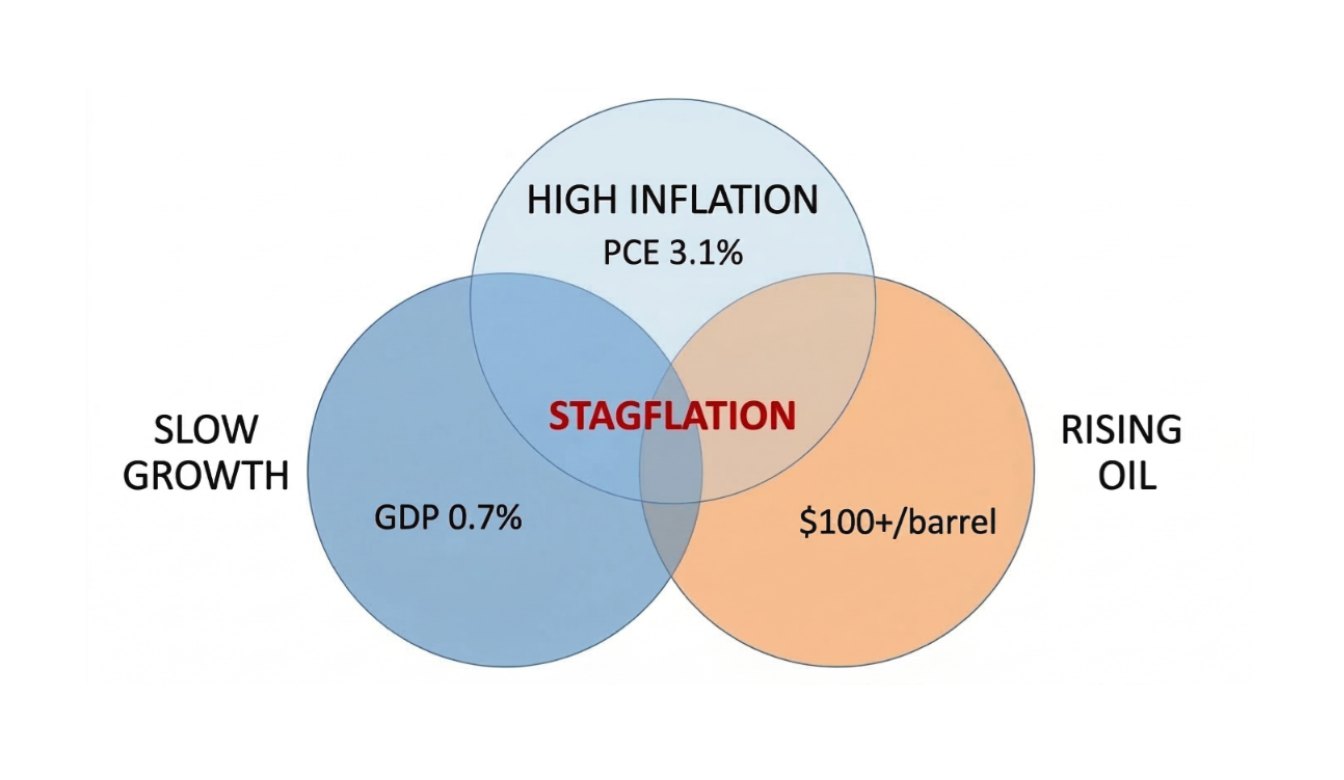

Stagflation 2026?

The Iran conflict and Strait of Hormuz disruption are turning an energy shock into a broader threat of slower growth and higher inflation.

OpenMacro

The 2026 Iran conflict has pushed oil above $100 and revived a global stagflation threat. Growth forecasts are being cut while inflation expectations rise, leaving central banks facing the same painful tradeoff seen during the major oil shocks of the 1970s.

The 2026 Iran conflict and the resulting disruption in the Strait of Hormuz have transformed what began as a geopolitical supply shock into a full-blown stagflationary threat.

Oil prices have remained above $100 per barrel for weeks, driving headline inflation higher across major economies while simultaneously weakening global growth. Economists at the IMF, World Bank, and major investment banks have already revised 2026 global GDP forecasts downward by 0.4 to 0.7 percentage points. At the same time, inflation expectations for the United States and Europe have been pushed up sharply.

This toxic combination, rising prices and slowing growth, is exactly what defined the stagflation of the 1970s, triggered by the 1973 Yom Kippur War and the 1979 Iranian Revolution. Back then, central banks faced an impossible dilemma: fight inflation with higher rates and risk deeper recession, or support growth and let inflation run hot.

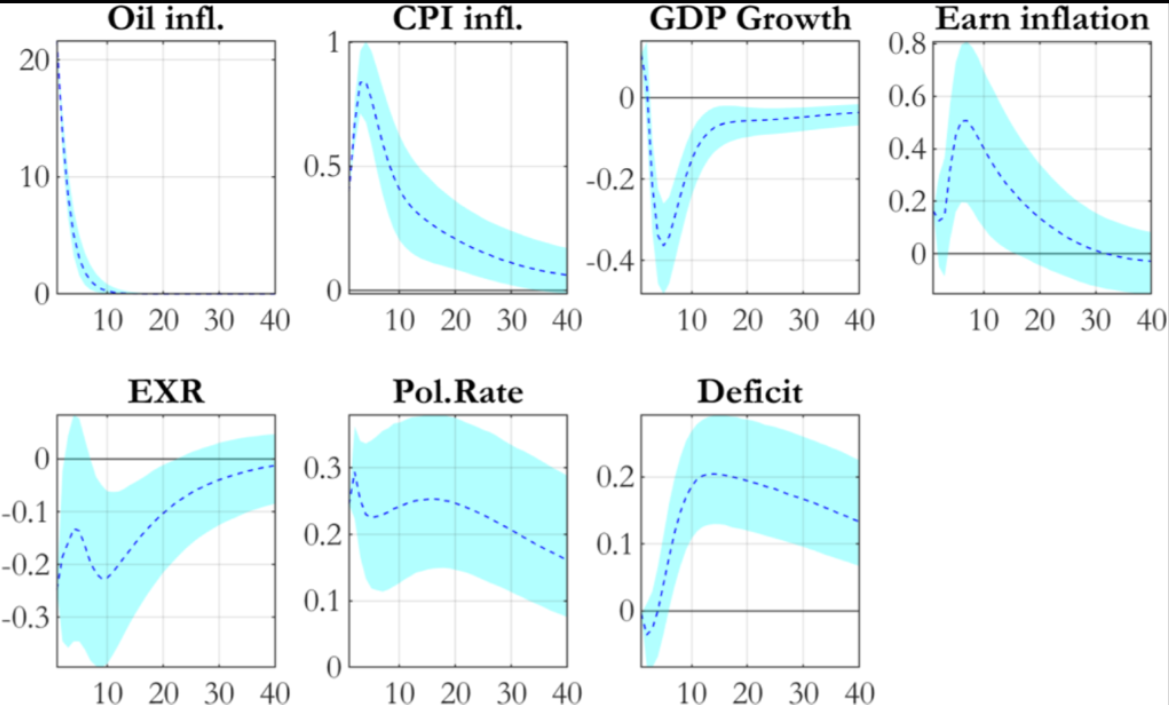

Figure 1

Estimated macro effects of an oil shock across inflation, GDP growth, exchange rates, policy rates, and fiscal deficits.

Source: OpenMacro

Today the situation is even more complex. Major economies enter this shock with significantly higher public debt levels, exhausted fiscal space after the pandemic, and central banks that have only recently begun to normalize policy after years of ultra-loose conditions.

The United States is already seeing core PCE inflation climb toward 3.1%, while Europe faces energy-driven price pressures that are pushing CPI forecasts for 2026 above 3%. Emerging markets are feeling the pain even more acutely. Countries with large current-account deficits and heavy reliance on imported energy are seeing capital outflows and currency depreciation, which further fuels imported inflation.

The big unknown is how central banks will respond. Will the Fed and ECB prioritize inflation control and accept slower growth, or will they hesitate and allow inflation expectations to become unanchored? History suggests that delayed or inconsistent policy responses only prolong the pain.

The 2026 oil shock is not just another energy spike. It is testing the resilience of the post-pandemic global economy and forcing policymakers to confront a scenario many had hoped was consigned to the history books.

Bottom line: stagflation risk in 2026 is real, and markets are beginning to price it in. Investors should prepare for higher volatility, stickier inflation, and a more challenging environment for both equities and bonds.

Related Research

Geopolitics

US Miscalculation in the Iran Conflict: Hormuz Oil Shock and Inflation Pressure Force Early Negotiations Push

Inflation

US Inflation Reaccelerates: Energy Drives 3.3% Jump, Clouding the 2026 Outlook

Recession