Why the U.S. Consumer Discretionary Sector Underperformed So Badly in 2025

High rates, sticky inflation, weak confidence, and tariff pressure combined to make consumer discretionary one of the S&P 500’s biggest laggards in 2025.

OpenMacro

The consumer discretionary sector badly lagged the broader market in 2025 as high borrowing costs, persistent inflation, weak sentiment, and tariff-related cost pressures squeezed both demand and margins.

The consumer discretionary sector, once a market darling, became one of the biggest laggards of 2025. The S&P 500 Consumer Discretionary Select Sector Index, tracked closely by the XLY ETF, delivered significantly weaker returns than the broader S&P 500, with many analysts calling it a clear underperformer in a volatile macro environment.

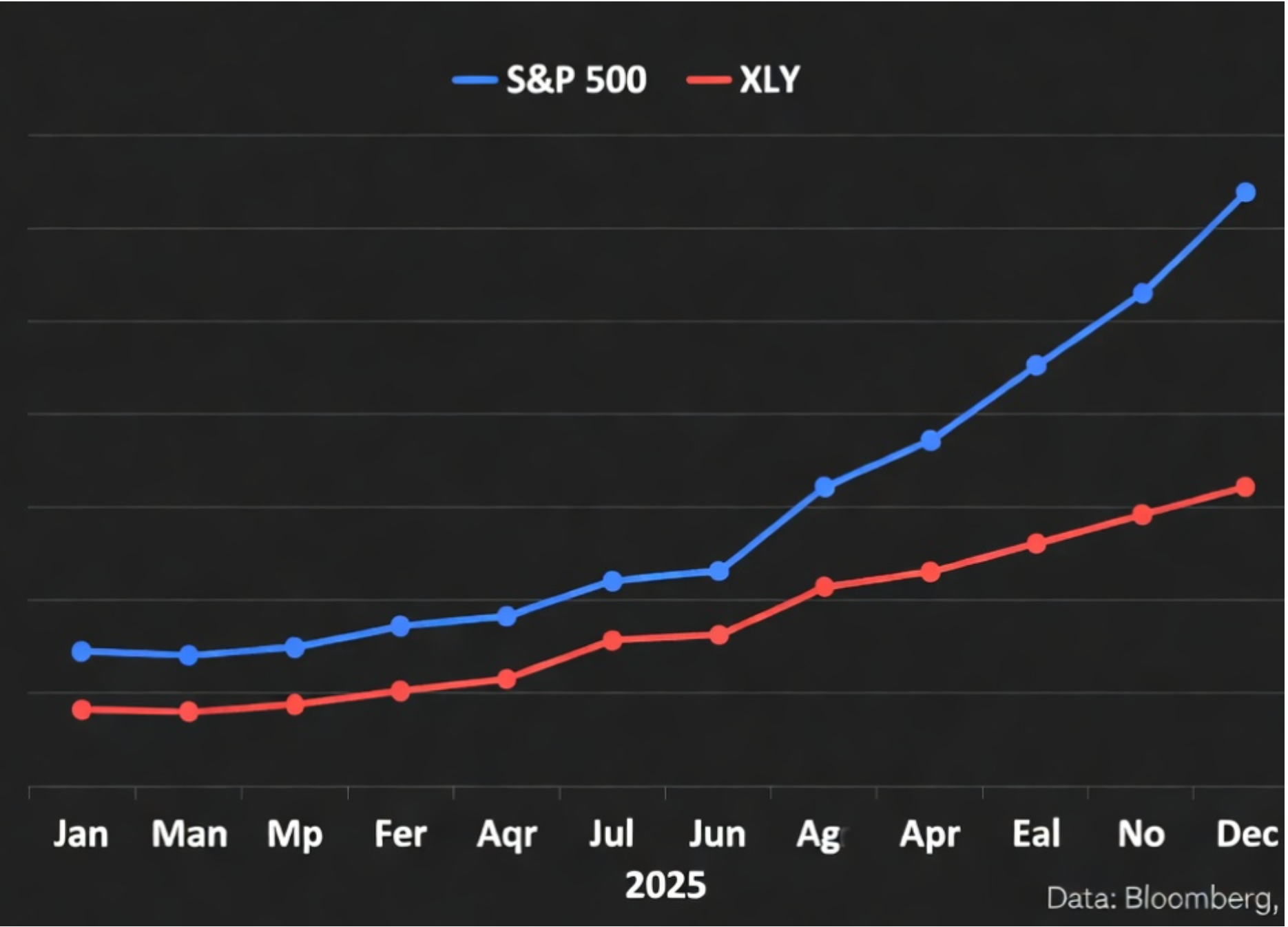

Figure 1

Consumer discretionary stocks badly underperformed the broader market in 2025 as macro headwinds hit the sector.

Source: Bloomberg

Key performance numbers in 2025:

- XLY total return: about +4.2%

- S&P 500 total return: about +18.7%

- Sector underperformance: roughly -14.5 percentage points

So what went wrong? Several forces hit the sector at once.

1. Elevated interest rates crushed big-ticket purchases.

The Federal Reserve kept rates higher for longer throughout 2025. With the federal funds rate hovering between 4.25% and 4.75% for most of the year, financing costs for cars, homes, appliances, and furniture remained painfully high. Consumer discretionary spending is highly sensitive to borrowing costs, and higher rates caused many households to delay or cancel large purchases.

2. Persistent inflation hit lower- and middle-income households hardest.

Even as headline inflation cooled from 2024 peaks, core prices, especially food, rent, and energy, remained sticky. Lower-income consumers, who devote a larger share of their budgets to essentials, had less room for discretionary spending on travel, dining, apparel, or electronics. Premium retailers and auto manufacturers felt the squeeze.

3. Weak consumer confidence and recession fears.

Surveys from the Conference Board and the University of Michigan showed sentiment staying below long-term averages. Concerns about slower growth, high debt levels, and exhausted pandemic savings pushed households to prioritize saving over non-essential purchases.

4. Heavy concentration risk in just two stocks.

Sector performance became overly dependent on Amazon and Tesla. When either showed weakness, the whole index suffered. Smaller discretionary names, including department stores, specialty retail, and hotels, generally performed even worse. 5. Early impact of new tariffs on retail costs.

Tariff hikes on imports from China and other countries increased costs for clothing, electronics, and auto parts. Many retailers passed part of these costs on to consumers, which further dampened demand.

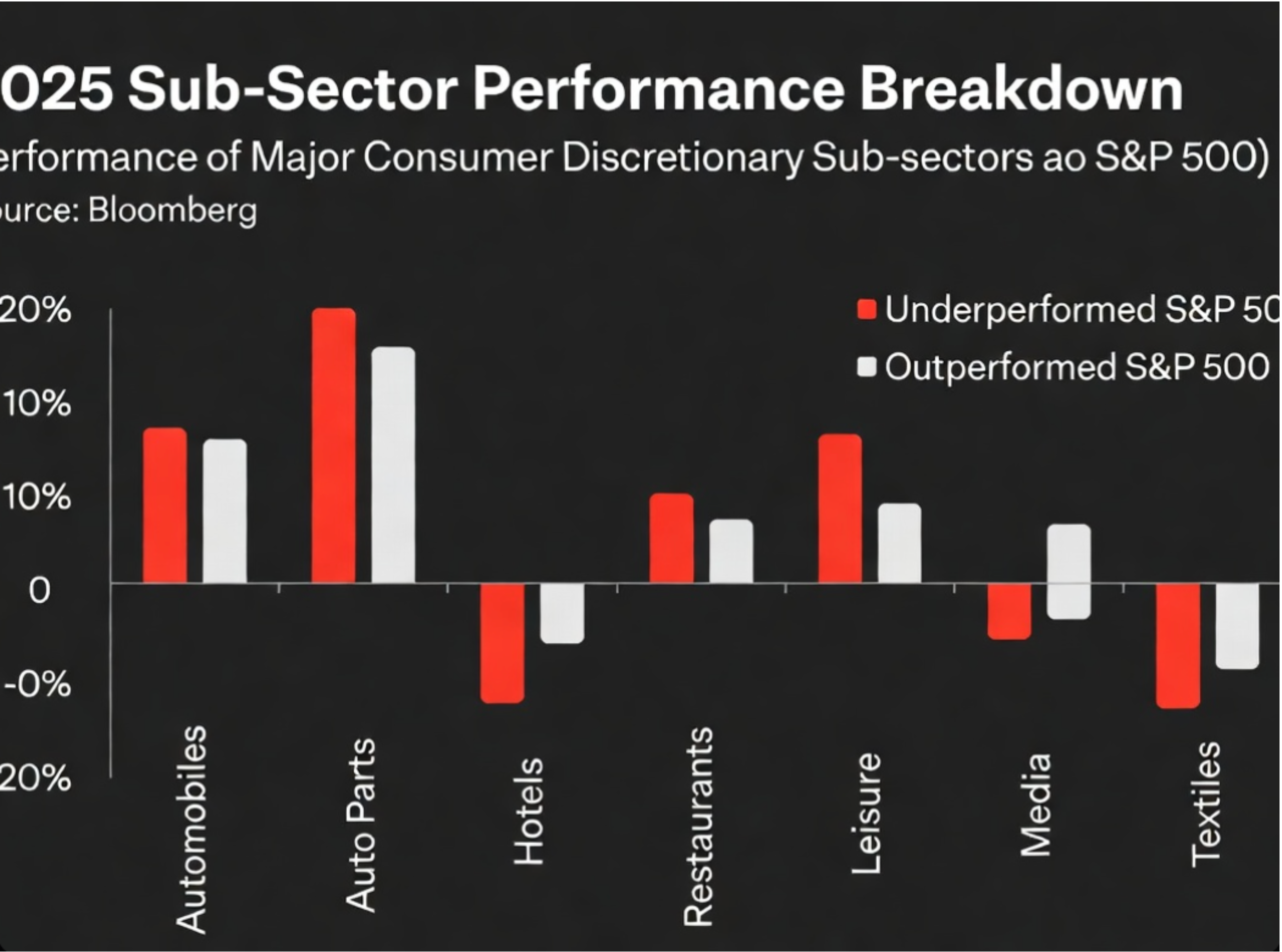

Figure 2

Weakness was broad across consumer discretionary, with hotels, textiles, and other rate-sensitive segments among the worst performers.

Source: Bloomberg

Sub-sector breakdown:

- Automobiles and components: -8%

- Retailing, including specialty and department stores: -11%

- Hotels, restaurants, and leisure: -14%

- Consumer durables: -9%

Goldman Sachs strategist David Kostin argued that the sector’s weakness suggested the US consumer was under more pressure than headline data implied. JPMorgan’s retail analysts described tariffs and rates as a double-whammy the sector could not absorb in 2025.