The Energy Tax Returns: How Sustained High Oil Prices Are Fueling US Inflation Risks in 2026

Persistently high oil prices are re-emerging as a major inflation driver, raising the risk of stickier CPI and a more constrained Fed path.

OpenMacro

Sustained oil above $100 is becoming a major inflation risk for the US in 2026. With energy costs feeding into transport, manufacturing, and household bills, elevated crude prices could keep CPI above target, reduce the odds of rate cuts, and raise stagflation concerns.

As of early April 2026, WTI crude is trading near $112 per barrel and Brent around $110, levels not seen since the peak of previous energy shocks. While markets have focused on the immediate geopolitical fallout from the Iran conflict, the longer-term macro implication is becoming clear: if these elevated energy prices persist for several more months, they will deliver a significant second-round boost to US inflation.

According to RBC Economics, a sustained period above $100 oil could push headline CPI above 3% through the remainder of 2026. Wall Street analysts estimate that every $10 sustained increase in the oil price adds roughly 0.3 to 0.4 percentage points to headline CPI. This pass-through effect is not limited to gasoline. Higher energy costs flow directly into transportation, freight, manufacturing, and food production, all of which feed into both headline and, eventually, core inflation metrics.

The mechanism is straightforward: energy acts as an implicit tax on the entire economy. Households face higher costs at the pump and for heating, while businesses absorb rising input costs that are eventually passed on to consumers. Estimates suggest that $100-plus oil for a prolonged period could add an extra roughly $150 billion in annual costs to American consumers through higher fuel and energy bills alone.

This dynamic complicates the Federal Reserve’s path. With inflation already proving sticky, sustained high energy prices reduce the likelihood of aggressive rate cuts in 2026 and could even revive market speculation about a pause or, in an extreme scenario, renewed tightening talk. The risk of stagflation-lite, higher inflation combined with slower growth, is now a serious consideration among institutional investors.

The market is already pricing in some of these risks. Summer Brent futures are trading at a discount to spot prices, a classic backwardation signal that traders expect prices to ease later in the year, and 10-year Treasury yields have remained below their pre-war highs. This suggests that while the near-term inflationary impulse is real, investors still anticipate a partial recovery in global oil supply as tensions moderate.

Nevertheless, the near-term pressure is undeniable. Until oil and gas prices show clear signs of sustained decline, the energy tax will remain one of the most important macro headwinds for the US economy in 2026.

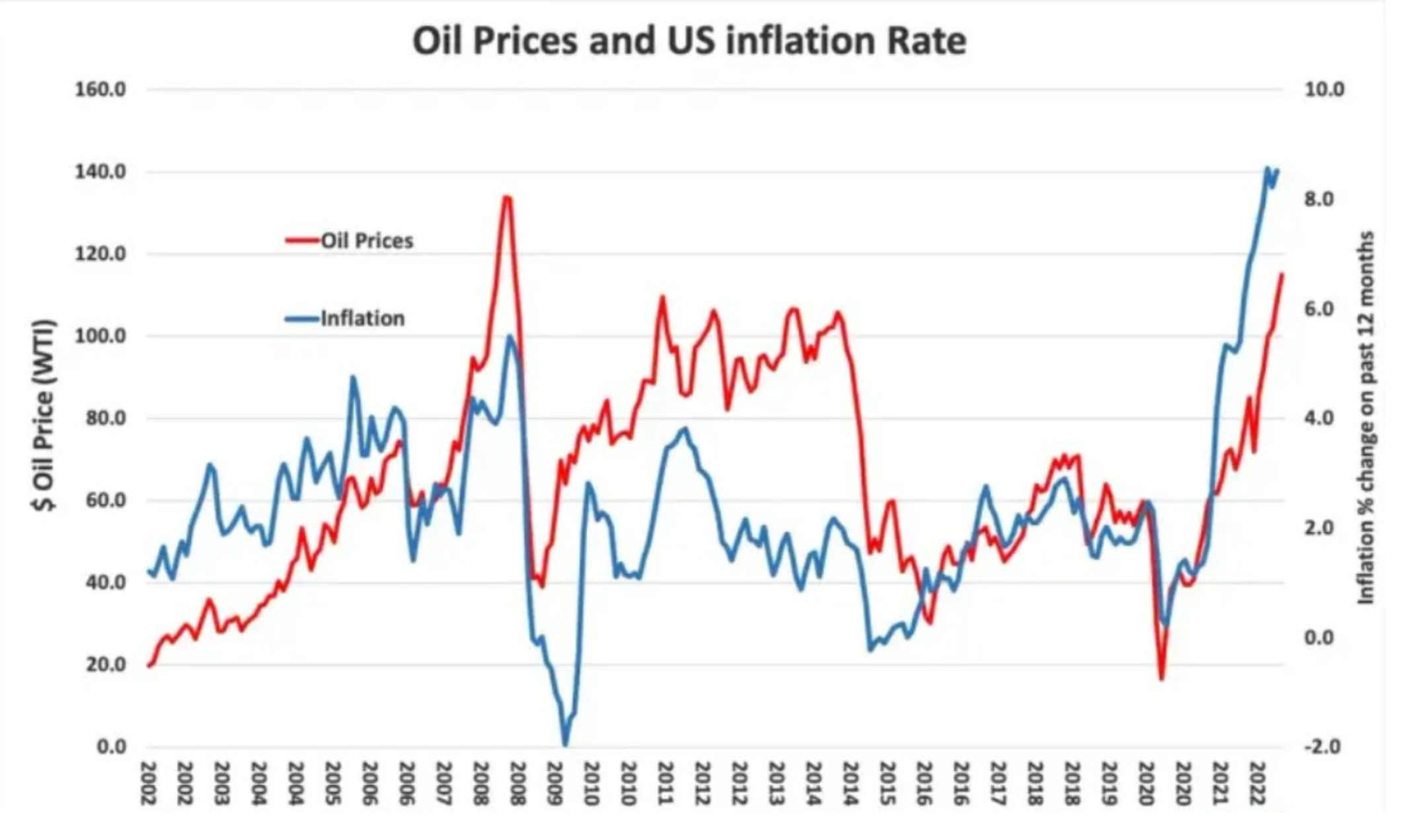

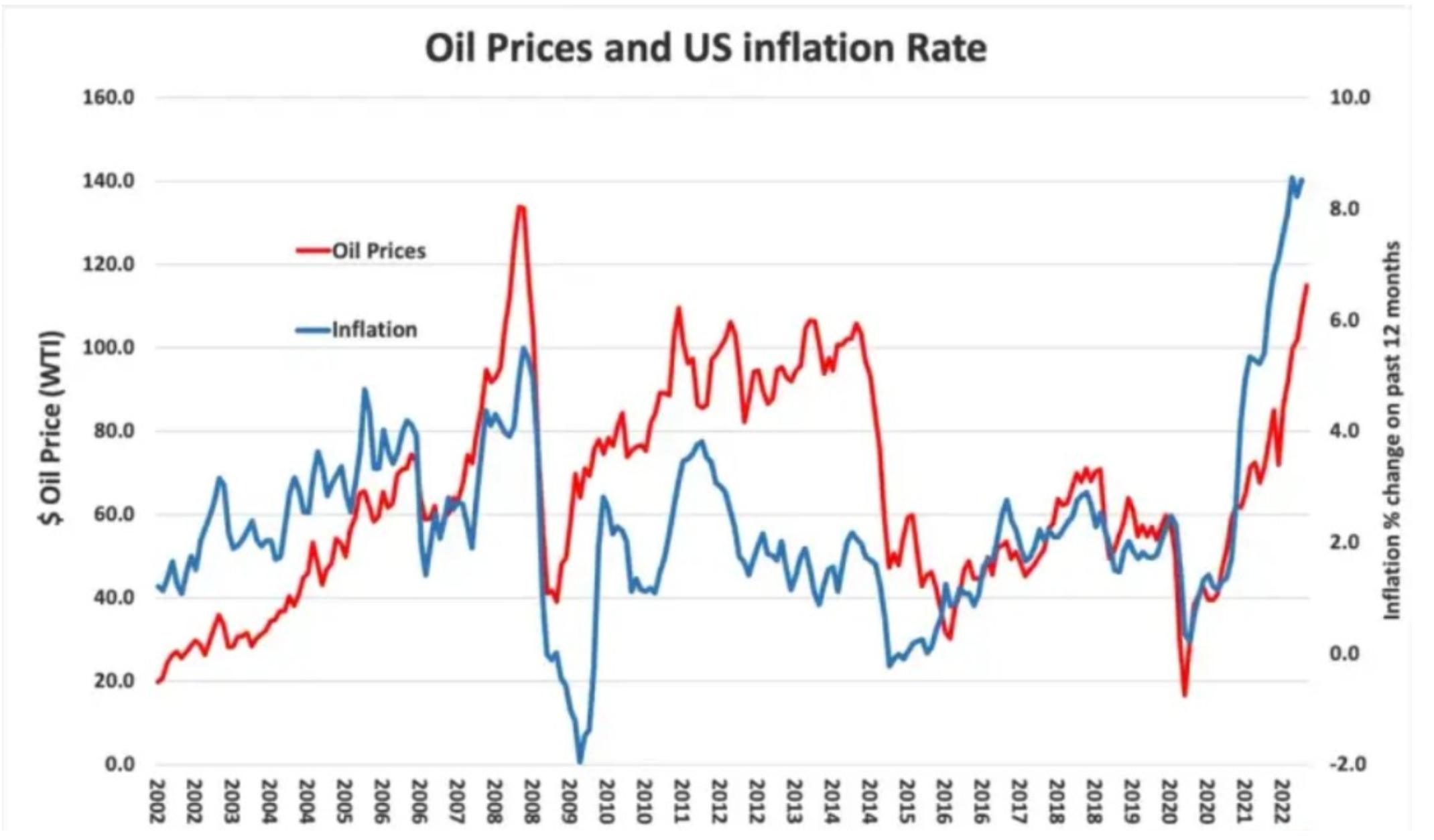

Historical relationship between rising oil prices and US inflation pressure.

Source: OpenMacro