Oil Prices Will Remain Above Pre-War Levels Even If the Conflict Ends

Even if active fighting stops, physical damage, depleted inventories, higher shipping costs, and a lasting Gulf risk premium are likely to keep oil prices elevated.

OpenMacro

Oil is unlikely to return quickly to pre-war price levels even if the conflict ends. Damage to energy infrastructure, tighter inventories, higher freight and insurance costs, and a lasting geopolitical risk premium are keeping the market structurally tighter.

The recent escalation in the Middle East, particularly the US-Israeli strikes on Iran and the temporary Iranian control of the Strait of Hormuz in March 2026, sent global oil markets into turmoil.

Brent crude, which had been trading in the low $60s to $70s in early 2026 forecasts, skyrocketed above $100 per barrel, with peaks nearing $110 to $120 in volatile trading.

Even as ceasefires were announced and some tanker traffic resumed, many analysts warn that oil prices are unlikely to return to pre-conflict levels in the short to medium term, over the next 6 to 24 months. Structural, logistical, and geopolitical factors will keep the market tight and maintain a significant risk premium.

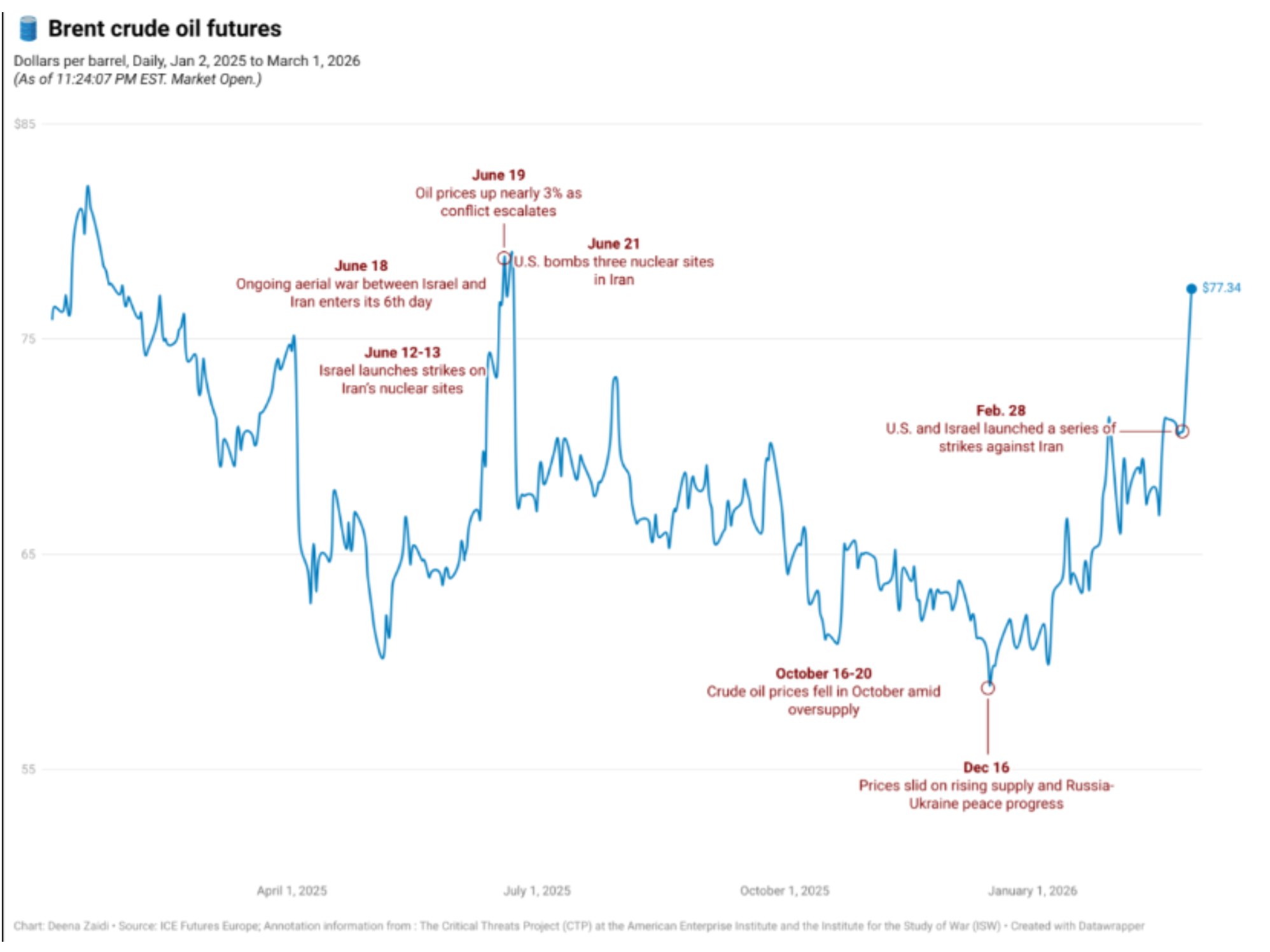

Figure 1

Brent crude has repeatedly repriced higher around conflict escalation, reinforcing the view that oil may remain above pre-war levels.

Source: ICE Futures Europe; annotation data from CTP and ISW

Before the conflict intensified, the oil market was already navigating a delicate balance of recovering demand from Asia, OPEC+ production discipline, and lingering sanctions on Russia.

Pre-war consensus forecasts from banks like Goldman Sachs and the EIA pointed to Brent averaging around $60 to $70 in 2026 amid expected oversupply from non-OPEC producers, including US shale, Guyana, and Brazil.

The disruption of nearly 20% of global oil flows through the Strait of Hormuz, combined with damage to more than 40 energy assets, flipped the narrative overnight. Prices jumped more than 30% in a matter of weeks, reflecting not just immediate supply loss but fears of prolonged outages.

Even in a best-case scenario of sustained peace, physical damage to ports, terminals, and pipelines in the Persian Gulf cannot be fixed overnight. Repairs to major facilities could take 6 to 18 months or longer, depending on the extent of the strikes.

Tanker insurance premiums and freight rates have already risen sharply and will remain elevated until safe passage is fully proven. European and Asian buyers, who rely heavily on Middle Eastern crude, face higher costs for alternative routes or diverted cargoes. As one EU energy official noted, even if peace is restored immediately, normal market conditions are unlikely to return in the foreseeable future.

Depleted Inventories and the Need for Rebuilding Global strategic and commercial stockpiles were drawn down aggressively during the disruption. Rebuilding these buffers, especially in Asia and Europe, will require months of above-normal production. The IEA has already flagged that supply losses in March 2026 exceeded releases from emergency reserves.

Low inventories reduce the market’s cushion against future shocks but also support higher prices until stocks normalize.

Figure 2

Damage to oil and gas facilities across the Gulf helps explain why supply risks can persist even after active fighting eases.

Source: OpenMacro

Persistent Geopolitical Risk Premium The conflict has permanently repriced concentration risk in the Persian Gulf. Long-dated futures now reflect a higher Gulf risk premium, as traders recognize that around 20 million barrels per day remain vulnerable to future tensions.

Goldman Sachs and HSBC analysts argue that this premium is now baked in and will not vanish quickly. Even after flows resume, insurance, security, and rerouting costs will keep effective prices elevated.

OPEC+ Discipline and Supply-Side Constraints OPEC+ has shown willingness to adjust output, and recent increases have been modest rather than transformative. Non-OPEC growth from the US, Canada, and South America is real, but it faces headwinds. US shale productivity gains are slowing, and years of underinvestment in new conventional projects have limited the speed of supply response.

Russian output also remains constrained by sanctions and technology gaps. The net result is that global spare capacity is tighter than pre-conflict projections had suggested.

In short, even if the shooting stops, oil markets are unlikely to revert quickly to the low-price environment expected before the war. The combination of infrastructure damage, tighter inventories, elevated transport costs, and a re-priced geopolitical risk premium means oil is likely to remain structurally above pre-war levels for an extended period.