The Macroeconomic Shock of a “Soft Frexit”: What France Would Lose by Leaving the EU While Keeping the Euro

Leaving the EU while keeping the euro would not spare France from a deep trade, investment, and fiscal shock. It would preserve monetary constraints while stripping away many of the benefits of single-market membership.

OpenMacro

A “soft Frexit” would leave France inside the euro but outside the EU, exposing it to major losses in trade, investment, employment, and fiscal stability. The result would likely be weaker growth, lower real wages, higher inflation pressure, and a prolonged erosion of competitiveness.

France’s prosperity is deeply tied to the European Union. It benefits not only from tariff-free trade, but from frictionless supply chains, common standards, labor mobility, capital flows, and influence over the rules governing its largest market. A “soft Frexit,” in which France leaves the EU but keeps the euro, might appear at first glance to preserve monetary stability while reclaiming sovereignty. In macroeconomic terms, however, it would more likely combine the costs of exit with only a fraction of the supposed gains.

That is because France would remain bound to euro-area monetary conditions while losing full access to the institutional and commercial advantages of EU membership. Trade frictions would rise, investment would weaken, public finances would come under greater strain, and the labor market would absorb a prolonged adjustment. The country would still live under ECB policy, but with less influence over it and fewer buffers against the resulting shock.

The central issue is not whether France could survive outside the EU. It could. The question is what the cost would be. On that measure, the answer is severe: lower trade volumes, weaker productivity, diminished capital formation, softer wages, higher inflation pressure, and a structurally poorer growth outlook.

Why trade would be hit by a soft Frexit

| Channel | What changes after EU exit | Likely effect on France |

|---|---|---|

| Goods trade | Customs checks and possible tariffs | Higher export and import costs |

| Supply chains | Border friction and rules-of-origin hurdles | Lower efficiency and competitiveness |

| Services | Reduced market access and legal complexity | Weaker financial and business exports |

| Regulation | Divergence from EU rules over time | More compliance costs for firms |

Source: Article analysis based on France’s trade integration and Brexit-style friction channels

1. Trade and the Single Market Would Take the First Hit

The most immediate damage would come through trade. France sends the majority of its goods exports to EU partners, and much of its competitiveness relies on the absence of customs barriers, divergent regulations, and border delays. Leaving the EU would mean losing the full benefits of the single market, even if France later negotiated a broad trade agreement.

That distinction matters. A conventional trade deal can reduce tariffs, but it cannot replicate the zero-friction conditions of full membership. Customs checks, rules-of-origin requirements, regulatory divergence, and services restrictions would all raise costs. For an economy as integrated as France’s, those frictions would not be marginal. They would cut directly into output.

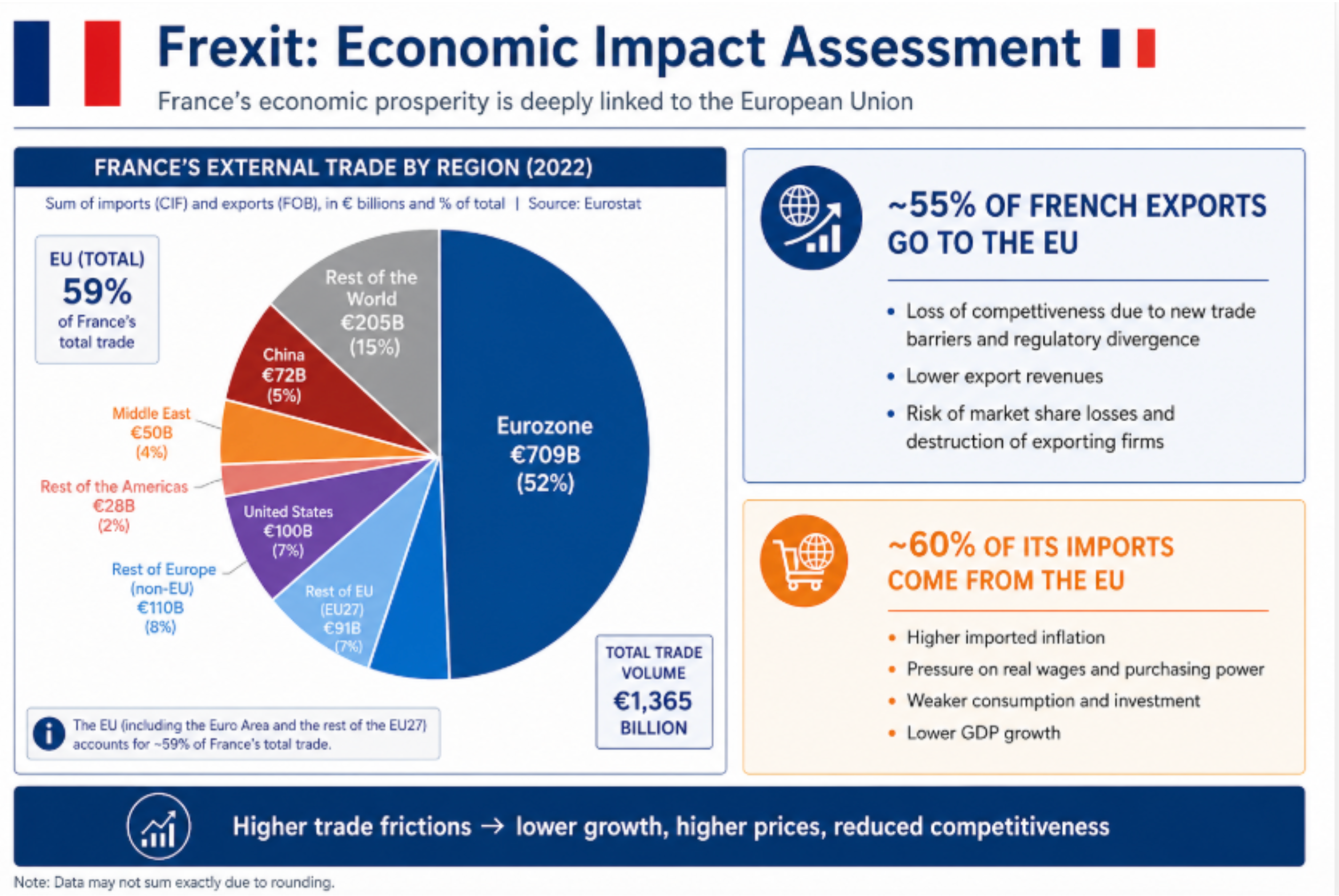

Figure 1

France’s trade structure shows how deeply its economy depends on the EU single market, making any exit likely to raise costs, weaken competitiveness, and slow growth.

Source: Eurostat

The sectors most exposed are also among the most important. Aerospace, autos, chemicals, pharmaceuticals, luxury goods, wine, and agri-food all depend on complex cross-border production and distribution networks. Fragmenting those networks would make France less competitive inside its own neighborhood.

2. Investment, Growth, and Productivity Would Weaken

Trade losses would not stay confined to exports. Once firms believe market access has become less reliable, investment decisions change. Foreign investors become more cautious, domestic firms postpone expansion, and long-term productivity begins to erode.

That pattern was visible after Brexit in the UK, where weaker business investment, softer productivity, and a sustained GDP shortfall gradually emerged. France would likely face a larger version of that dynamic because its integration with the EU is deeper and more central to its industrial model.

A soft Frexit would also create an especially awkward institutional position. France would still use the euro, but outside the EU it would lose influence over rulemaking and over the wider regulatory architecture that supports capital flows, financial activity, and corporate planning. Paris could struggle to preserve its appeal as a financial center if investors concluded that France had chosen monetary continuity without institutional certainty.

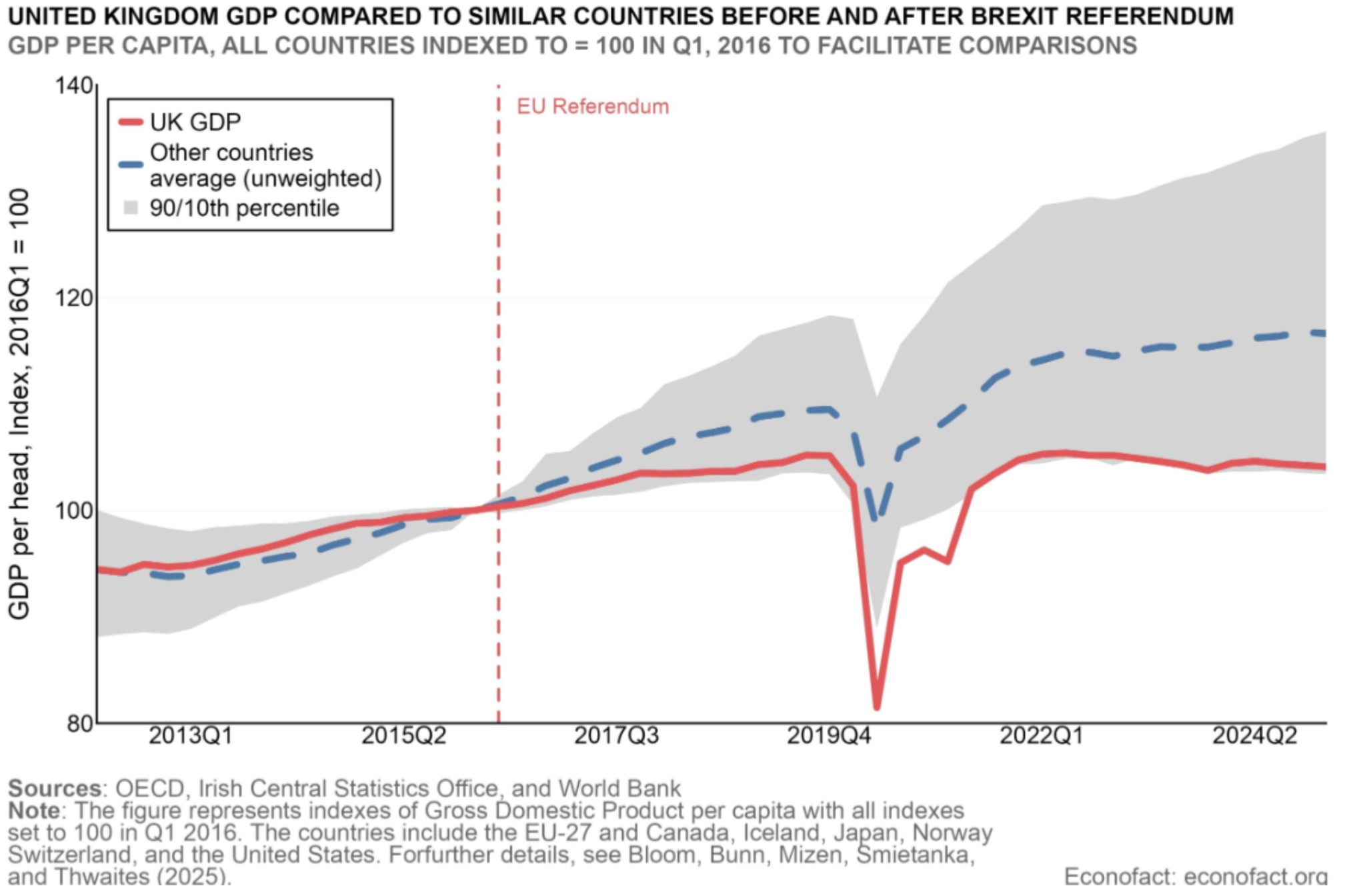

Figure 2

Brexit’s post-referendum growth shortfall offers a warning for France: once trade frictions and uncertainty rise, the economic costs can persist for years.

Source: Econofact; OECD; Irish Central Statistics Office; World Bank

The long-run consequence would be slower potential growth. A more fragmented market means fewer scale advantages, weaker innovation spillovers, and a lower return on capital. That is how a one-time political rupture becomes a lasting productivity problem.

3. Employment, Real Wages, and Inflation Would Come Under Pressure

The labor-market effects would likely be politically explosive. Export-oriented sectors would bear the first adjustment, especially in industrial and logistics-heavy regions already exposed to competitive strain. If trade volumes fall and supply chains contract, employment in those areas would come under pressure.

At the same time, import costs would likely rise. More frictions at the border, weaker confidence, and reduced efficiency in sourcing intermediate goods would feed into prices. In the first years after a Frexit, inflation could rise meaningfully even without a full currency crisis, simply because the economy would become less efficient and more expensive to operate.

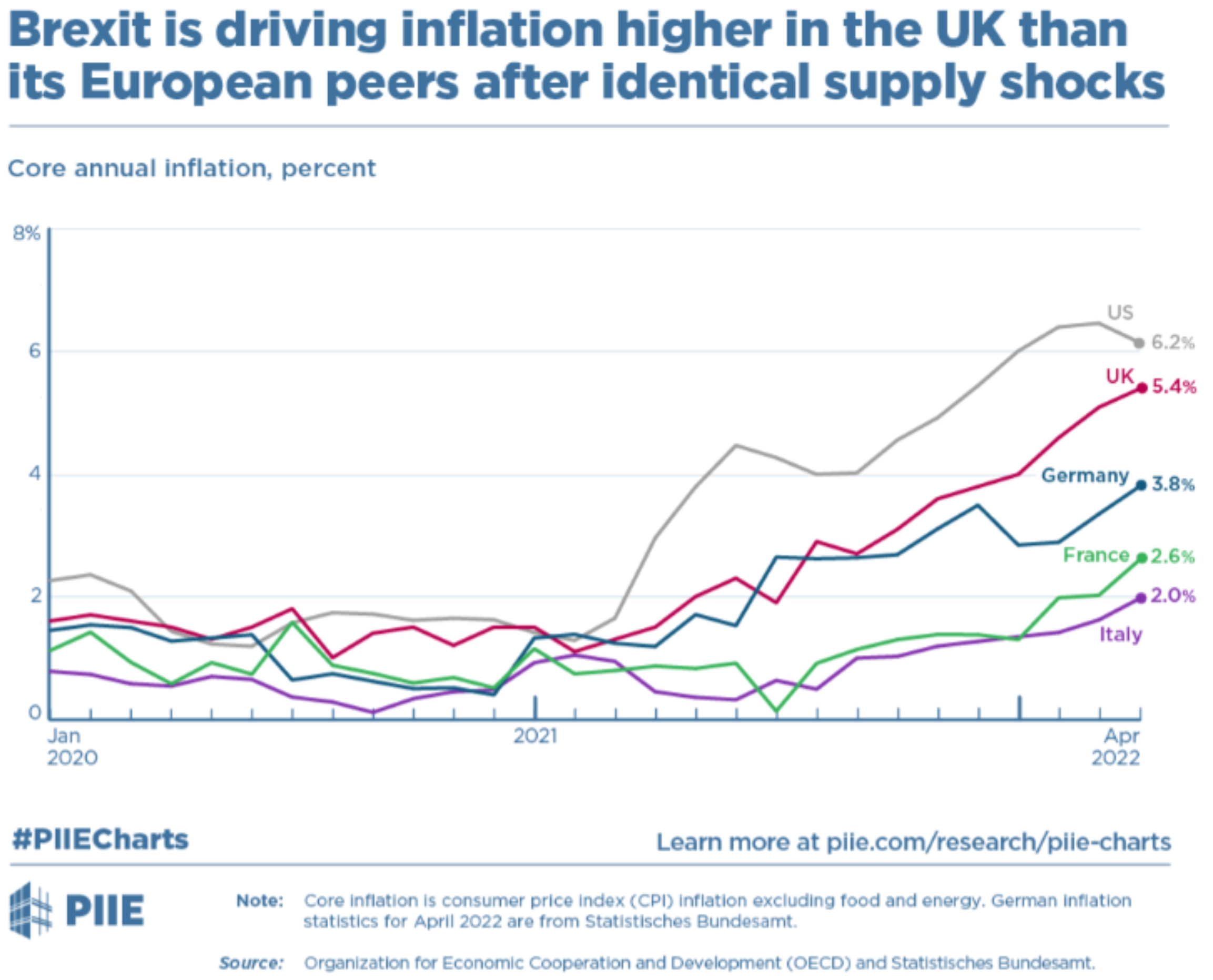

Figure 3

The UK’s stronger post-Brexit inflation pressures suggest that trade frictions and weaker efficiency can raise costs even without a full monetary crisis.

Source: Peterson Institute for International Economics; OECD; Statistisches Bundesamt

That combination is damaging because wages usually adjust more slowly than prices. Households would therefore face a squeeze in real purchasing power. With consumption making up a large share of French GDP, weaker real wages would not only hurt living standards. They would also deepen the broader slowdown.

Short-term labor-market pressures

- Export-sector job losses

- Weaker hiring in manufacturing and logistics

- Higher youth unemployment risk

- Lower business confidence

- Softer household consumption

Inflation and wage pressures

- More expensive imported inputs

- Higher costs for energy and intermediate goods

- Slower wage adjustment

- Decline in real purchasing power

- More social and political strain

4. Public Finances Would Deteriorate

France already enters this scenario with a heavy debt burden. A soft Frexit would make fiscal management harder, not easier. The country would lose access to EU-related inflows and policy support while facing weaker growth, lower tax revenue, and potentially higher financing costs.

That matters especially for agriculture, regional development, and research. France is a net contributor to the EU budget, but it also receives substantial support through the Common Agricultural Policy and other European programs. Losing those flows would put pressure on the national budget if Paris tried to replace them domestically.

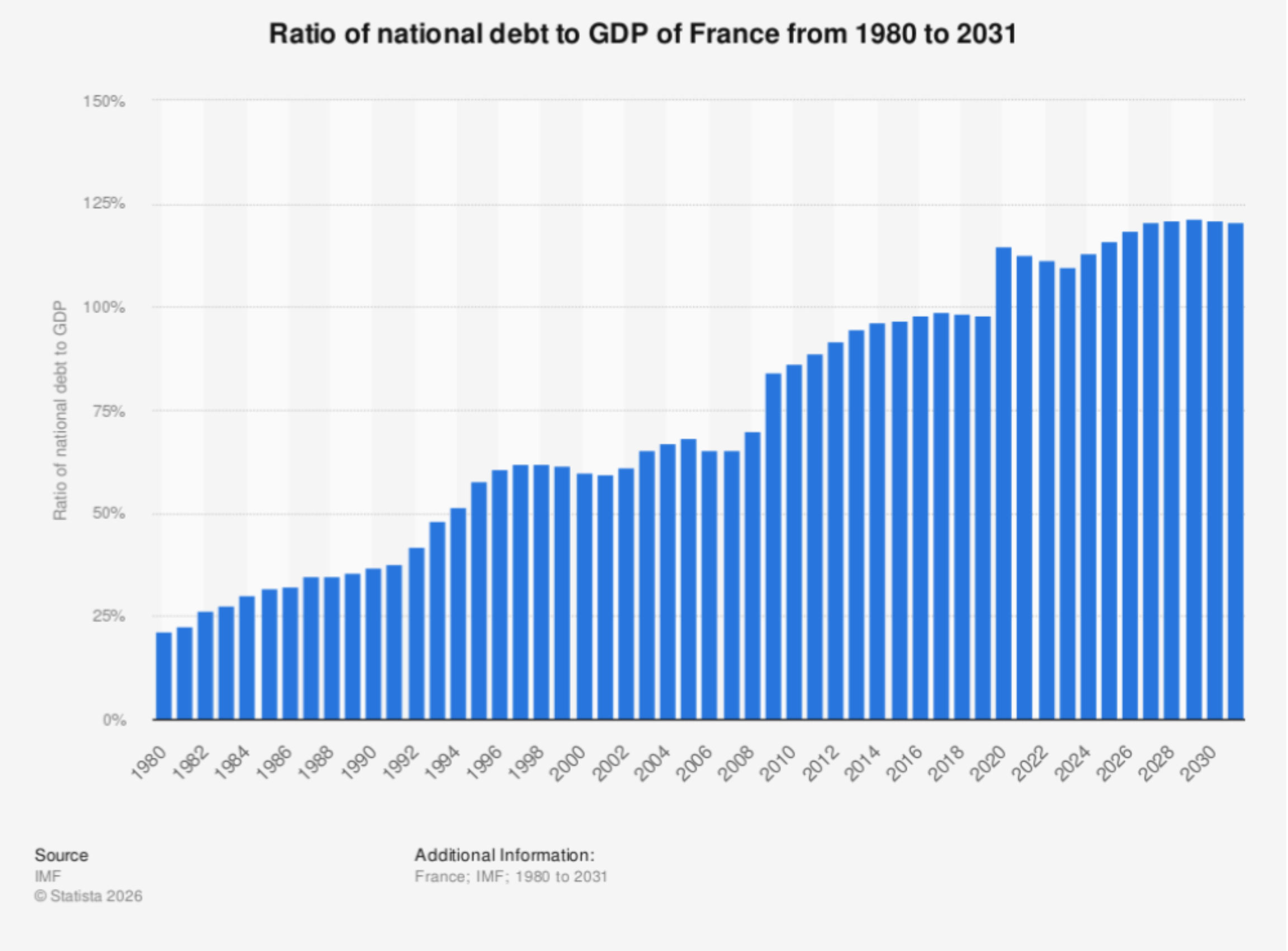

Figure 4

France’s already elevated debt burden means that slower growth, weaker revenues, and higher borrowing costs after a Frexit would be harder to absorb.

Source: IMF; Statista 2026

The broader fiscal arithmetic is even more difficult in a downturn. If output weakens, unemployment rises, and market confidence softens, deficits tend to widen automatically. In a soft Frexit, France would still face the discipline of euro-area borrowing conditions, but with less institutional credibility and more political uncertainty. Debt dynamics could therefore become harder to stabilize, even without any monetary rupture.

5. Keeping the Euro Would Not Eliminate the Structural Tension

At first glance, keeping the euro might seem like the stabilizing element in a soft Frexit. It would likely prevent the kind of abrupt currency collapse associated with a full monetary break. But that same choice would create a different problem: France would remain inside the euro’s monetary framework while outside the EU’s political and regulatory core.

That would mean continued exposure to ECB decisions without full participation in the broader institutional system that shapes European economic governance. France could also find itself aligning with EU standards for trade access anyway, but without having the same voice in setting them. In other words, the country could lose influence without gaining much real autonomy.

This is why the sovereignty argument is weaker than it first appears. A soft Frexit does not cleanly restore policy freedom. It mostly rearranges the costs while keeping key constraints in place.

6. Brexit Offers the Closest Warning, but France Could Fare Worse

Brexit remains the most relevant real-world comparison. The UK’s experience showed that even a large advanced economy can suffer persistent trade, investment, and productivity costs once friction with the EU increases. The damage did not come through one dramatic collapse. It came through years of weaker performance.

France could face a harsher version of that experience because of its different starting point. Its industrial integration with the EU is deeper, its role in the euro area is more central, and its policy constraints under a soft-exit model would be unusually awkward. That means the long-term cost could accumulate into hundreds of billions of euros in lost output over a decade.

The result would likely be a France that is still wealthy, still functional, and still using the euro, but operating with lower growth, weaker competitiveness, and less influence than before. That is not liberation. It is a structural downgrade.

Conclusion

A soft Frexit would be a high-cost gamble with limited upside. France’s economic model is built on access, integration, and influence inside Europe. Leaving the EU while keeping the euro would preserve some stability, but it would not preserve the foundations of that model.

The likely outcome would be weaker trade, softer investment, lower productivity, more labor-market pain, and greater pressure on public finances. France would still live with euro-area constraints, but without the full advantages of being one of the EU’s core powers.

That is the central macroeconomic reality. The question is not whether France could leave the EU and continue functioning. It is whether doing so would make the country richer, stronger, or more sovereign in any meaningful economic sense. The evidence suggests the opposite.