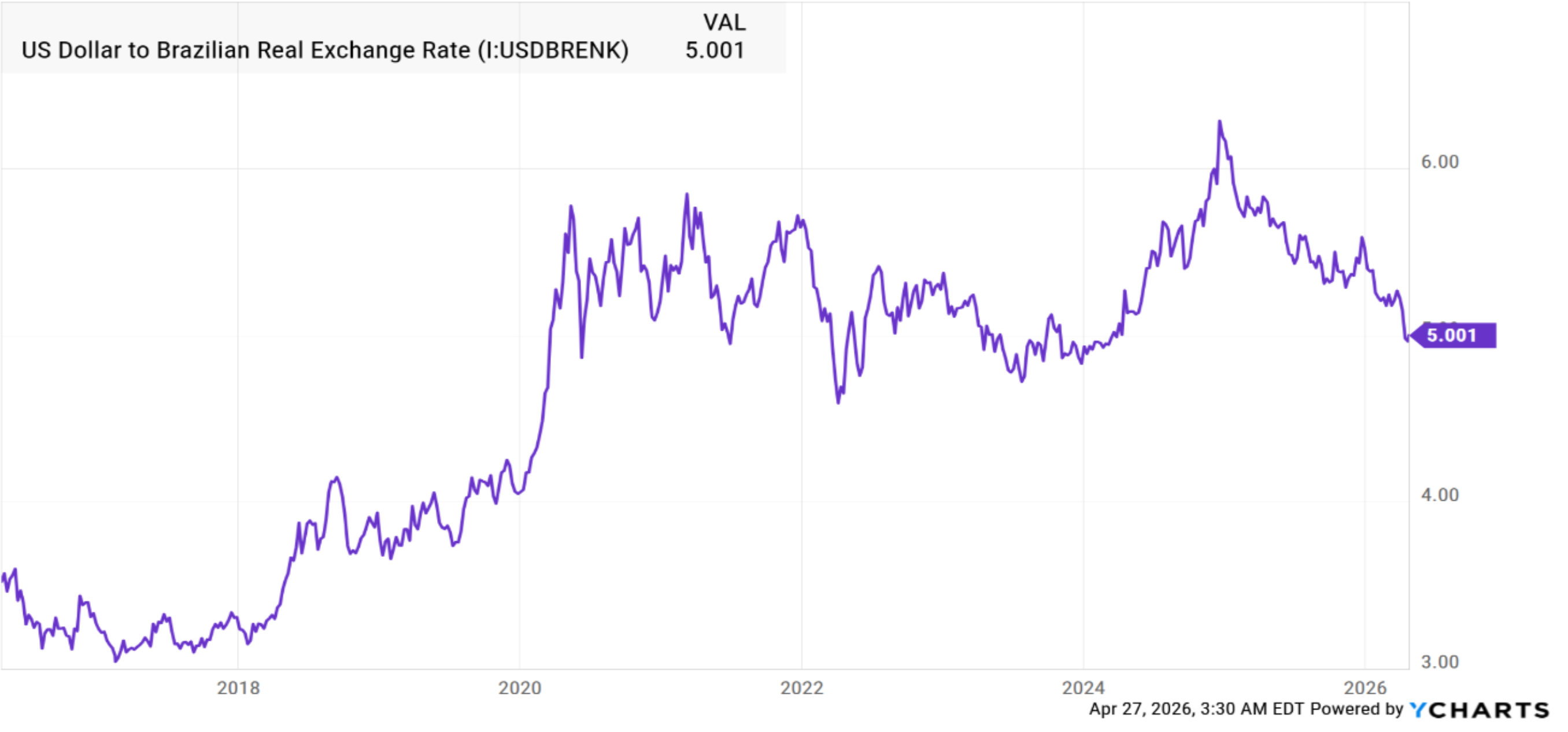

Figure 3

Stronger commodity revenues and better terms of trade have helped support the real, reinforcing Brazil’s position as a net beneficiary of the oil shock.

Source: YCharts

The Current Account Improves Even If It Does Not Fully Flip

Brazil has long tended to run current-account deficits because goods surpluses are offset by outflows in services, profits, and dividends. The oil shock does not eliminate those structural features, but it does make the external picture healthier by strengthening the trade balance.

That effect is especially important in a volatile global environment. A narrower current-account deficit reduces dependence on external financing and improves perceptions of resilience. Analysts increasingly view Brazil as a net winner from the current oil-price environment precisely because its export gains are large enough to improve external sustainability even if monthly data remain uneven.

There is also a reinforcing investment channel. As the oil sector generates more cash and becomes even more attractive commercially, it draws in additional foreign direct investment, supporting the financial account as well. In that sense, the oil windfall is not only helping current trade numbers; it is also strengthening Brazil’s medium-term external position.

Why the current account improves

- Larger goods surplus

- Higher oil export receipts

- Better terms of trade

- Reduced external vulnerability

- Stronger investor confidence

Why it may not turn fully positive

- Services outflows remain sizable

- Profit and dividend remittances continue

- Refined-fuel imports still create offsets

- Global demand could soften later

- Some gains may prove cyclical rather than permanent

Fiscal Revenues and Investment Get a Lift

Beyond trade and currency effects, the oil shock also boosts public finances. Higher crude prices increase royalties, special participation fees, and Petrobras-related dividends flowing to the federal government and producing states. That creates fiscal space that can help reduce deficits, support public investment, or stabilize spending.

The corporate side matters just as much. Petrobras benefits from stronger cash generation, particularly because pre-salt output remains relatively low cost. Higher cash flow supports upstream investment, future production growth, and shareholder distributions, while also benefiting the wider services and infrastructure ecosystem linked to offshore production.

This combination of public and private gains gives Brazil a broader economic cushion than many peers enjoy. The oil shock is not simply a story of better export prices. It is also a story of stronger revenue collection, more investment capacity, and higher confidence in the durability of the country’s macro position.

Why Brazil Is Better Shielded From Inflation Than Other Oil Economies

Higher crude prices usually create inflation headaches, but Brazil has an important buffer: ethanol. Because flex-fuel vehicles allow consumers to switch between gasoline and biofuels, domestic fuel demand can adjust in ways that soften the pass-through from global oil prices to local pump prices.

That does not eliminate inflationary pressure entirely. The central bank still needs to monitor the supply-side effects of a sustained energy shock, and some inflation impact is likely if high prices persist. But Brazil enters this period in a more favorable position than many emerging-market oil importers, where rising fuel costs translate far more directly into consumer-price stress and weaker growth.

This makes Brazil’s overall macro outcome more balanced. The country captures the export and fiscal upside of higher prices while muting part of the inflation downside through a diversified fuel mix and stronger currency dynamics.

Risks and Limits to the Windfall

The gains are meaningful, but they are not unconditional. If high oil prices persist for too long, they could eventually weaken global growth and reduce demand for exports more broadly. Brazil also still imports some refined products, which creates a partial offset in the fuel balance.

There is also the risk of excessive currency strength. A stronger real helps on inflation and external sustainability, but it can create pressure for non-commodity exporters and raise familiar concerns about a mild Dutch disease effect. Policymakers therefore need to manage the windfall carefully, especially if stronger oil revenues encourage procyclical fiscal decisions.

The central challenge is to avoid treating a favorable external shock as permanent. The opportunity is real, but so is the need for discipline. Windfall revenues are most valuable when they strengthen long-term resilience rather than simply finance short-term expansion.

Conclusion

The 2026 oil price shock has highlighted Brazil’s new strategic position in the global energy economy. Thanks to its large pre-salt reserves, low-cost production base, and exporter status, Brazil is capturing clear gains from a market environment that is hurting many others.

Those gains are visible across the macroeconomy: a wider trade surplus, stronger support for the Brazilian real, an improved current-account position, larger fiscal receipts, and stronger investment capacity. Brazil is not insulated from global volatility, but it is far better positioned than it would have been in earlier oil shocks.

The larger significance is that this moment offers more than a temporary windfall. If managed well, it can support long-term investment in refining, infrastructure, diversification, and the broader energy transition. In that sense, the oil shock is not just boosting Brazil’s economy today. It is creating an opening to reinforce economic stability and strategic strength for years to come.