Europe Must Defend Its Strategic Industries Before China Destroys Them

Europe’s industrial base is being squeezed by Chinese subsidies, overcapacity, high energy costs, and slow trade defence. Strategic sectors now need strategic protection.

Renaissance Europe

China’s subsidised industrial overcapacity is weakening Europe’s strategic sectors, from chemicals to clean tech and semiconductors. Europe needs faster trade defence, lower energy costs, and a clearer industrial doctrine to protect its economic sovereignty.

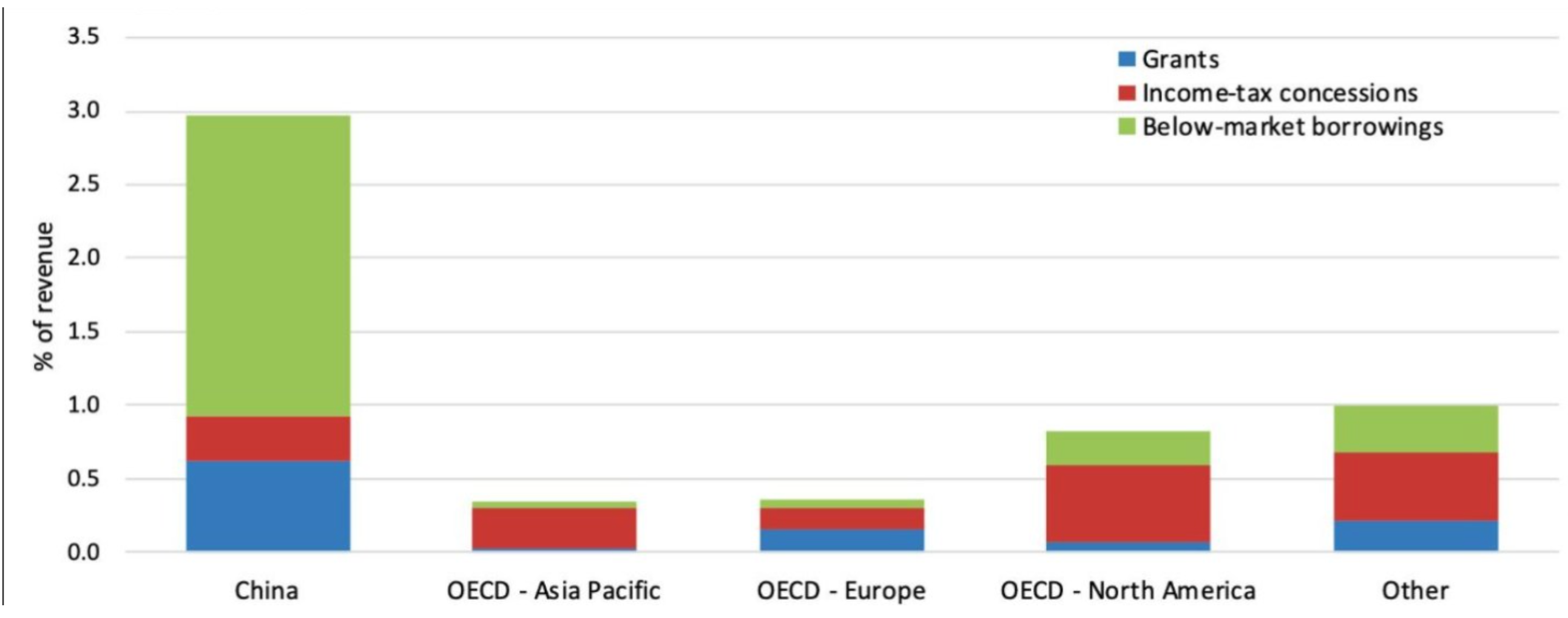

Figure 1

China’s industrial support is far larger than in OECD economies, with below-market borrowing playing a major role in its manufacturing advantage.

Source: OECD MAGIC Database of Industrial Subsidies

For decades, Europe assumed that open markets, high standards, and regulatory discipline would be enough to preserve its industrial strength. That assumption is now collapsing.

China’s rise in strategic manufacturing has not been the result of free-market competition alone. It has been built through massive state subsidies, cheap credit, protected domestic demand, state-directed investment, and industrial overcapacity.

Beijing has deliberately scaled production in sectors far beyond domestic consumption, allowing Chinese firms to export excess capacity into global markets at prices European companies often cannot match.

The OECD has estimated that Chinese firms received between three and eight times more government support than firms in OECD economies between 2005 and 2024. It also found that a large share of China’s gains in global market share has been driven by subsidies rather than pure productivity improvements.

The Chemicals Sector Shows the Risk

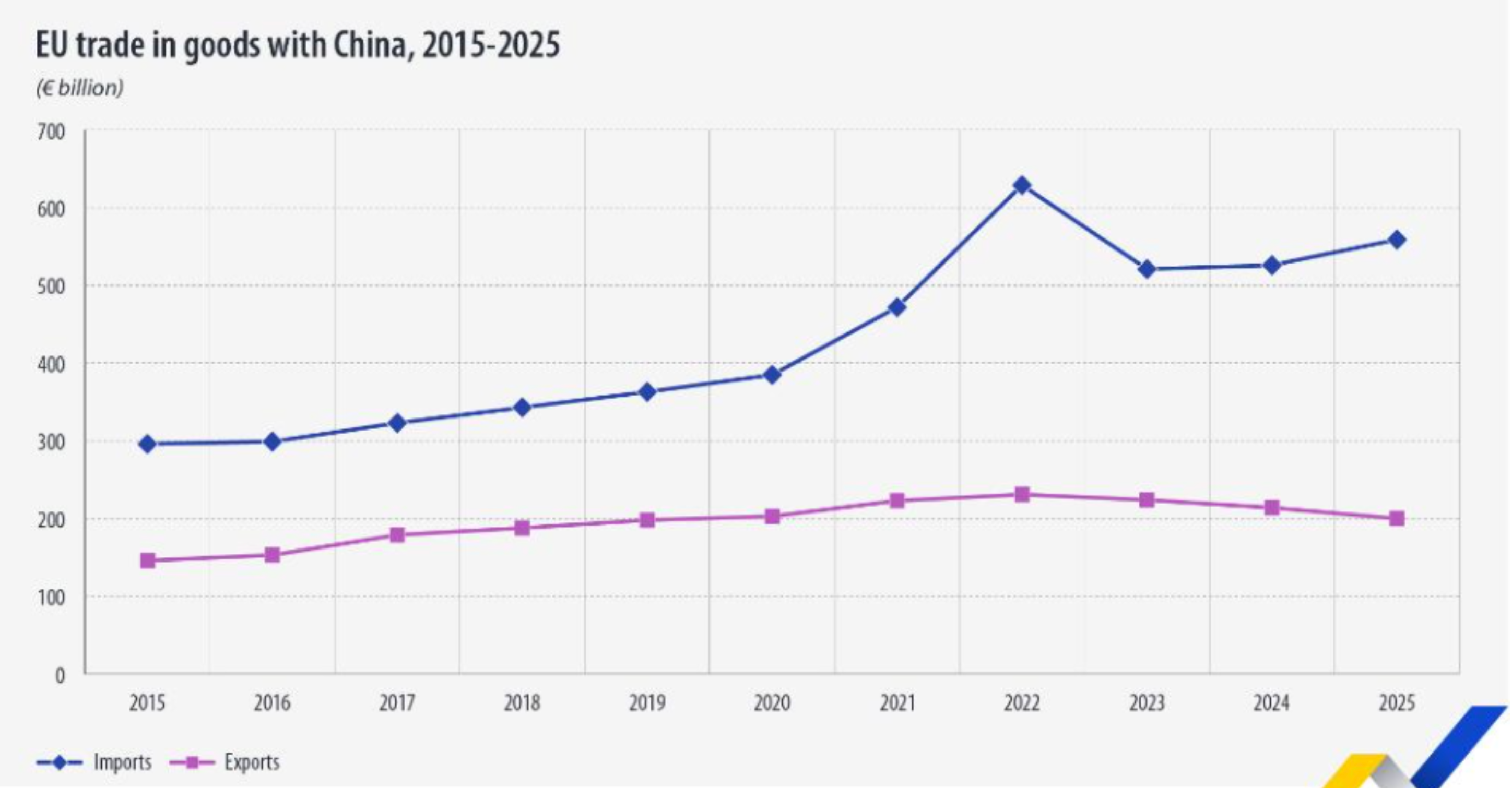

Figure 2

EU goods imports from China have grown much faster than exports, reflecting Europe’s widening exposure to Chinese industrial capacity.

Source: Eurostat

The chemicals sector shows the consequences clearly. Europe’s chemical industry still generates around €635 billion in turnover and employs 1.2 million people, but its global position has weakened dramatically.

Europe’s share of global chemical sales has fallen to around 13%, while China now accounts for 46% of global sales.

Chemicals are not just another industrial sector. They are an input into pharmaceuticals, semiconductors, defence, batteries, agriculture, construction, healthcare, and advanced manufacturing.

If Europe loses its chemical base, it does not only lose factories. It loses part of the industrial foundation required for technological sovereignty, military resilience, and economic security.

Why Europe Is Losing Ground

Europe’s weakness has several causes. High energy costs after the 2022 energy shock damaged the competitiveness of energy-intensive industries. Regulatory complexity has made investment slower and more expensive.

But Chinese overcapacity has added a direct external shock. European firms are competing against a system where the state uses subsidies, cheap financing, and industrial planning to dominate global supply chains.

Europe’s internal weaknesses

- High industrial energy costs

- Slow permitting

- Regulatory complexity

- Fragmented industrial coordination

- Insufficient strategic procurement

China’s external pressure

- State subsidies

- Cheap credit

- Protected domestic demand

- Overcapacity in strategic sectors

- Export pricing European firms cannot match

Trade Defence Is Too Slow

The European response has been too slow. Anti-dumping investigations and trade-defence cases remain necessary, but they are reactive, narrow, and delayed.

By the time a measure is approved, capacity may already have closed, skilled workers may have been lost, and supply chains may have moved permanently outside Europe.

Europe needs a new industrial doctrine. Open markets remain valuable, but openness cannot mean allowing subsidised foreign overcapacity to dismantle Europe’s strategic sectors.

Fair competition requires reciprocity. If Chinese firms benefit from state support, protected domestic markets, and non-market advantages, the EU has the right to defend its own industrial base.

What Strategic Defence Requires

That means faster anti-dumping and anti-subsidy tools. It means stricter treatment of imports produced through heavy state support. It means using access to the Single Market as leverage.

It means excluding heavily subsidised foreign suppliers from sensitive EU-funded infrastructure and procurement when European security interests are at stake.

It also means reducing Europe’s own internal weaknesses. The chemicals industry cannot survive long-term with permanently higher energy costs than its competitors.

Europe must accelerate domestic power production, renewables, nuclear, grids, storage, and electrification to lower structural energy costs for industry. Without energy sovereignty, there can be no industrial sovereignty.

A European strategic industry doctrine

| Policy Area | What Europe Needs |

|---|---|

| Trade defence | Faster anti-dumping and anti-subsidy decisions |

| Single Market leverage | Stricter treatment of heavily subsidised imports |

| Procurement | Exclude subsidised suppliers from sensitive EU-funded projects where security is at stake |

| Energy policy | Lower industrial power costs through domestic generation, grids, storage, nuclear, renewables, and electrification |

| Strategic sectors | Treat chemicals, batteries, clean tech, semiconductors, defence, critical minerals, and advanced manufacturing as security-relevant industries |

| Investment policy | Faster permitting, targeted support, and European-scale coordination |

Strategic Industries Need Strategic Policy

The EU should treat chemicals, batteries, clean tech, semiconductors, defence, critical minerals, and advanced manufacturing as strategic sectors, not ordinary markets.

These industries require targeted support, faster permitting, investment incentives, and European-scale coordination.

China does not separate economics from power. The United States does not either. Europe can no longer afford to be the only major economic bloc pretending that strategic industries can survive without strategic policy.

The choice is not between free markets and protectionism. The real choice is between controlled strategic defence and uncontrolled industrial decline.

Conclusion

Europe should remain open to trade. But it must stop being naïve about the world it is trading with.

If Europe wants to remain a serious economic power, it must defend the industries that make sovereignty possible.

Open markets are valuable, but they only work when competition is fair. When strategic sectors face state-backed overcapacity, Europe needs speed, reciprocity, and industrial policy equal to the scale of the threat.