Global Market Outlook — April 2024

Perspectives from the Global Portfolio Team

OpenMacro

Inflation is back at the center of market narratives, but moderating indicators and improved earnings have nudged central banks toward a more patient stance. Our base case is a “hold” from major central banks, continued volatility (shifting to the long end of curves).

Inflation concerns have dominated recent discussions, with better than expected corporate earnings and moderating economic indicators prompting central bankers to adopt a more dovish stance on interest rates since our last update. Federal Reserve Chair Jerome Powell suggested that the Fed is nearing the confidence required to begin easing interest rates, stating, "when we do gain that confidence which isn't far off it will be appropriate to start scaling back restrictions. " Similarly, European Central Bank President Christine Lagarde hinted at a possible interest rate cut in June, as new projections indicated inflation reaching the 2% target by 2025.

Introduction: a world transformed

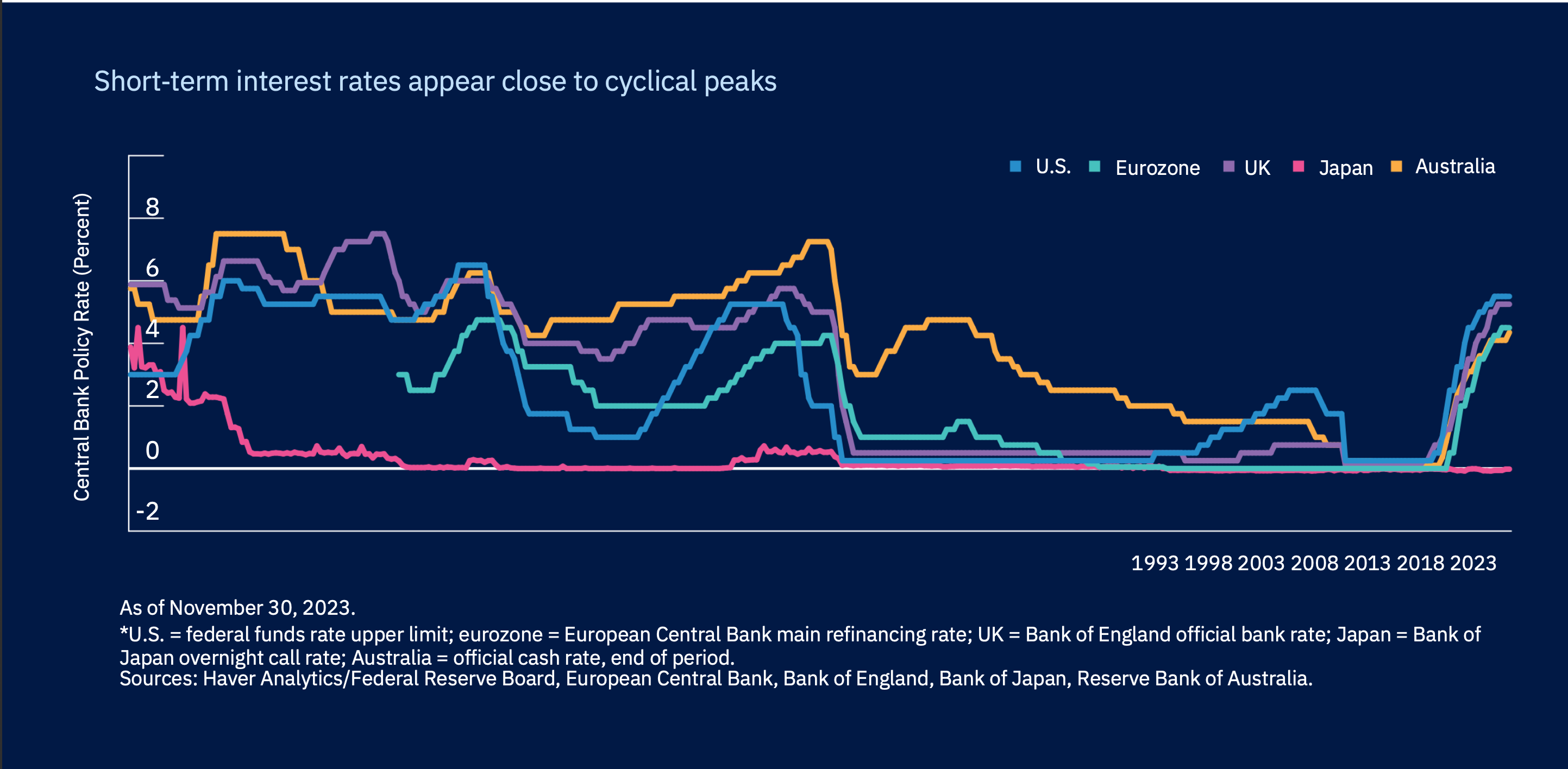

The recent economic disruptions have caused significant changes in the worldwide investment scene. The extensive fiscal support and low interest rates observed during the pandemic have transitioned into tighter monetary policies and notably increased bond yields. Despite the efforts of major central banks like the U.S. Federal Reserve to combat inflation and the apparent nearing of policy rate peaks, our analysis suggests that the Fed is likely to keep rates stable in 2024.

The impacts of monetary policy usually take time to manifest, which means that global economic growth remains under threat. The eurozone is already experiencing a recession, and China's recovery following the pandemic has been underwhelming. Nevertheless, the economic outlook in the United States appears more positive, with both businesses and consumers demonstrating a lesser sensitivity to rising rates compared to other major global economies. Fiscal stimulus has added further support. Bond volatility moves to the long end

Uncertainty is likely to keep fixed income volatility high in 2024. But if major central banks remain on hold, volatility is likely to move to the long end of the yield curve, as opposed to the sharp moves seen at the short end as central banks tightened. Surging U.S. Treasury issuance also could keep upward pressure on longer‑term yields.

Attractive yields should support below investment‑grade (IG) corporates, with improved credit quality helping keep defaults relatively low. Shorter‑term IG corporates also appear to offer opportunities. Careful attention to issuer fundamentals will be critical.

Looking beyond the tech giants

The global equity rebound in 2023 was dominated by a handful of mega‑cap U.S. technology stocks. But positive fundamentals in some regional markets and innovations in other key sectors should help expand the opportunity set in 2024.

Health care innovation is one area that could offer opportunities, as could the energy sector, thanks to capital investment in both traditional and renewable energy sources. Commodity‑related sectors appear to have bottomed and could be attractive hedges if inflation proves stickier than expected.

Emerging market (EM) equities are attractively valued relative to developed markets. We see selective opportunities in China, despite sluggish economic growth. Within the developed markets, structural and cyclical factors should be supportive for Japanese equities.

Figure 1 — Central bank policy rates

Short-term interest rates appear close to cyclical peaks

Source: Haver Analytics / Federal Reserve Board, ECB, BoE, BoJ, RBA

Navigating macroeconomic intricacies

The COVID pandemic and the subsequent recovery continue to distort the economic data, forcing economists who rely on traditional recession signals to continually revise their assumptions. As a result, the most anticipated global recession in history has become the most delayed recession in history.

To be sure, there are reasons for caution regarding the global economic outlook. Europe looks likely to endure stagnant growth in early 2024 before recovering in the second half. In Asia, China’s economic outlook remains gloomy, with few signs of improvement in the country’s property market. Commercial real estate sectors remain fragile in several other countries as well.

Meanwhile, the U.S., Japan, and Europe are at different stages in the balance between growth and inflation, meaning the Fed, the European Central Bank, and the Bank of Japan (BoJ) are likely to pursue increasingly asynchronous monetary policies in 2024, adding to the potential for increased market volatility. Geopolitical uncertainty also could bring further volatility, particularly if conflicts in the Middle East and Ukraine cause a resurgence in energy prices. Recent election victories for far-right populist candidates in Argentina and the Netherlands raise the question of whether further wins for populist parties could occur elsewhere, especially in the U.S., where the November 2024 election will be the most consequential currently known political event of the year.

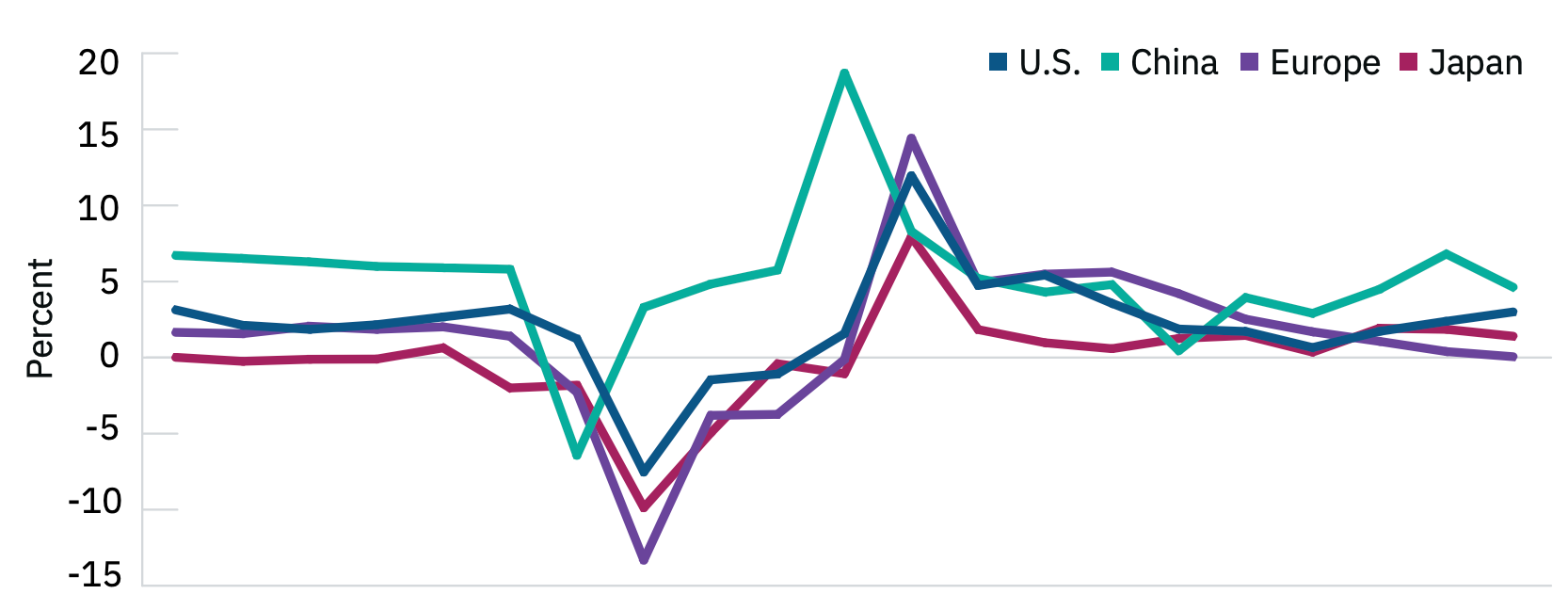

As of late November 2023, most global economies were showing surprising resilience to higher rates (Figure 2), and the U.S. economy was performing better than expected. The unprecedented levels of cash generated by pandemic support and other fiscal stimulus measures have been a key support for U.S. household and corporate balance sheets. Excess consumer savings should continue to provide support for U.S. economic growth going forward .

“ The most anticipated global recession in history has become the most delayed recession in history.”

Figure 2 — Major economies show surprising resilience

Major global economies have shown resilience despite higher rates

Source: U.S. BEA; Statistical Office of the European Communities; Cabinet Office of Japan / Haver Analytics

Dealing with regime change

Even if the U.S. economy remains resilient, investors may need to adapt to a new market regime. Comparing today to historical regimes suggests the post-GFC “new normal” is less likely to return, while upside inflation risks remain meaningful.

If inflation reaccelerates while growth is anemic, stagflation risks would rise. The key is not to assume that the last decade’s playbook will apply unchanged.

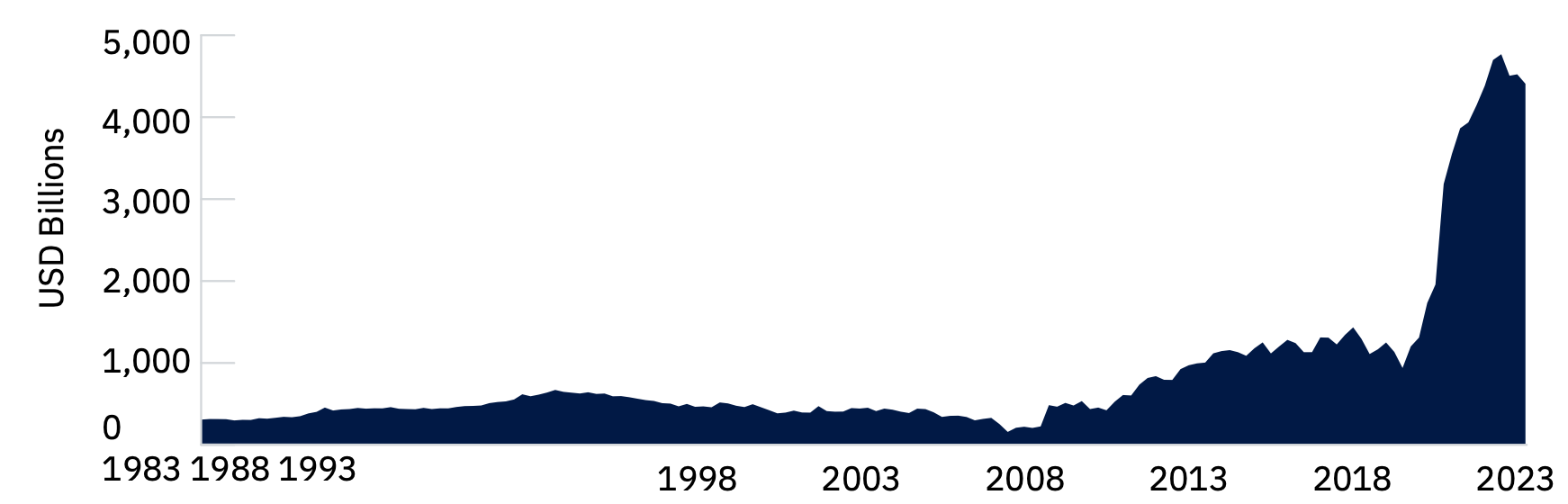

Figure 3 — U.S. consumers still flush with cash

Household cash balances rose sharply in the post-pandemic period

Source: U.S. Federal Reserve Board

Dealing with regime change

Consumer spending has been the most resilient driver of growth, due to the strength of the U.S. labor market. At the end of September 2023, there were 9.6 million open jobs available for the 6.4 million unemployed workers in the U.S. labor force.

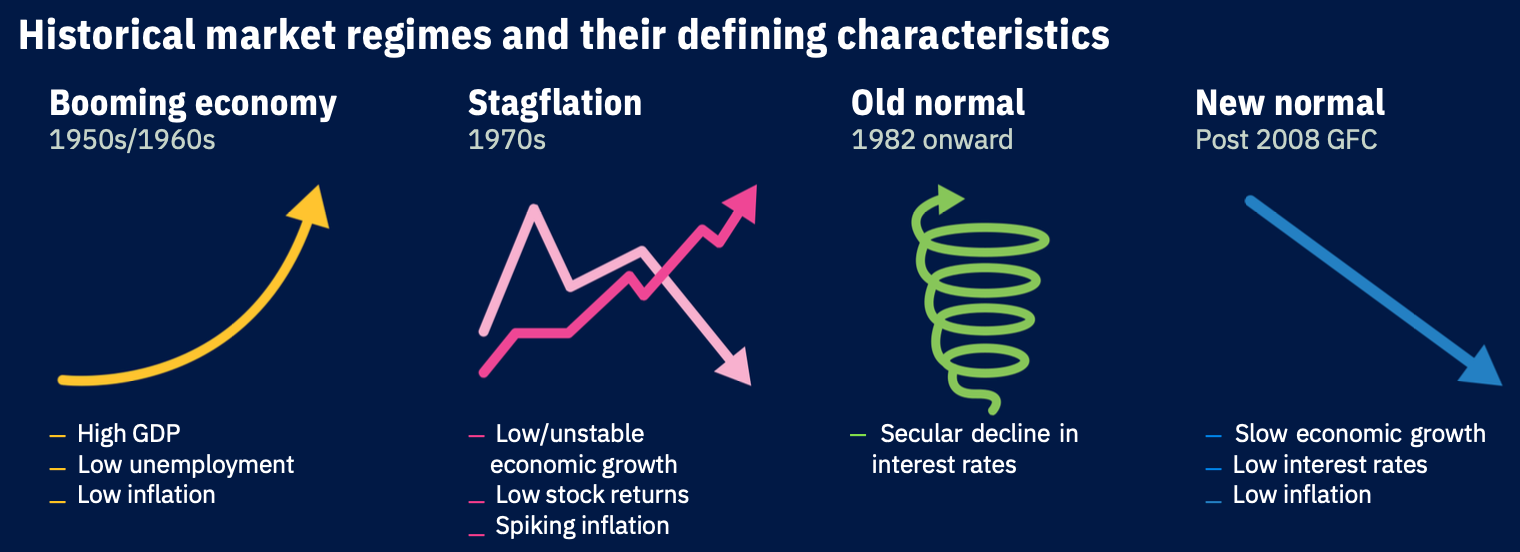

Even if the U.S. economy remains resilient in 2024, we believe investors will need to adapt themselves to a new market regime. To understand the implications of this shift, it is useful to examine the four historical regimes that U.S. markets have experienced since 1955, after the distortions created by World War II and the Korean War had largely dissipated. While the post-pandemic regime may not align perfectly with any of these prior periods, it will include some factors that prevailed during those regimes. Given the shift away from the structural forces that supported disinflation and lower rates in the wake of the 2008 global financial crisis (GFC), a return to the post-GFC “new normal” strikes us as the least likely outcome going forward.

Heading into 2024, inflation risks are skewed to the upside. Energy prices are a concern amid supply-side pressures. As of third quarter 2023, U.S. wages were still growing at almost a 4% annual rate. If U.S. consumer inflation changes course and reaccelerates while economic growth remains anemic, the risk of stagflation will rise considerably.

Which regime is most likely to prevail in 2024?

Recent readings for the fed funds rate and inflation have been closest to the pre-GFC “old normal.” But the regime second closest to recent conditions isn’t stagflation, it’s the postwar boom.

It remains to be seen how real (after-inflation) interest rates above 2% will play out in the markets. But we do not believe that high rates will kill the U.S. economy. Rates are high relative to the post-GFC period, but not relative to capital market history. The federal funds rate exceeded 5% for decades and stock markets still did well. Sticky inflation historically has been good for earnings.

Figure 4 - Historical market regimes

Source: Astant Global

Neutral on risk assets

Despite the macroeconomic uncertainties, we see no reason for investors to be excessively bearish. Market segments that don’t trade at nosebleed valuations, such as small- and mid-cap stocks and real assets equities, look appealing on a relative basis. If we see a spike in volatility and a market sell-off, it could be an opportunity to buy stocks.

However, we also don’t think this is the right time to take large tactical (short-term) allocation bets. The recent “dis-inversion” of the U.S. yield curve could augur volatility in both stocks and bonds in the months ahead. We think the best approach heading into 2024 is to have a broadly neutral view on risk assets, including equities.

With U.S. interest rates closer to their historical averages, a balanced portfolio could offer diversification benefits1 as bonds now provide higher income and ballast to stocks. However, interest rates are likely to remain volatile in 2024, which could favor cash or short-term bonds. These assets currently offer attractive yields with minimal duration2 exposure and could be potential sources of liquidity if market opportunities arise.

Looking beyond the traditional 60/40 stock/bond portfolio, investors willing to take on more risk could consider alternatives with lower correlations to traditional assets and areas of the market that could benefit from market dislocations and higher yields, such as private credit.

Rethinking fixed income

The massive tightening of financial conditions since late 2021 has produced a fixed income market vastly different from the stimulus-fueled environment during and following the pandemic. The cross-currents generated by these changes will challenge investors again in 2024. Heading into the year, we think the best way to describe the macro environment is that we have reached or passed peak everything—inflation, liquidity, fiscal support, China growth, housing, credit availability, and labor market strength. In other words, most of the one-off tailwinds that defined the post-pandemic environment are fading away.

“We see no reason for investors to be excessively bearish.”

Although global economies—the U.S. economy in particular—have held up relatively well so far despite higher rates, a hard economic landing is not out of the question, especially following the spike in bond yields. Even if a recession is avoided in 2024, we are likely to see economic growth concerns intermittently elevated.

Investment Idea — Income + reasonable valuations

| Investment Idea | Rationale | Examples |

|---|---|---|

| Focus on areas with attractive income | The global economy has been resilient despite higher rates, but strong growth is unlikely in 2024. This should limit the upside in asset prices, so income from higher yields is likely to be an important driver of returns in 2024. | — Short‑term fixed income |

| Consider tilting toward asset classes where valuations are undemanding. | Small‑cap equities trade at historically low valuations, reflecting economic growth concerns and the potential impact of higher rates. Small‑caps could provide significant upside if the economy remains resilient. | U.S. small‑cap stocks, International small‑cap stocks |

Source: April 2024 Global Market Outlook

"Obtaining attractive yields doesn’t require investors to accept as much credit risk as in the past"

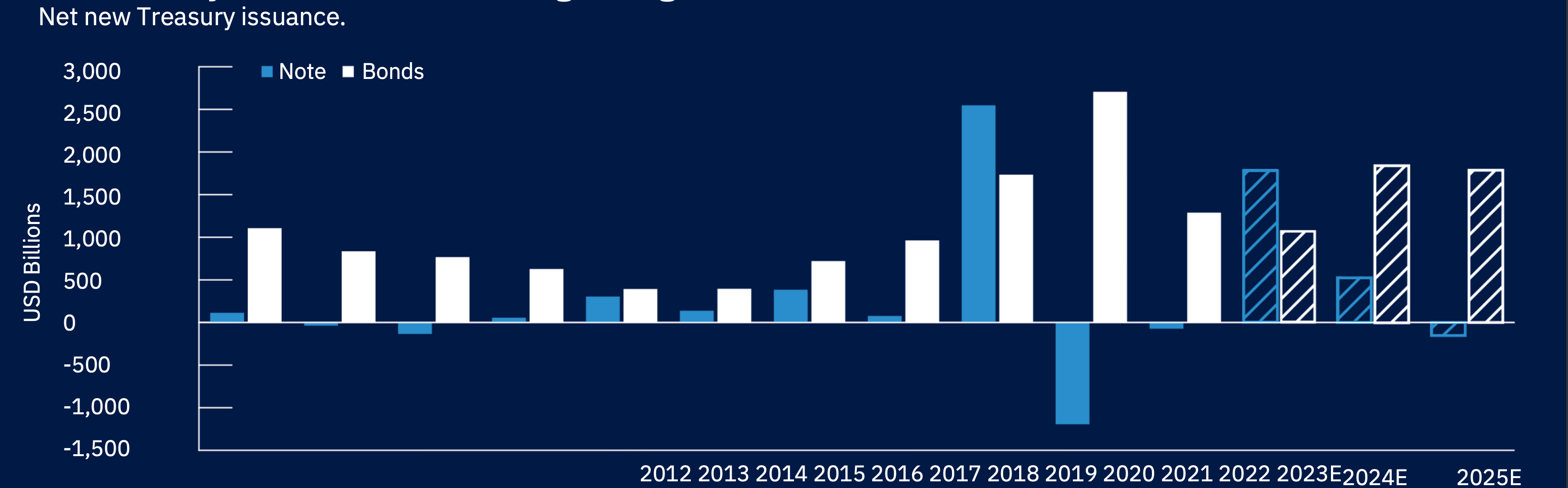

Sovereign issuance is surging

With fiscal deficits ballooning, we expect governments to continue flooding the market with new sovereign debt. This is particularly true in the U.S, where the treasury is shifting the bulk of new issuance away from short-term bills and into longer-term notes and bonds .

This issuance shift is the basis for one of our highest-conviction calls: that yield curves will steepen in 2024. Although yields on high-quality sovereign debt may have peaked in late 2023, they still could move higher. Accordingly, we think curve steepening is likely to be a more significant factor than the outlook for interest rate levels.

Another implication of the surge in government bond issuance is that it could crowd corporate borrowers out of the market—or at least force up their funding costs. This could make companies less likely to spend on capital projects or hire more employees, reducing support for the global economy.

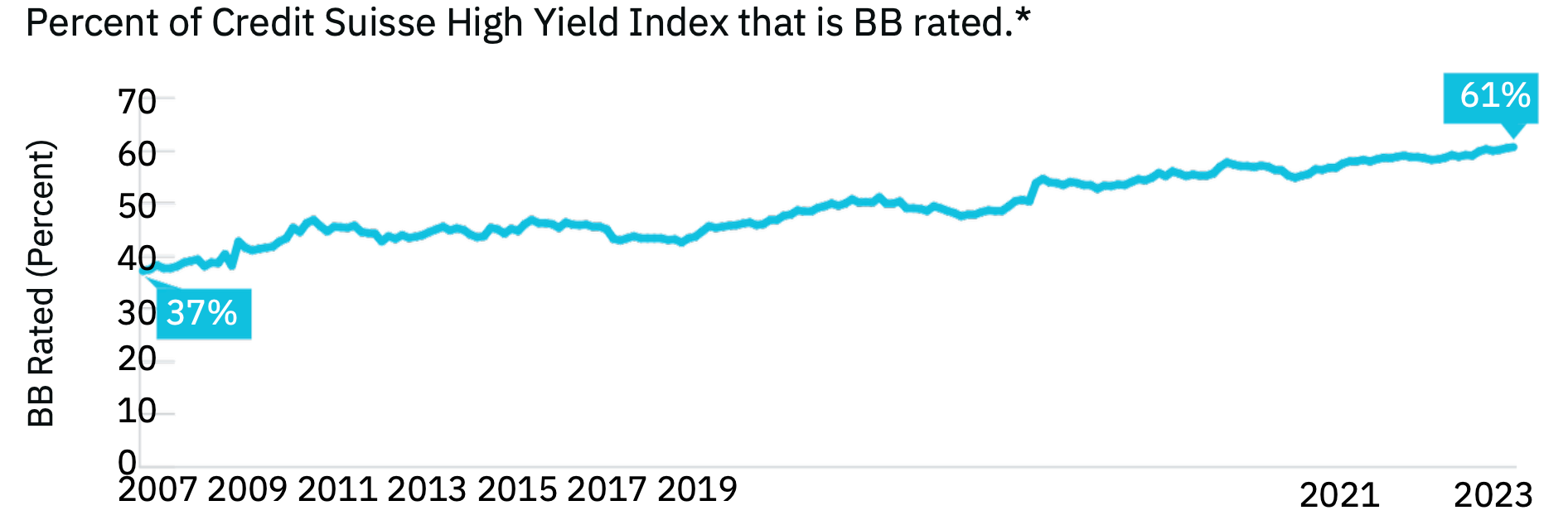

High yield credit quality has improved

Looking more closely at the corporate bond market, attractive yields should continue to support demand for high yield bonds, even though credit spreads—the yield differences between bonds with credit risk and high-quality government bonds with similar maturity dates—appear less compelling, trending near historical averages as of late November. Obtaining attractive yields doesn’t require investors to accept as much credit risk as in the past because the quality of the high yield bond universe overall has improved .

We also see attractive opportunities in shorter-term IG corporates. While these instruments carry some credit risk, short maturities reduce their exposure to an economic downturn. As of late November, shorter-term corporates provided a meaningful yield premium over money

Figure 5 - High yield ratings quality has “migrated up”

*Based on S&P ratings. BB represents the highest rating below investment grade.

Source: Credit Suisse

Figure 6 - U.S. Treasury debt issuance is shifting to longer maturities

Actual outcomes may differ materially from estimates.

Source: U.S. Treasury, Securities Industry and Financial Markets Association, Morgan Stanley. Estimates by Morgan Stanley.

Broadening equity horizons

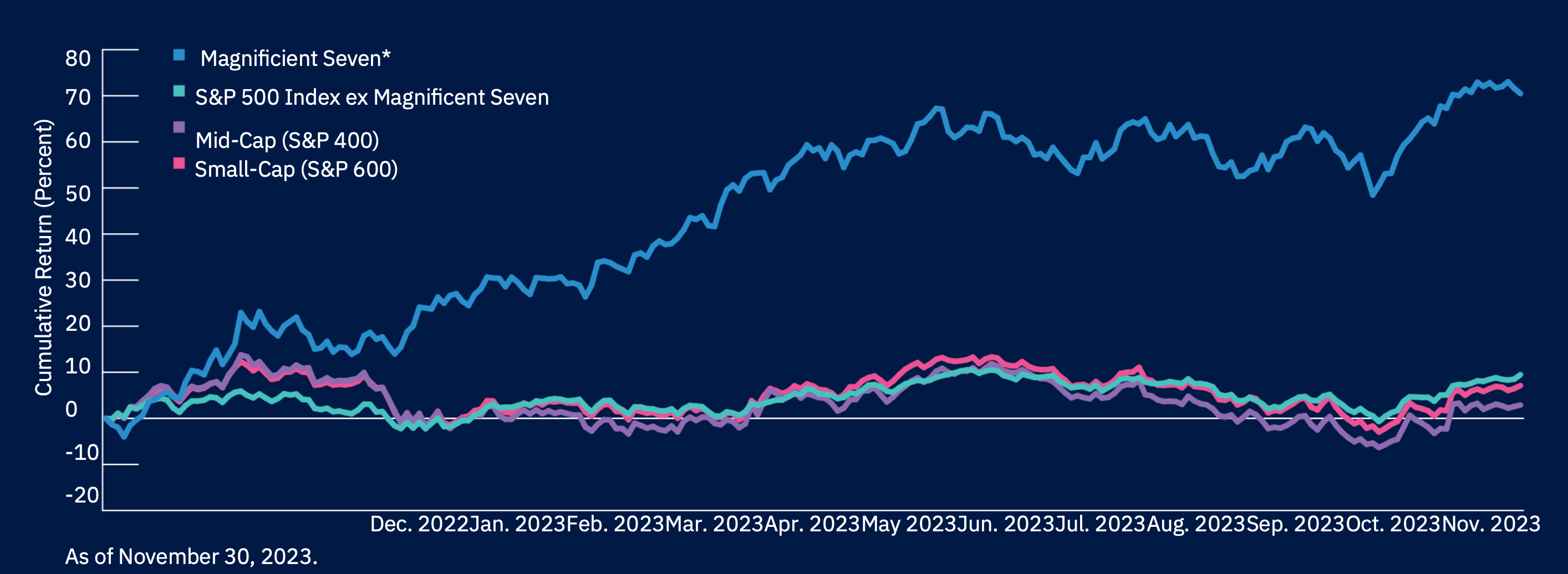

Global equity markets are likely to remain challenged in 2024 as the world transitions to a regime of higher trend inflation and interest rates. This transition could generate shifts in earnings growth expectations, triggering volatility. Close attention to risk management will be needed. On the plus side, broader, less concentrated market leadership is likely to provide more varied sources of returns for investors who maintain a sharp focus on valuation fundamentals. Although U.S. equity valuations appear more reasonable, they continue to face stiff competition from attractive yields on money market and short-term fixed income assets. This suggests a need to look for pockets of attractive relative valuation. Global equity performance in 2023 was predominantly driven by the so-called “Magnificent Seven” mega-cap U.S.

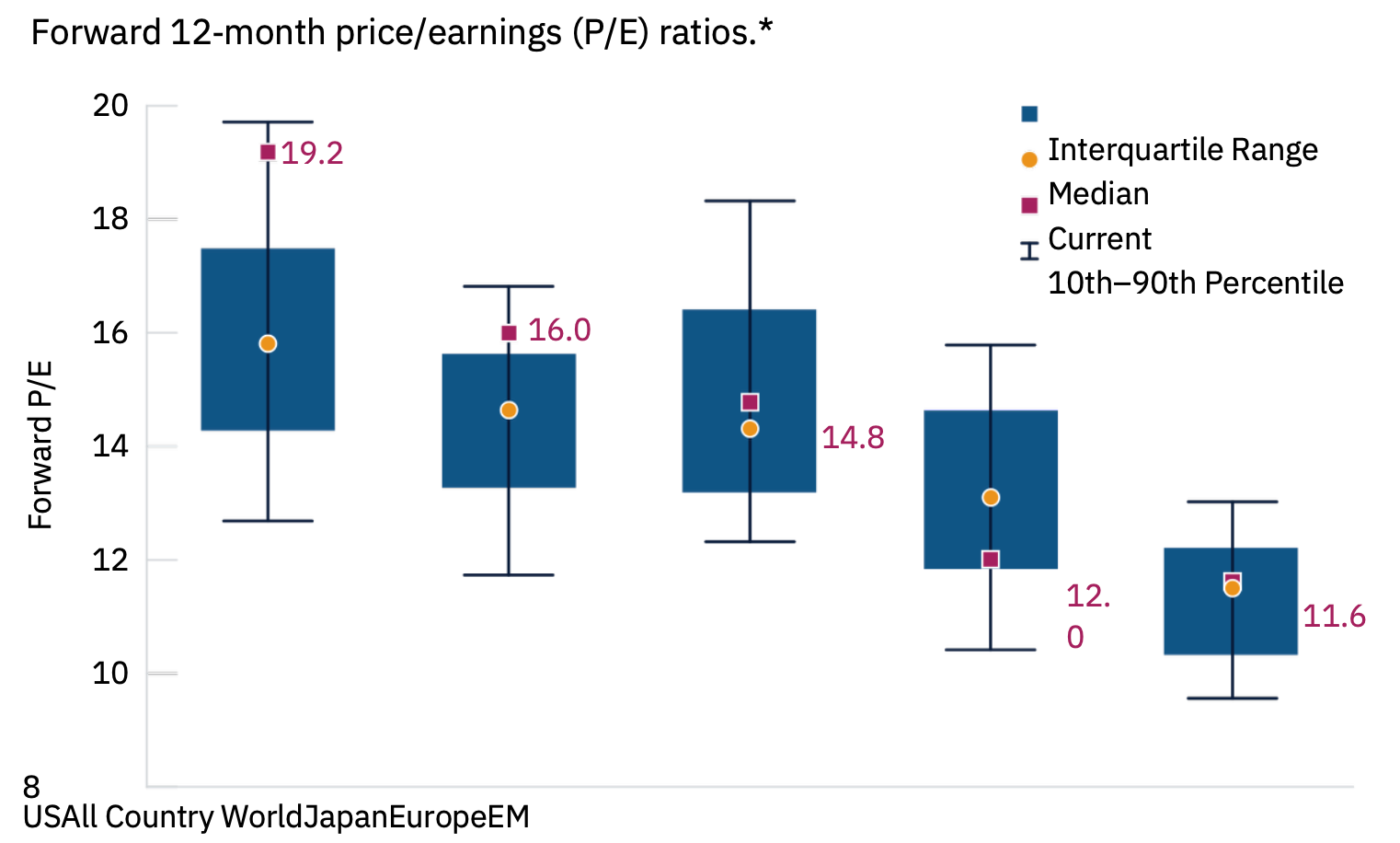

Figure 7 - EM equity valuations appear relatively cheap

As of November 20, 2023.

Source: Goldman Sachs Investment Research. Actual outcomes may differ materially from forecasts.

Technology stocks, propelled by their above average earnings performance and rising expectations for artificial intelligence (AI) applications. Through November, the Magnificent Seven stocks collectively were up over 70% for the year to date on a capitalization-weighted basis. The remaining 493 stocks in the S&P 500, on the other hand, rose less than 9.5% . Such highly concentrated markets increase risk, particularly for investment strategies measured against benchmarks that require them to maintain exposure to these outsized positions.

Stretched valuations, produced by their strong performance, leave the U.S. tech giants vulnerable to mean reversion—the historical tendency for periods of above-average performance to be followed by subpar returns. Accordingly, we believe mega-cap tech leadership is likely to fade in 2024 as the opportunity set broadens.

Figure 8 - U.S. equity performance has been top‑heavy, but that could change in 2024

As of November 30, 2023. * The Magnificent 7 are Apple, Alphabet, Amazon, Meta, Microsoft, NVIDIA, and Tesla. Performance results shown are capitalization‑weighted averages.

Source: Standard & Poor’s (see Additional Disclosures). AGM analysis using data from FactSet Research Systems Inc. All rights reserved.