Europe’s Startup Problem Is Capital Scale, Not Just Regulation

Europe has the talent to build global technology leaders, but fragmented markets and shallow late-stage capital keep too many startups from scaling like their US peers.

Renaissance Europe

Europe’s startup weakness is not only regulation. The deeper problem is capital scale: smaller venture markets, weaker late-stage funding, fragmented national systems, and thinner exit markets prevent European startups from scaling at US speed.

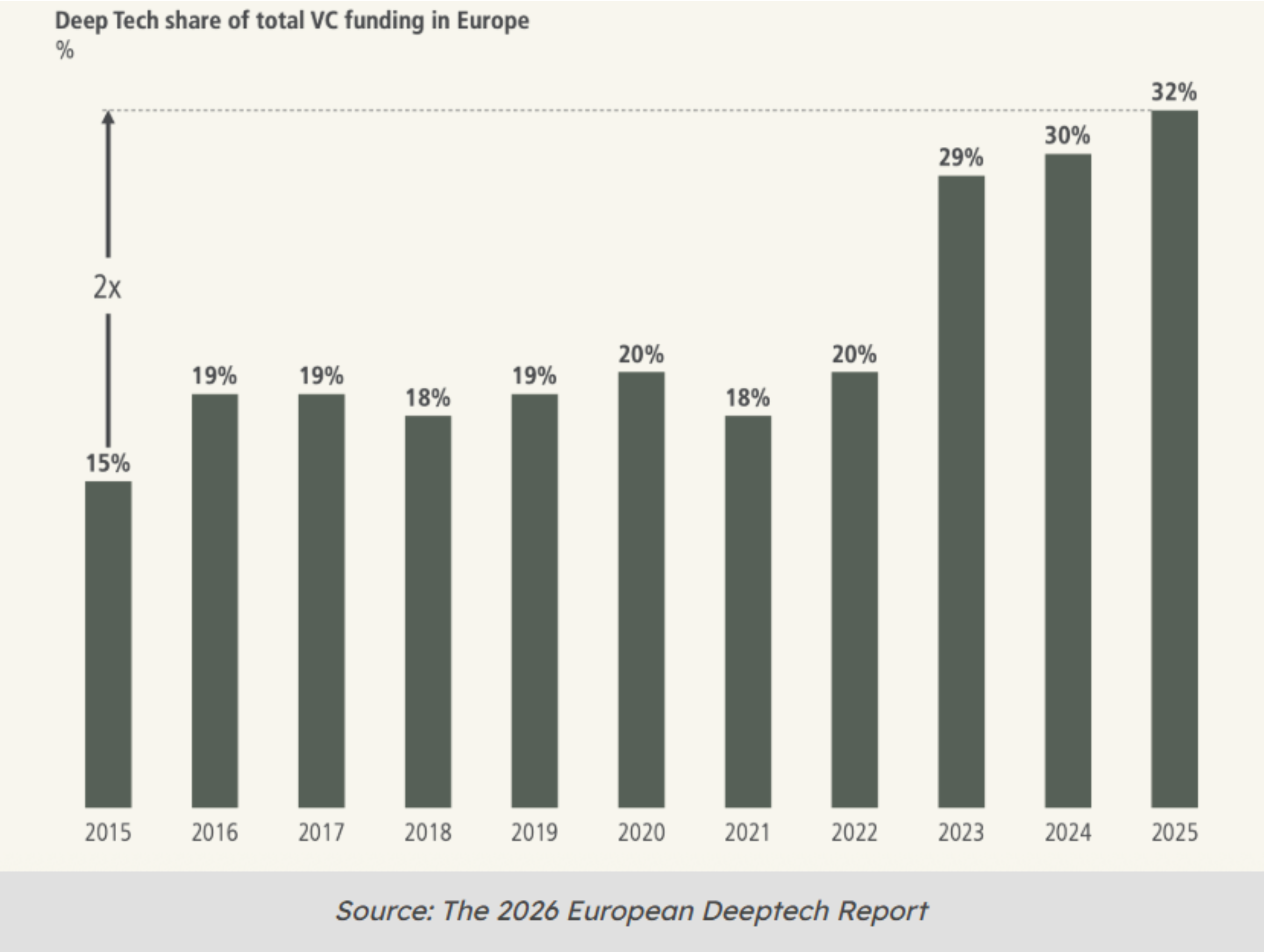

Figure 1

Deep tech is taking a larger share of Europe’s venture funding, but the broader capital pool remains too small to match the scale of US financing.

Source: The 2026 European Deeptech Report

Europe has talent, but it does not give that talent enough capital or a large enough integrated market to scale at the speed of the United States.

The debate is often reduced to one sentence: Europe has too much regulation. That is partly true. But it is not the core of the problem. The bigger issue is capital scale.

In 2025, US venture-backed companies raised around $340 billion. European venture capital investment reached roughly €66 billion. Even allowing for exchange rates and methodology differences, the conclusion is clear: Europe attracted barely one fifth of US venture capital despite having a comparable economic size.

Why Capital Scale Matters

This capital gap matters because startups are not normal companies. They do not scale gradually through retained earnings. They scale through large, repeated funding rounds that allow them to hire aggressively, expand internationally, invest in technology, subsidize customer acquisition, build infrastructure, and absorb years of losses before reaching profitability.

The United States has a much deeper venture capital system. It has larger funds, larger late-stage rounds, deeper institutional capital, stronger pension fund participation, more liquid exit markets, and a single continental market for scaling.

Europe has the opposite structure: smaller funding rounds, more fragmented investors, weaker late-stage capital, thinner IPO markets, and a startup environment divided across 27 national systems.

Europe’s startup scale gap

| Area | United States | Europe |

|---|---|---|

| Venture capital depth | Larger funds and much bigger annual VC deployment | Smaller total VC pool and fewer large rounds |

| Late-stage finance | Deep crossover, pension, endowment, and institutional capital | Weaker scale-up financing environment |

| Market structure | One large continental market | Fragmented across 27 national systems |

| Exit markets | Deeper IPO and acquisition pathways | Thinner public markets and fewer large exits |

| Startup scaling | Faster expansion and higher valuations | More relocation, acquisition, or stalled scaling risk |

The Funding Gap Is Structural

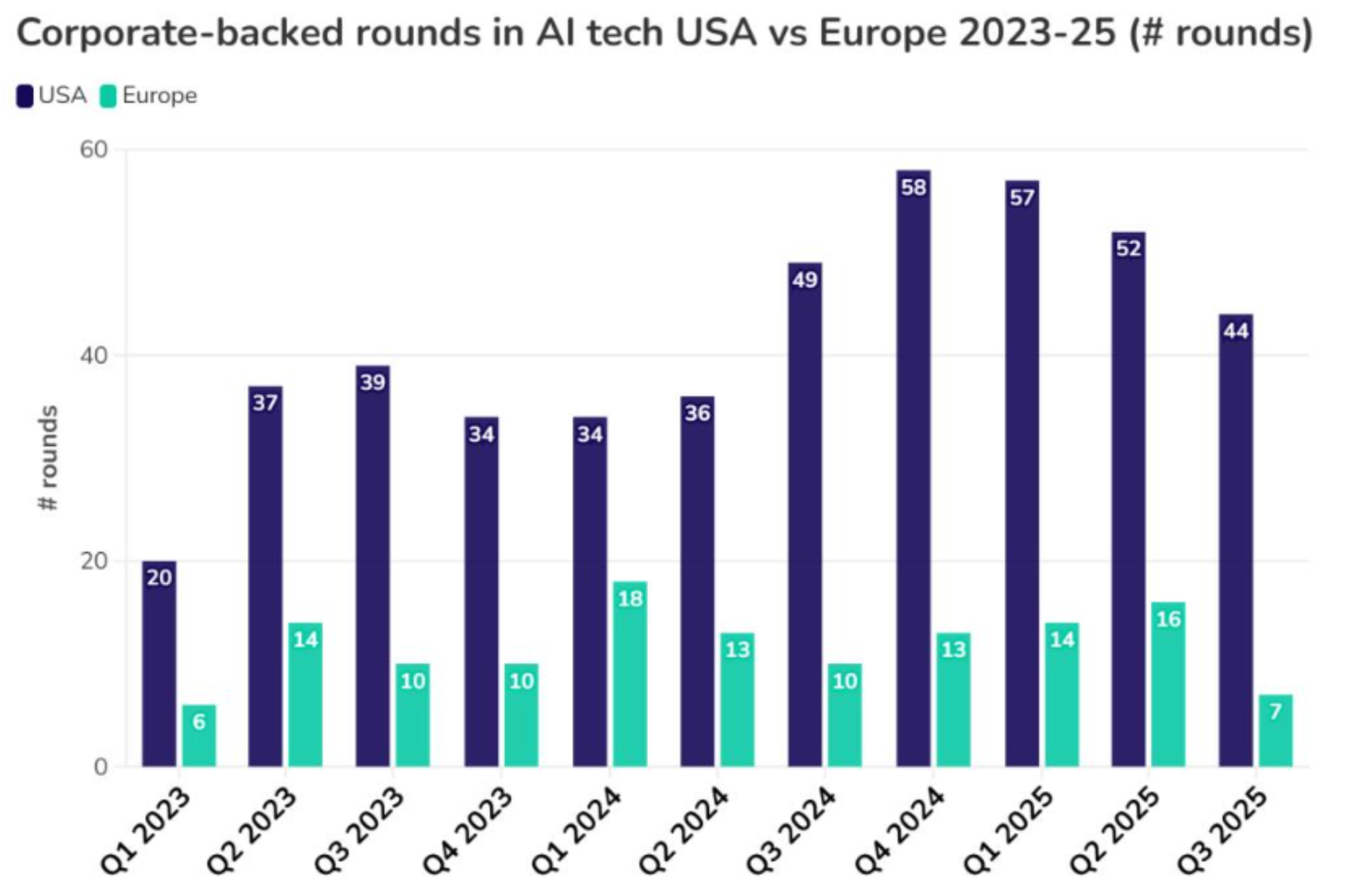

Figure 2

Corporate-backed AI funding rounds remain far deeper in the United States, reinforcing Europe’s disadvantage in late-stage capital and strategic technology scaling.

Source: GCV

Between 2020 and 2025, the United States allocated €1.33 trillion in venture capital, while Europe allocated only €252 billion. In AI, the gap is even more severe: the US directed 34% of its VC funding to AI, while Europe allocated only 18%.

That is not a marginal difference. It is the difference between building global category leaders and producing promising companies that are acquired, relocated, or fail to scale.

The OECD estimates that in 2025, global AI venture investment reached $258.7 billion. US firms attracted around 75% of that value, or roughly $194 billion. EU27 firms attracted only 6%, around $15.8 billion.

Fragmentation Kills Scale

This is the new industrial battlefield. Artificial intelligence, defense technology, semiconductors, quantum computing, robotics, energy systems, and advanced manufacturing all require enormous capital intensity. Europe cannot compete in these sectors with fragmented national funding ecosystems and small late-stage rounds.

The faster a company hires, sells, raises capital, and expands, the more likely it is to dominate a market. Fragmentation directly weakens that momentum.

Europe’s Single Market remains incomplete for companies. In theory, a startup founded in Madrid, Paris, Berlin, or Milan should be able to scale across the continent as easily as a company in California expands across the United States. In practice, it cannot.

European startups face different national tax systems, labor rules, corporate structures, stock-option regimes, insolvency laws, administrative procedures, and regulatory interpretations. Even when the EU has common rules on paper, implementation remains fragmented.

What fragmentation does

- Raises legal and compliance costs

- Slows cross-border hiring

- Complicates stock options

- Weakens investor confidence

- Reduces startup valuations

What scale requires

- Larger integrated market access

- Unified corporate structures

- Deeper late-stage capital

- Better exit markets

- Faster pan-European expansion

The Late-Stage Problem

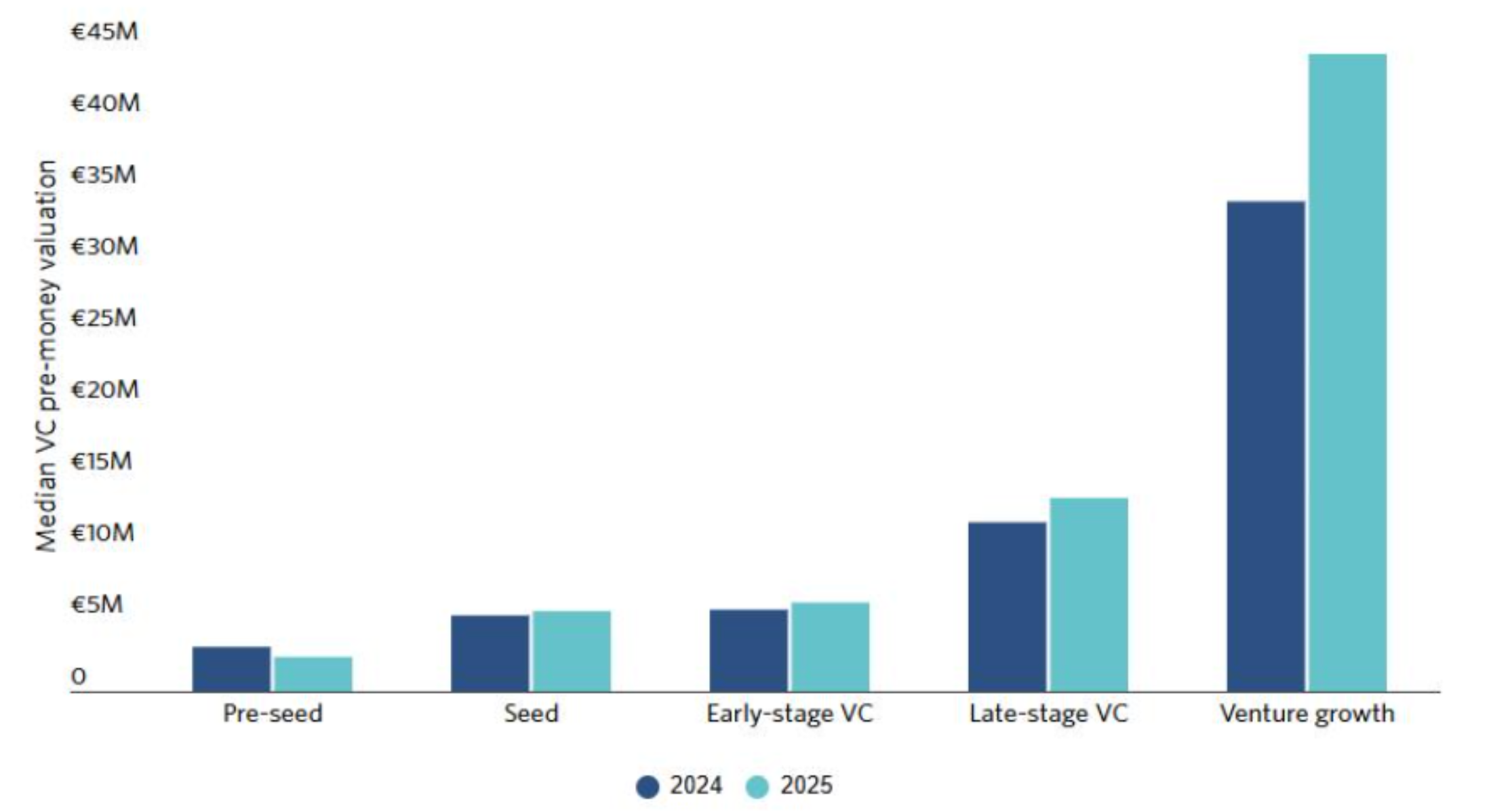

Figure 3

European valuations rise sharply at the venture-growth stage, showing why deeper late-stage capital is critical for scaling startups.

Source: PitchBook’s Q1 2025 European VC Valuations Report

Europe’s capital weakness is most damaging at the scale-up stage. Early-stage capital exists. Europe can fund seed rounds. It can create thousands of promising startups. But when companies need €50 million, €100 million, or €500 million to compete globally, the system becomes much weaker.

This is where the United States dominates. Large American funds, pension capital, endowments, sovereign investors, crossover funds, and public market investors create a much deeper financing environment.

According to Banque de France analysis, between 2014 and 2023 venture capital investment reached more than €1 trillion in the United States, compared with only €89 billion in the EU. The same analysis notes that long-term private financial investors contribute 17 times less to venture capital in Europe than in the United States.

That is the heart of the problem. Europe has savings. It has capital. It has pension assets, insurance assets, and household wealth. But too much of that capital is trapped in low-risk, low-return instruments or fragmented national financial systems instead of being channeled into innovation, technology, and productive risk-taking.

The Solution: Capital Markets Union and a Real Single Market

Europe does not need to choose between deregulation and industrial strategy. It needs both. But the central reform is clear: Europe needs capital scale.

That means completing the Capital Markets Union and building a true Single Market for companies.

A real Capital Markets Union would mobilize European savings into productive investment, deepen venture capital markets, expand late-stage financing, improve IPO conditions, and make it easier for institutional investors to allocate capital to European technology.

A real Single Market for companies would allow startups to scale across the continent without rebuilding their corporate, legal, tax, and employment structure in every country.

The European Commission’s EU Inc proposal is a step in this direction. It aims to allow companies to register online within 48 hours for €100 and operate under a more unified EU-wide corporate framework. That would not solve every problem, but it recognizes the core issue: European companies need a continental operating base, not 27 fragmented national systems.

A fragmented market produces fragmented capital. If Europe wants global startups, it must give them a continental market and continental-scale financing.

Conclusion

Europe’s startup problem is not just regulation. Regulation matters, but the deeper issue is that European companies do not get enough capital, late enough, at sufficient scale, inside a market unified enough to support global expansion.

The United States combines deep venture capital, large institutional investors, liquid exit markets, and one vast domestic market. Europe combines talent with fragmentation. That is why too many European startups remain promising rather than dominant.

Fixing this requires a serious Capital Markets Union, stronger late-stage financing, deeper institutional participation, better IPO markets, and a real Single Market for companies. Without those reforms, Europe will continue to generate ideas that scale elsewhere.