Japan’s Debt Crisis: The Highest Debt Burden in the Developed World – Sustainability Risks in 2026

Japan’s debt model has survived for years on low rates and domestic ownership, but rising yields and BoJ normalization are raising fresh sustainability risks.

OpenMacro

Japan’s massive public debt has long been sustained by domestic ownership and ultra-low rates, but rising yields, fiscal expansion, and BoJ normalization are increasing the risk that debt servicing costs become materially harder to manage.

Japan’s public debt stands as the highest among advanced economies, with gross government debt-to-GDP exceeding 230% to 260% in 2026, depending on the measurement used.

For decades, this mountain of debt, built through persistent deficits to fight stagnation and deflation, has been managed without crisis thanks to unique domestic factors: ultra-low interest rates, massive Bank of Japan bond purchases, and the fact that nearly all debt is held by Japanese institutions and citizens.

However, the policy landscape is shifting dramatically. Rising yields, monetary normalization, fiscal expansion under new leadership, and structural headwinds are raising serious questions about long-term sustainability.

Figure 1

Japan’s era of near-zero yields is ending, increasing the fiscal sensitivity of an already enormous public debt burden.

Source: OpenMacro

The Scale of the Problem

Gross debt reached roughly 1,342 trillion yen by late 2025, against nominal GDP of around 665 trillion yen. Net debt, after accounting for government assets, is lower at roughly 77% to 130% of GDP, but the headline figure still dwarfs peers such as the United States and Italy.

Debt-servicing costs are projected to climb sharply, from 31.3 trillion yen in fiscal 2026 to more than 40 trillion yen by fiscal 2029, potentially consuming around 30% of the budget. Every 1% rise in yields adds materially to annual interest costs.

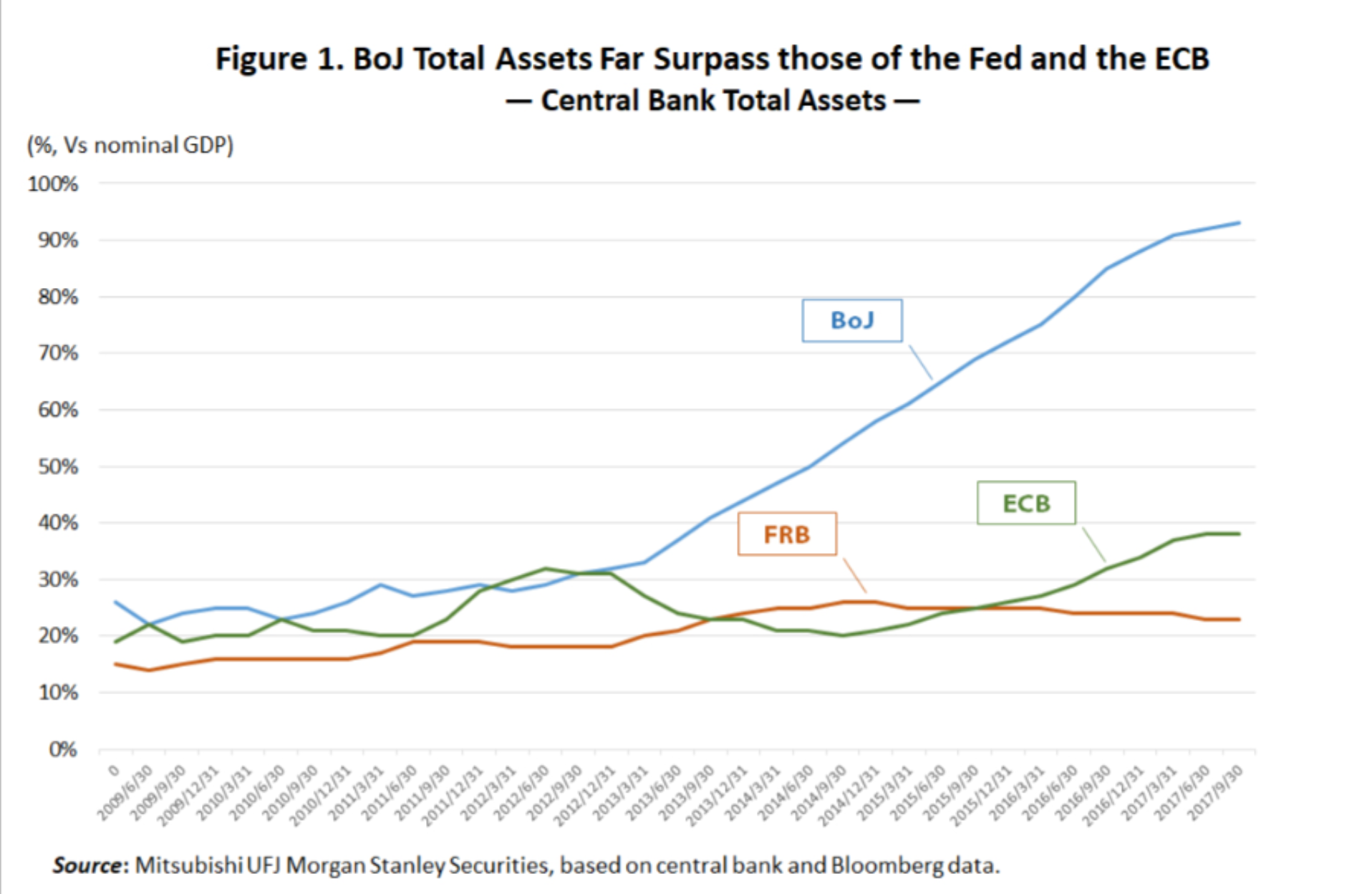

Why No Crisis So Far? Domestic Ownership and BoJ Support

Approximately 90% of Japanese Government Bonds are held domestically, reducing rollover risk from foreign investors. The Bank of Japan owns more than 50% of outstanding JGBs, effectively monetizing debt and suppressing yields for years.

This form of financial repression kept effective interest rates near zero, allowing nominal GDP growth, even if modest, to outpace interest costs. That classic r < g dynamic helped stabilize debt ratios.

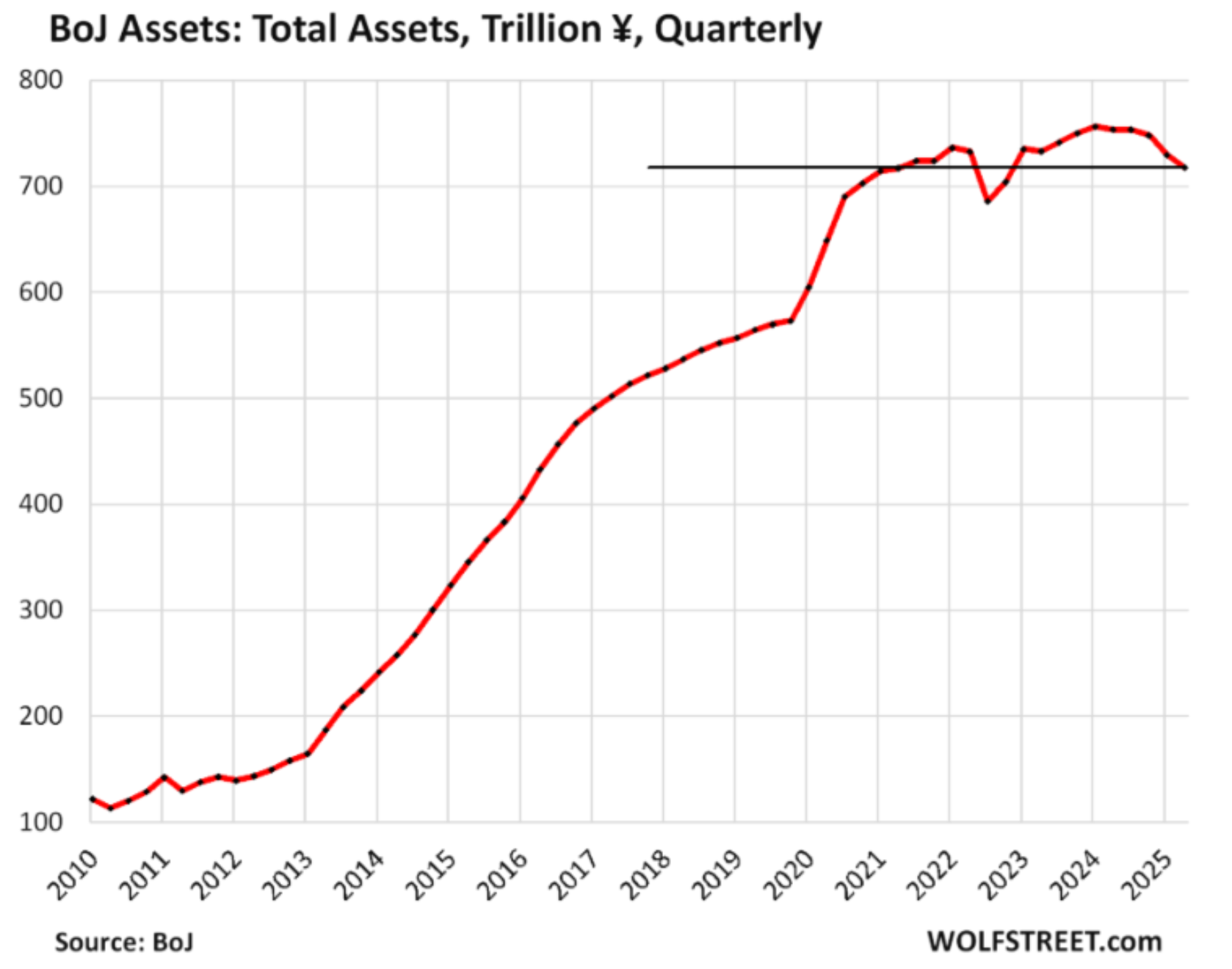

Figure 2

The BoJ’s balance sheet is exceptionally large relative to GDP, highlighting how heavily Japan has relied on central-bank support to sustain its fiscal model.

Source: Mitsubishi UFJ Morgan Stanley Securities, based on central bank and Bloomberg data

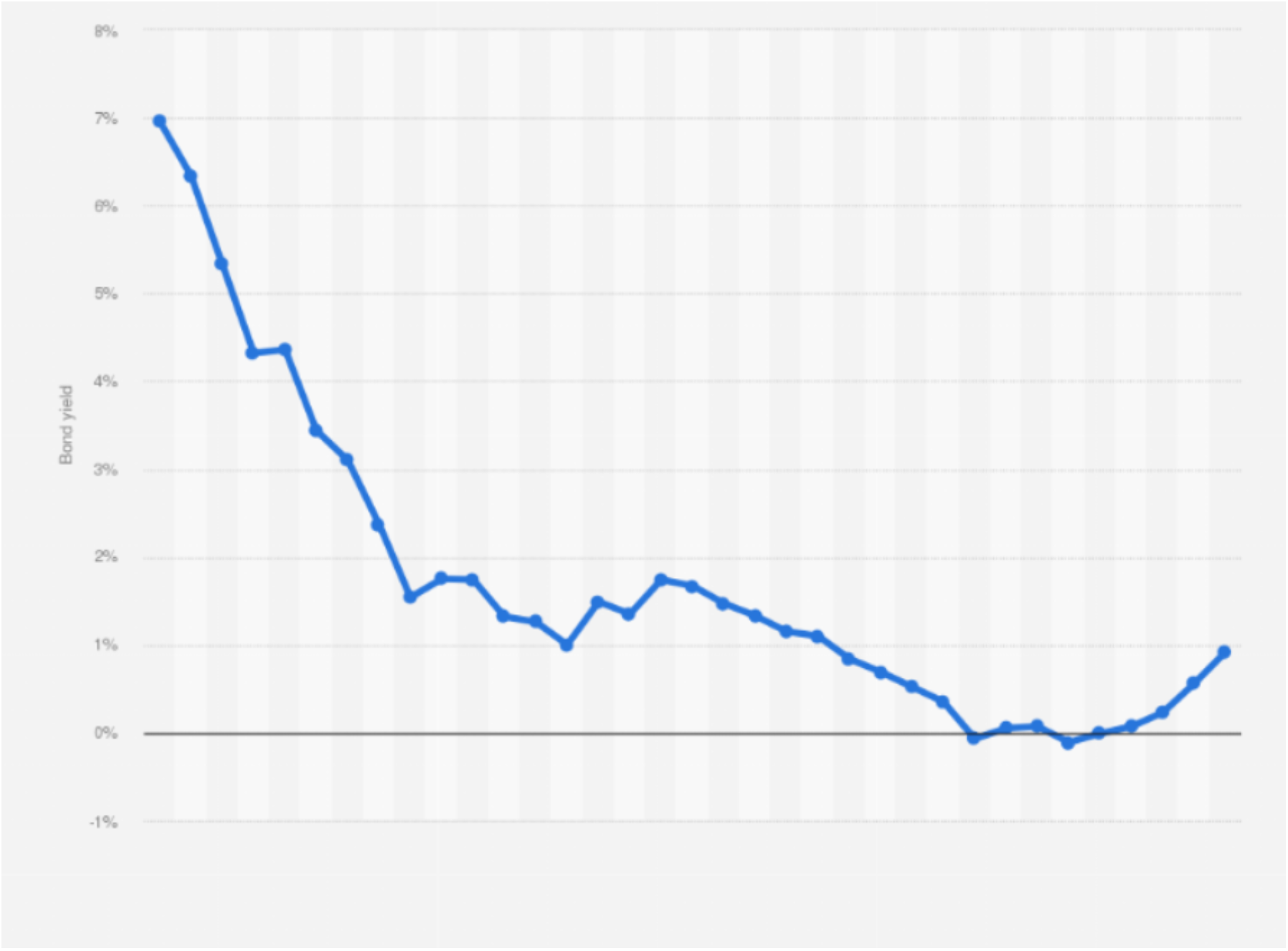

The Shifting Landscape: Rising Yields and Monetary Normalization

Since the BoJ ended yield-curve control in 2024 and began gradual rate hikes, with policy reaching around 0.75% by late 2025, 10-year JGB yields have tripled from historic lows to around 2% or higher, the highest in more than two decades.

Fiscal stimulus packages under Prime Minister Sanae Takaichi, including tax cuts, defense spending, and childcare measures, are widening deficits at precisely the moment the BoJ is reducing bond purchases. Markets are pricing in higher long-term rates, steepening the yield curve and raising concerns about a potential debt spiral.

Yen Weakness Adds Fuel to the Fire

The yen has weakened significantly, with USD/JPY trading in the 150 to 160 range, driven by interest-rate differentials and fiscal loosening.

A weaker yen boosts exports and tourism but also raises import costs for energy and food, feeding inflation and pressuring real wages. Intervention attempts by the Ministry of Finance have had limited success while the BoJ continues an accommodative stance. Persistent depreciation risks further eroding investor confidence.

Structural Headwinds: Demographics and Growth

Japan’s aging and shrinking population caps potential growth at roughly 0.5% to 1.0% annually. Productivity gains remain elusive, and labor shortages persist despite wage growth reaching multi-decade highs.

Primary fiscal deficits remain around 2% to 5.5% of GDP in the near term. Without more forceful reforms, such as asset sales, pension adjustments, or tax increases, the debt trajectory becomes harder to sustain if rates continue to rise. Some economists now argue that Japan is closer to a debt crisis than markets assume.