The UK’s Macroeconomic Crisis: Brexit, Energy and the Cost of Leaving Europe’s Economic Core

Britain’s weak growth reflects two structural shocks: costly energy dependence and the loss of frictionless access to the European Single Market.

Renaissance Europe

The UK’s macroeconomic weakness is not just cyclical. Brexit raised trade frictions with its largest market, while energy dependence exposed households and industry to price shocks, weakening growth, investment, productivity, and real incomes.

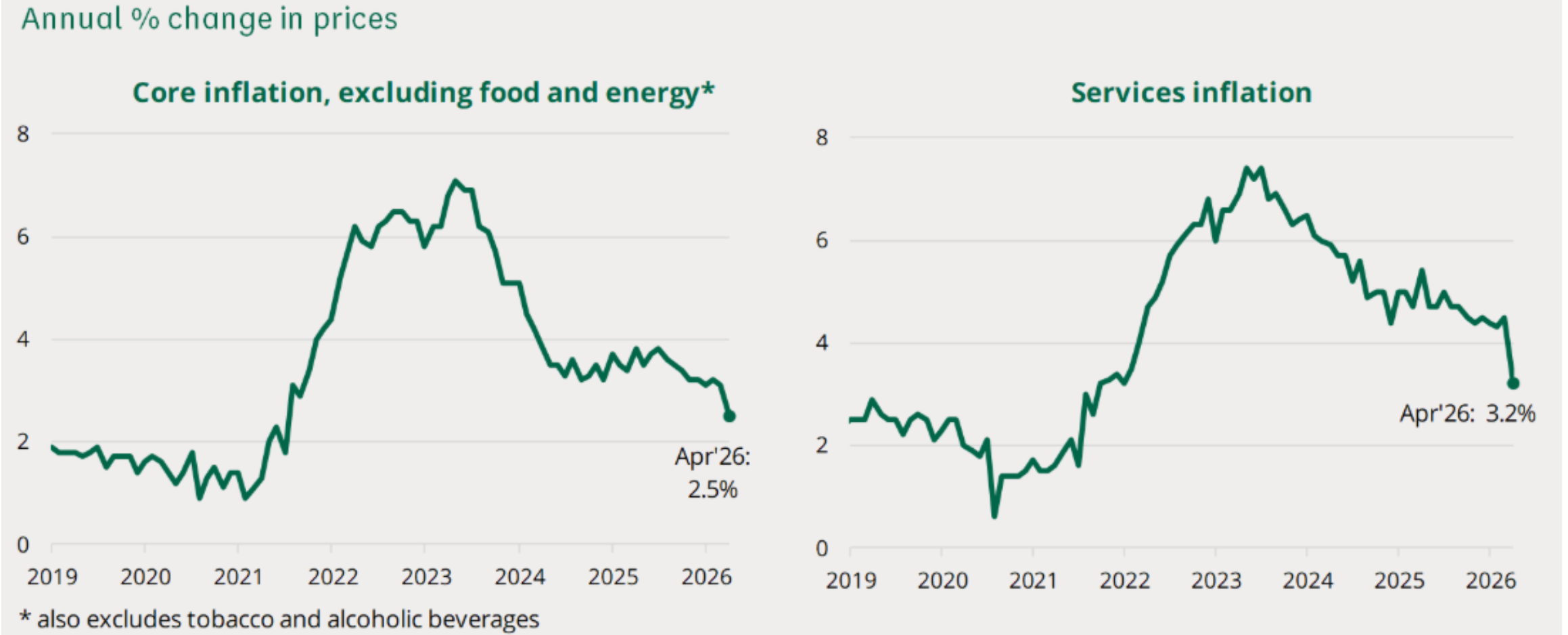

Figure 1

Inflation has eased from its post-energy-shock peak, but services inflation remains elevated, keeping pressure on households and monetary policy.

Source: ONS

The United Kingdom is facing one of the most structural macroeconomic crises in the developed world. It is not the result of one shock, but of two overlapping shocks: the post-2022 energy crisis and the loss of frictionless access to the European Single Market after Brexit.

The result has been weak growth, high inflation, falling competitiveness, pressure on real incomes, weaker investment, a deteriorating goods trade position, and a deep productivity problem.

In 2025, UK GDP grew by only 1.4%, after growth of around 1.0% in 2024. Real GDP per head remained weak, meaning that the economy was expanding only slowly while living standards stayed under pressure. In Q1 2026, GDP rose by 0.6%, but this followed only 0.2% growth in Q4 2025, showing that the recovery remains fragile rather than structurally strong.

The First Shock: Energy Dependence

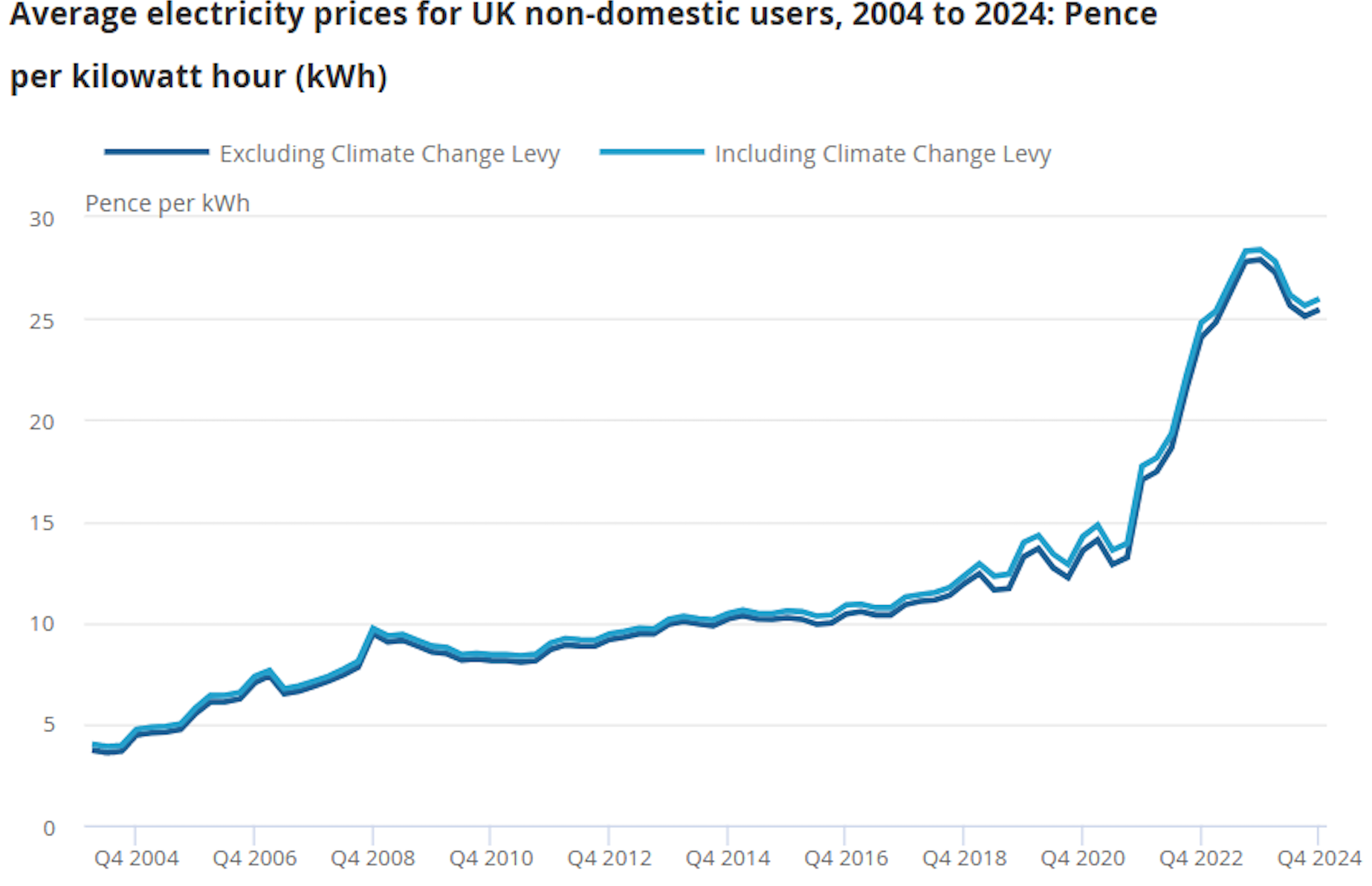

Figure 2

UK industrial and commercial electricity prices surged after the energy crisis, intensifying pressure on margins, investment, and competitiveness.

Source: DESNZ, Gas and electricity prices in the non-domestic sector

The first shock was energy. The UK is a net energy importer. In 2025, its net import dependency was still around 43.5%, while fossil fuels still accounted for 75.2% of UK energy consumption.

That means the British economy remains heavily exposed to global gas and energy-price shocks. When Russia’s full-scale invasion of Ukraine triggered the European energy crisis, the UK was hit directly through gas-linked electricity prices, household bills, and industrial costs.

UK CPI inflation reached 11.1% in October 2022, the highest rate in around four decades. The pressure on households was enormous. Average annual dual-fuel bills for typical consumption rose by 54% in the April 2022 price cap and by a further 27% in October 2022, even with government intervention limiting the full rise.

The pressure on industry was just as damaging. In 2023, UK industrial electricity prices were 46% higher than the IEA median, and over the previous decade they had ranged between 17% and 49% above the IEA median.

This directly damaged manufacturing, chemicals, steel, automotive, food processing, and other energy-intensive sectors. High energy prices do not only increase bills. They destroy competitiveness, reduce margins, discourage investment, increase import dependence, and weaken the industrial base.

UK energy shock indicators

| Indicator | Approximate Value | Macroeconomic Impact |

|---|---|---|

| Net energy import dependency | 43.5% | Leaves the UK exposed to global energy shocks |

| Fossil fuels in energy consumption | 75.2% | Keeps the economy tied to volatile fossil-fuel markets |

| Peak CPI inflation | 11.1% | Shows the household cost of the energy shock |

| April 2022 energy price-cap rise | 54% | Sharp increase in typical household energy bills |

| October 2022 energy price-cap rise | 27% | Additional pressure despite government intervention |

| Industrial electricity premium | 46% above IEA median | Weakens manufacturing and industrial competitiveness |

The Second Shock: Brexit

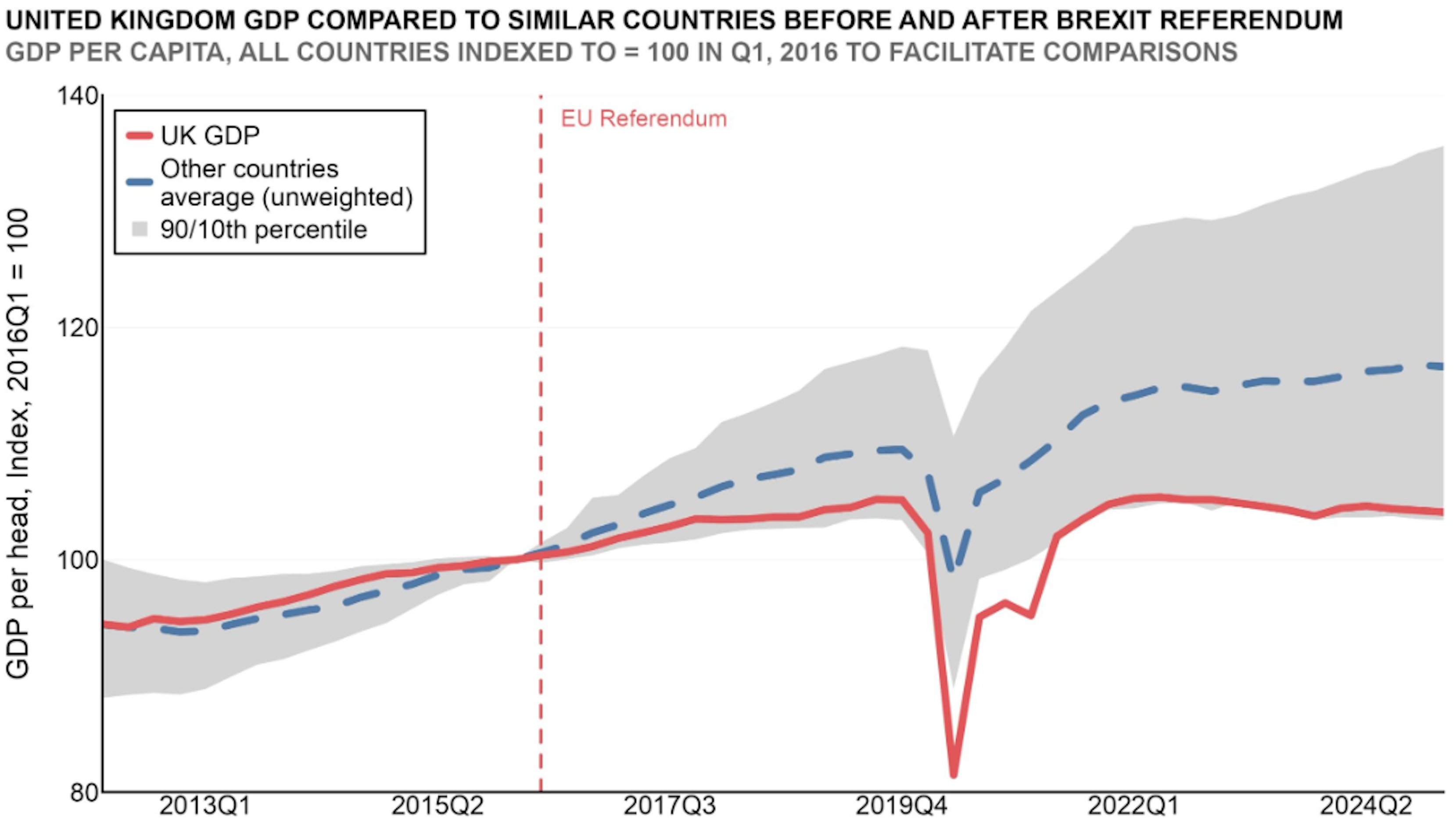

Figure 3

UK GDP per capita has underperformed comparable economies since the Brexit referendum, reinforcing concerns about weaker productivity and investment.

Source: Econofact; OECD; Irish Central Statistics Office; World Bank

The second shock was Brexit. Leaving the European Union did not simply mean leaving a political institution. It meant leaving the most important economic integration project in the world: the European Single Market.

The UK’s largest trading partner remains the EU. In 2025, UK exports of goods and services totalled £931 billion, with the EU accounting for 41% of them, around £382 billion. UK imports totalled £970 billion, with the EU accounting for 49%, around £475 billion.

This means the UK left the regulatory and customs framework of the market that still absorbs more than two-fifths of its exports and supplies nearly half of its imports.

The economic damage is visible. The Office for Budget Responsibility has stated that evidence remains consistent with its assumption that Brexit will reduce both import and export intensity by around 15% in the long run.

More recent academic estimates are even more severe. A 2026 Federal Reserve note summarising the literature reports that by 2025 Brexit may have reduced UK GDP by 6–8%, investment by 12–18%, employment by 3–4%, and productivity by 3–4%.

The Cost of Trading Outside the Single Market

This is the central point: Brexit did not make the UK more globally competitive. It increased trade frictions with its closest, largest, and richest market.

The UK still depends heavily on Europe, but now trades with it from outside the Single Market. That means customs checks, rules-of-origin requirements, regulatory divergence, border frictions, duplicate certification costs, and reduced attractiveness as a base for serving the European market.

What Brexit added

- Customs checks

- Rules-of-origin requirements

- Regulatory divergence

- Border frictions

- Duplicate certification costs

- Lower attractiveness as an EU market base

What the UK lost

- Frictionless Single Market access

- Simpler cross-border trade

- EU-wide regulatory certainty

- Stronger export intensity

- Easier supply-chain integration

- Greater investment appeal

The Three-Pillar Strategy Britain Needs

The UK needs a new economic strategy based on three pillars.

First, it needs cheaper and more stable energy. That means accelerating domestic electricity generation, grids, storage, nuclear, offshore wind, interconnectors, and long-term power contracts that reduce the link between gas prices and electricity prices.

Second, it needs deeper economic reintegration with Europe. The UK does not need symbolic debates. It needs practical access: lower trade barriers, regulatory alignment where economically useful, veterinary and food agreements, industrial cooperation, mobility for skilled workers, energy-market cooperation, and deeper defence-industrial integration.

Third, it needs a serious productivity agenda: higher business investment, planning reform, infrastructure delivery, capital-market depth, R&D, AI adoption, technical education, and industrial policy focused on sectors where Britain can still lead.

Cheaper Energy

- Domestic electricity generation

- Grid expansion

- Storage investment

- Nuclear and offshore wind

- Interconnectors

- Long-term power contracts

European Reintegration

- Lower trade barriers

- Targeted regulatory alignment

- Food and veterinary agreements

- Skilled-worker mobility

- Energy-market cooperation

- Defence-industrial integration

Productivity Renewal

- Higher business investment

- Planning reform

- Infrastructure delivery

- Capital-market depth

- R&D and AI adoption

- Technical education

Britain’s growth problem will not be solved by waiting for the cycle to turn. It requires cheaper energy, deeper European access, and a credible productivity strategy.

Conclusion

The British macroeconomic crisis is not a normal cyclical slowdown.

It is the consequence of leaving the Single Market while remaining economically dependent on it, combined with an energy system still too exposed to imported fossil fuels and gas-linked electricity prices.

Until Britain solves the contradiction between political separation from Europe and economic dependence on Europe, its growth model will remain structurally weaker than it needs to be.